Introduction

When I got interested in railroads, it took me almost a year to pull the trigger and make my first purchase. Now, with a weak year for railroads, I am starting to increase my stake in the industry. In particular, I chose Canadian National (NYSE:CNI) stock as my favorite pick and am now dollar cost averaging. In this article, I will share why.

Summary of previous coverage

When I started studying railroads, I wanted to make sure I was starting to understand the industry and its economics. In this endeavour, I found great help in studying Warren Buffett and the criteria he used when he bought BNSF back in 2009 – when the financial crisis was at its worst. For those who haven’t had the chance yet, I recommend reading about my research in this article “Learning From Buffett About Investing In Railroads: The BNSF Case Study”.

After Buffett, I applied the same investing criteria to assess each one of the 5 publicly traded railroads, publishing a series called “Looking At Railroads As Mr. Buffett Does”. I used the same criteria I found Buffett was using: earning power (how many times pre-tax earnings cover interest expense); operating efficiency (operating ratio, fuel consumption); use of capital (capex, shareholder returns) and return on invested capital; free cash flow generation.

At the end of this first round of research, I bought Canadian National pick, coupled with a little position in Union Pacific (UNP). This was because Canadian National had the best overall scores in all the metrics I looked at, offering at the same time a very conservative and healthy balance sheet.

Assessing Canadian National Today

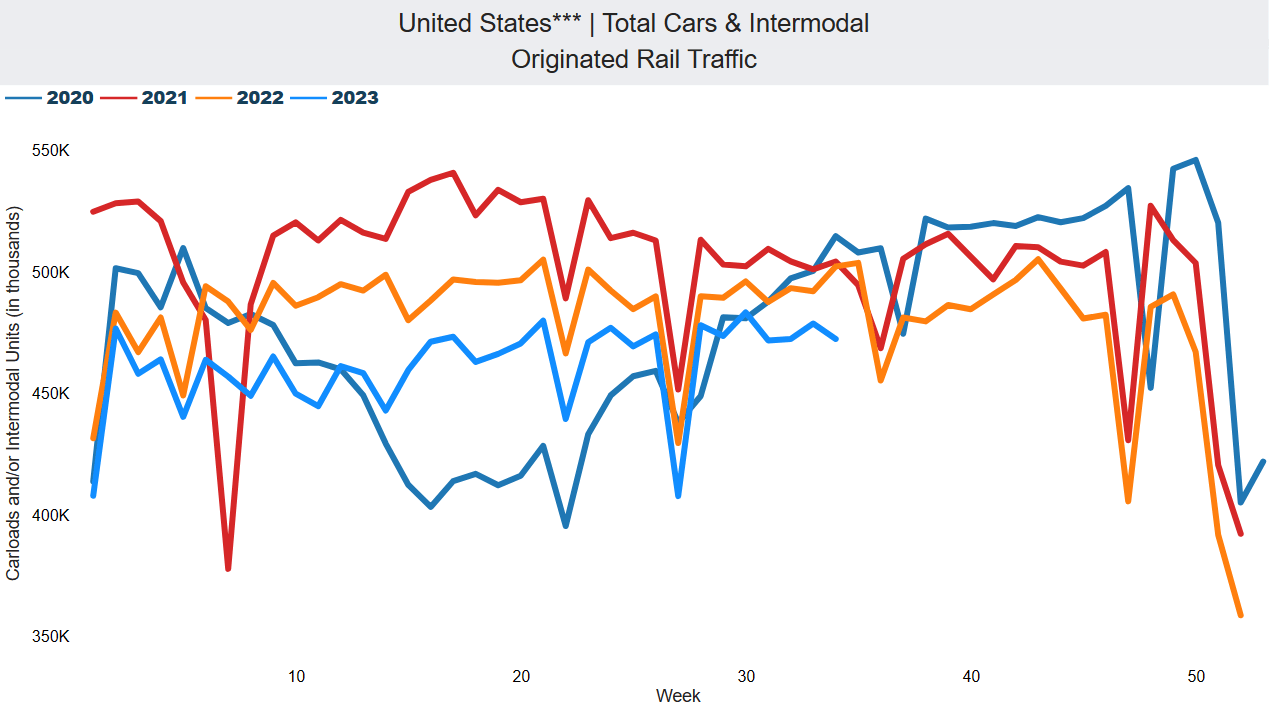

Railroads must be given time. They are long-term investments. Yet, this doesn’t mean we shouldn’t be monitoring how the company we picked performs. In particular, this is even more necessary as recent news shows U.S. weekly rail traffic declining, as the Association of American Railroads points out with this graph showing U.S. total rail traffic from 2020 (the dark blue line) to 2023 (the light blue line).

Association of American Railroads

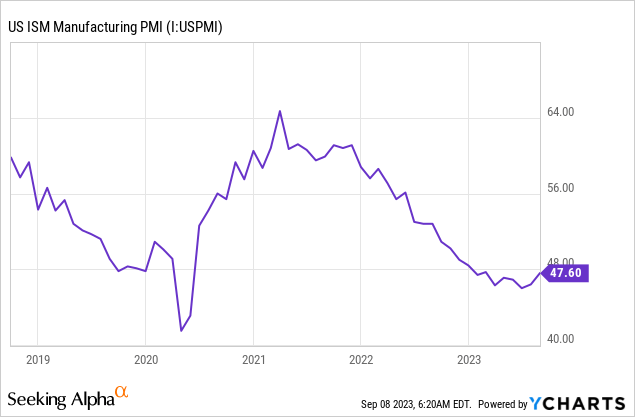

We see that 2023 has been underperforming all three previous years. Intermodal is declining and only grain and automotive are holding up freight volumes. In the meantime, the ISM manufacturing PMI index shows we are in contraction territory.

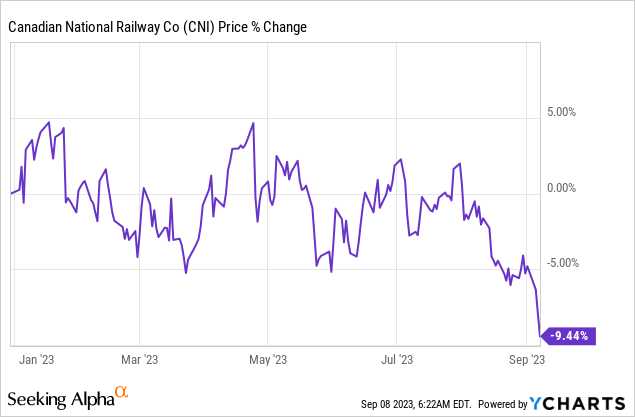

No wonder railroads are trading down while the market has been on a bull run since last October. Canadian National has lost almost 10% YtD.

This is a significant drop for a stock whose trajectory is usually trending upwards and sees rather low volatility compared to other stocks.

Canadian National Railway isn’t immune to the economic cycle. Actually, it can be considered a backbone of the economy running from the two Canadian shores all the way down to the Gulf Coast. After the company reported its first half earnings, the stock fell in aftermarket trading also because of weaker guidance for the remaining half of the year. Since then, the stock continued trading down another 6% on the Toronto Stock Exchange (almost 10% on the NYSE). May this be the setup many investors were waiting for to load more shares?

1H 2023 Results

In Q2, Canadian National’s revenues were down 7% to C$4.1 billion.

Operating income decreased 10% to $1.6 billion. The operating ratio (opex as a percentage of revenues) came in at 60.6%, which is 1.3 percentage points above the same quarter of the prior year. Surprisingly, Canadian National didn’t improve as usual its fuel efficiency, but actually reported a 6% deterioration. However, efficiency was also impacted by big fires that caused stops and starts.

As a consequence of these results, EPS were down 8% to C$1.76.

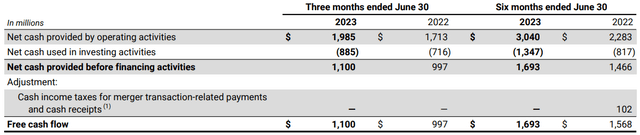

At the same time, FCF for the quarter was C$1.1 billion, 10% above Q2 2022. For the half, FCF was up 8% to C$1.7 billion. Looking at the cash flow statement we see that the increase of C$103 million is related to higher net cash provided by operating activities.

CNI Q2 2023 Report

Considering the Q2 report, we see that both in Q2 and in 1H of this year, net cash provided by operating activities was up. While net income for 1H 2023 was higher compared to 1H 2022 (C$ 2,387 million vs. C$ 2,243 million), it was down for the quarter (C$1,167 million vs. C$ 1,325). So where does the extra cash provided by operating activities come from? The main difference is from accounts receivable: C$165 million this past quarter vs. C$ (29) million. This is not something as meaningful as other items impacting free cash flow.

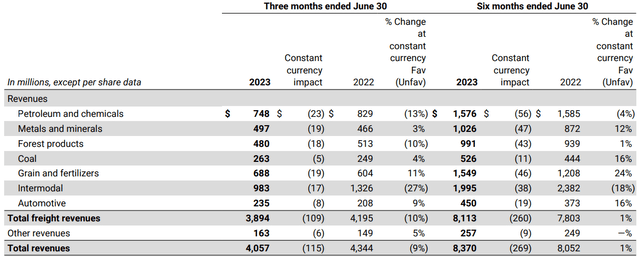

Let’s look at the revenue segment breakdown.

CNI Q2 2023 Report

Considering freight revenues, petroleum and chemicals declined due to softer demand for chemical feedstocks. During the earnings call, it was explained how this segment is particularly important because it is considered a leading indicator as the economy improves. So, since it hasn’t been going up, the indication suggests the economy is slowing down.

Forest products was down, too. But the greatest drawdown came from intermodal, with a 27% decline YoY. The company reported some margin pressure within the short haul business, where the trucking industry is stronger and competes with railroads.

Coal for metallurgical use was up, however thermal coal was weaker, as Canadian National’s management explained during the earnings call.

Grain revenues were up, though volumes were down. However, the company reported that:

Canadian grain was the bright spot in the quarter with close to 50% more RTMs versus last year. We continue to deliver for our grain customers and to engage closely to optimize the supply chain. In April, the Canadian Transportation Agency announced a 12% pricing index increase for the upcoming 2023/2024 crop year for CN.

this means that we should still see stronger revenues throughout the next quarters. In addition, it seems we are preparing for the second largest harvest in Canadian history, with yields declining slightly, but more than offset by a 3% increase in planted area. This will surely impact positively Canadian National.

Given the overall situation, it is no surprise Canadian National’s management decided to take a hard look at its year-end outlook. Assuming now that the economic recovery is pushed into 2024, Canadian National now expects its annual adjusted EPS to be flat to slightly negative.

Takeaway

It is before everyone’s eyes: railroads are going through the tough part of the cycle and this past quarter may only be the beginning of a longer period where we will see declining results. Nonetheless, Canadian National wants to stick to its 2024-2026 plan of 10%-15% EPS CAGR, with a 15%-17% ROIC. Dividend growth will be in line with earnings growth and share repurchases will achieve 2.5x leverage target over time (in other words, they will be increased compared to the past, amounting to around C$4 billion per year, which is around 4.1% of the current market cap in Toronto).

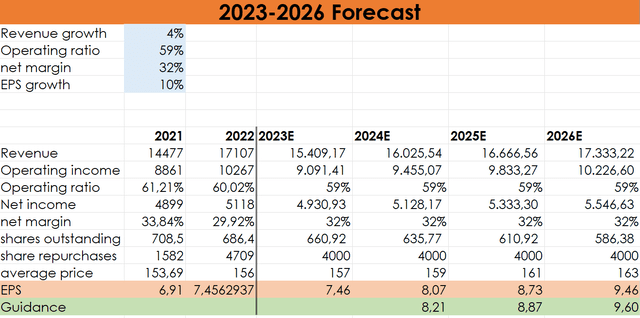

Instead of running another discounted cash flow model, let’s try to understand what should happen for the company to achieve its yearly EPS growth goal.

I put a 7% decline in revenue for this year, and then a growth from 2024 to 2026 of 4%. Keeping the operating ratio always at 59% and net margin at 32% and considering buybacks around C$4 million I tried to forecast what the future EPS should be from 2024 to 2026.

Author, with past data from CNI Annual Reports

In my forecast, I get a slower EPS growth than the 10% set by the management as the lower bound of the target the company intends to achieve. This means that according to my model, the company is trading at a fwd 2024 PE of 18.2 and a fwd 2026 PE of 15.5. But if the company achieves its targets, it is now even cheaper.

In addition, Canadian National has always been very conservative with its balance sheet. Now that many of its peers are pulling back on share repurchases because of more leveraged balance sheets, this company is able to keep up a huge buyback program which will significantly reduce its total outstanding shares.

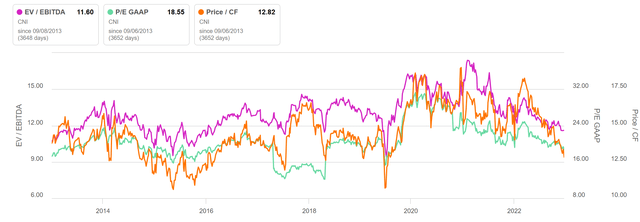

Right now, the company trades at a PE of 18.55, which is back to its pre-pandemic range. Under the EV/EBITDA perspective we have a score of 11.6, which is near the low end of the range since 2013. Price/FCF is also going down and it is now at 12.82 which is once again rather cheap if we look at the past decade.

Seeking Alpha

True, the short-term ride for the stock might be bumpy. There will probably be a revenue decline and maybe some pressure on margins. But I have difficulty in believing the company won’t have any future. I actually believe there will be even more need for its operations and this is why I am increasing my stake in the company.

Read the full article here