Thesis

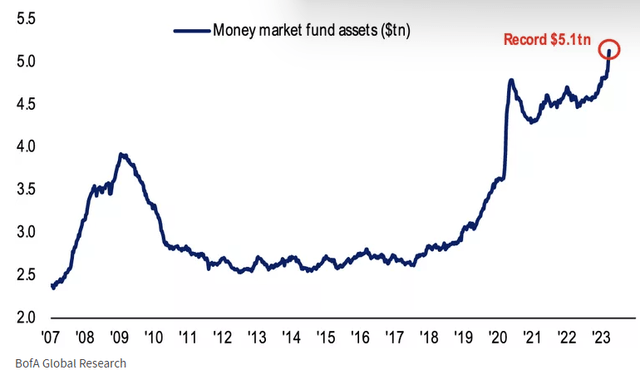

With rates above 5%, money market funds have attracted enormous inflows this year:

MM Funds (BofA)

Outside of short dated instruments, traditional bond funds are finally providing decent yields, and in this article we are going to have a closer look at the JPMorgan Core Plus Bond ETF (BATS:JCPB), a multi-asset fund from JPMorgan. The vehicle has current income as its primary purpose, and tends to focus on investment grade bonds, although it does have a small 15% sub-investment grade bucket.

In this article we are going to look at JCPB, its build and analytics, its yield in comparison with competing funds, and determine whether a retail investor is well served to allocate capital here.

Analytics

- AUM: $1.4 bil.

- Sharpe Ratio: -0.84 (3Y).

- Std. Deviation: 6 (3Y).

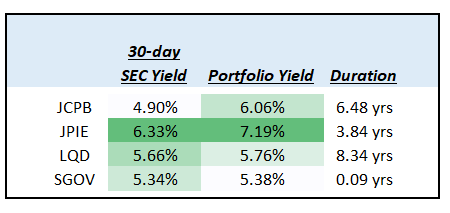

- Yield: 4.9% (30-day SEC Yield)

- Premium/Discount to NAV: n/a

- Z-Stat: n/a

- Leverage Ratio: 0%

- Composition: Fixed Income Multi Asset

- Duration: 6.4 yrs

- Expense Ratio: 0.4%

Yield Metrics

In today’s environment, especially when considering a fund for yield, it is important to understand the different metrics utilized, and their meaning:

Fund Cohort (Author)

The most important metric for current dividends is the 30-day SEC yield. This figure gives a retail investor the most accurate picture of what cash figure they will actually get. The metric is calculated by using the last dividend provided by a fund and annualizing that figure. Many financial websites present as dividend yield the trailing 12-months one, which is not accurate for a rising rates environment. That analytic presents the summation of dividends for the past twelve months, divided by the current price. If rates are much higher presently than in the past, that figure is usually much below the current 30-day SEC yield. To that end JCPB’s trailing twelve months yield is 4.15%, versus the 30-day SEC yield of 4.9%. Out of the analyzed cohort in the table, JPMorgan Income ETF (JPIE) stands head and shoulders above the rest of the funds, with a 30-day SEC yield of 6.33%. JPIE is also a multi-asset fund which we covered here, and has a 30-day SEC yield 140 bps higher than JCPB.

The second metric to look at from a yield standpoint is the ‘Portfolio Yield’. This figure gives an investor the yield to maturity for the assets in the portfolio. As time passes by, the 30-day SEC yield will move towards the ‘Portfolio Yield’. To note that our table above presents a ‘clean’ portfolio yield, where management expenses are not subtracted. We feel the best way to analyze a portfolio is on its own merits, and then management fees can be considered when choosing a ticker.

To note that short duration funds like the iShares 0-3 Month Treasury Bond ETF (SGOV) have very similar metrics in the 30-day SEC yield column and the portfolio yield one. As the portfolio ‘turns’, the 30-day SEC yield approaches the portfolio yield.

Again, the best looking fund from this cohort is JPIE, which sports the highest portfolio yield when compared to its peers. The fund does have a lower duration profile than JCPB, at only 3.84 years, but is also a multi-asset bond fund. JCPB’s portfolio yield is only 6.06%, meaning its 30-day SEC yield will never exceed that figure (all else equal in terms of rates staying at current levels).

Holdings

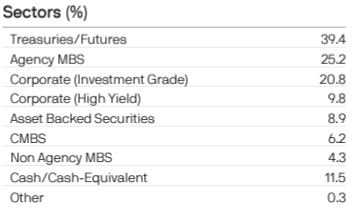

The fund has a multi-asset build:

Sectors (Fund Fact Sheet)

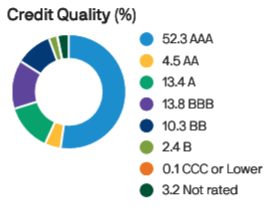

We can see that treasuries and treasury futures have the highest portfolio allocation at 39%, followed by Agency MBS and Investment Grade Corporates. This fund is overweight AAA assets, which make up over 52% of its collateral pool:

Credit Quality (Fund Website)

We can consider JCPB an investment grade fund, given that only a very small slice (sub 15%) is below investment grade. The main risk drivers therefore are rates and credit spreads.

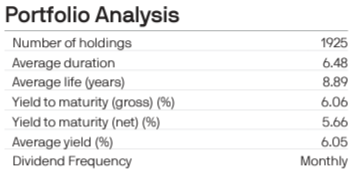

The portfolio is extremely granular, with over 1900 issuers in the collateral pool:

Portfolio Analysis (Fund Fact Sheet)

The fund has a fairly long duration of 6.4 years, reminiscent of the much better known iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD).

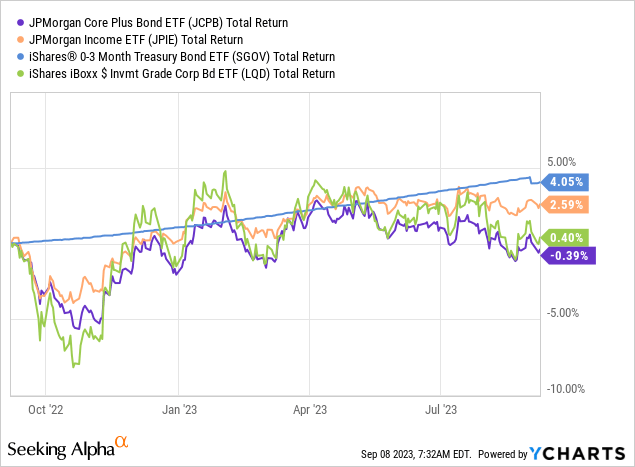

Performance

The fund is the worst performing one from the cohort on a 1-year look-back:

The analysis above is done from a total return perspective in order to include the fund dividends. The best performer has been the short duration fund SGOV, followed by JPIE and the iShares iBoxx $ Investment Grade Corporate Bond ETF. JCPB has a total return profile very similar to LQD in the past year, given their duration similarities.

What is the forward for JCPB?

With rates peaking as we speak, 2024 looks like a much better year for JCPB. The fund has a 6.4 years duration, and will start making investors money once the Fed starts cutting rates or if rates just remain at current levels. The more important question to ask though is whether JCPB is a better alternative than its peers right now.

From a 30-day SEC yield perspective it is not. A retail investor is better served by buying very short dated funds like SGOV, which have a very low duration profile and are entirely made up of AAA assets.

From a portfolio yield perspective JCPB again does not stack up when compared to the likes of JPIE, another multi-asset fund from JPMorgan. JCPB lags significantly here, and there is nothing appealing in this fund to choose it over JPIE.

From a pure rates / investment grade credit perspective LQD is slightly better, given its higher duration and only investment grade collateral composition.

While JCPB will make investors money in 2024, it just does not have any advantage over any of its peers.

Conclusion

JCPB is a fixed income exchange traded fund from JPMorgan. The fund falls in the multi-asset category, and is finally yielding above 4%, given the rise in rates. The fund has over 50% of its collateral in Treasury and Agency MBS, assets which are rated AAA. The vehicle has a small 15% sub-investment grade bucket, which in our opinion is used for yield enhancement.

However, with a 4.9% 30-day SEC yield and a 6.06% portfolio yield, the fund fails to impress. Both yields are below what competing funds offer, and do not represent a compelling choice, especially when we consider the high 40 bps expense ratio. From a multi-asset fund perspective JPIE (also from JPMorgan) looks much better here, while from a short dated high yielding angle SGOV is the better choice. Lastly, LQD is also superior when looking at a pure investment grade vehicle with a similar duration. While JCPB will make money for investors in 2024, the fund is just not a compelling choice when benchmarked against the above cohort. We are a Sell for this name, from a perspective of better capital allocation to the above mentioned names.

Read the full article here