Hello again, Seeking Alpha Community!

It has been a whopping 313 days since I wrote my last article on this platform. Today, I’ll cover one of my favorite companies on the stock market, Ulta Beauty (NASDAQ:ULTA).

In my first-ever Ulta article over a year ago, there were 3 key components of the investment thesis.

- Strong Brand & Customer Loyalty

- Growing Store Count & Same Store Sales

- Stellar Financials

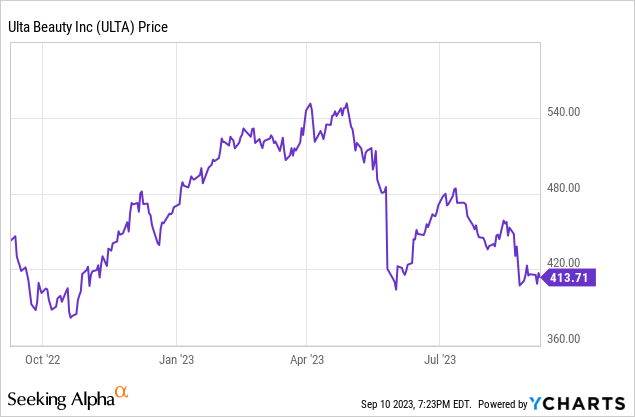

Since publishing my first article on Ulta, the stock price has remained relatively flat. However, during that time, the company hit all-time highs of over $540 prior to pulling back.

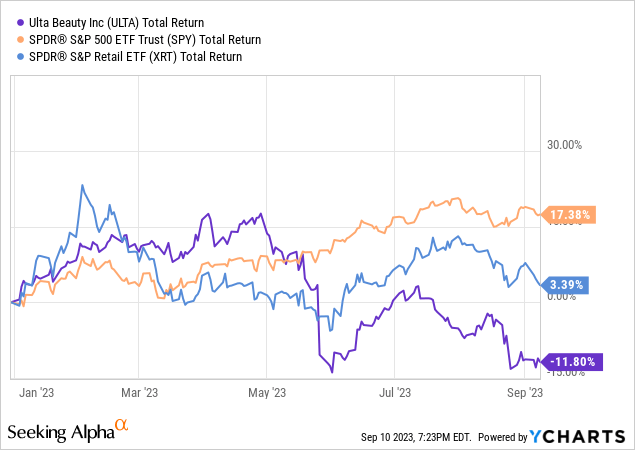

Ulta is down around 12% YTD, while the broader market indices (SPY) are up 17% YTD. Furthermore, the S&P 500 Retail ETF (XRT) is up 3% on the year, leading to an underperformance from Ulta on both fronts of 29% and 15%, respectively. Since its first quarter earnings release, ULTA has lost a quarter of its value.

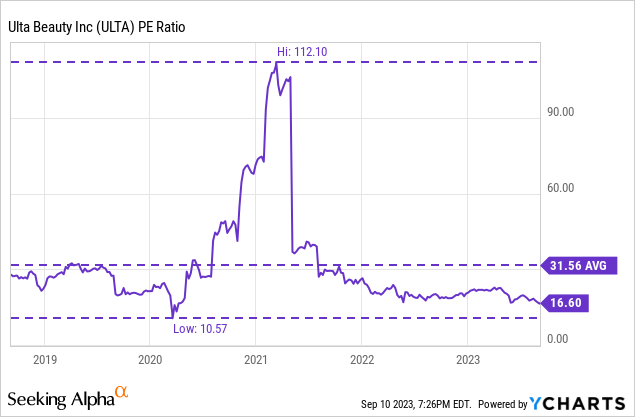

While investors of late likely are disappointed with the beauty retailer’s performance, its long-term prospects still remain intact, especially at its current valuation of 16x earnings.

In this article, I’ll dissect Ulta Beauty’s fundamentals and revisit my initial three thesis points from my first article. Also, I will be taking a look at why the bears have been selling this stock off in light of its most recent two-quarters of earnings.

Strong Brand Reputation & Customer Loyalty

As America’s largest specialty beauty retailer in the United States, Ulta Beauty boasts over 1,350 stores across the US sporting over 600 beauty brands comprising over 25,000 products.

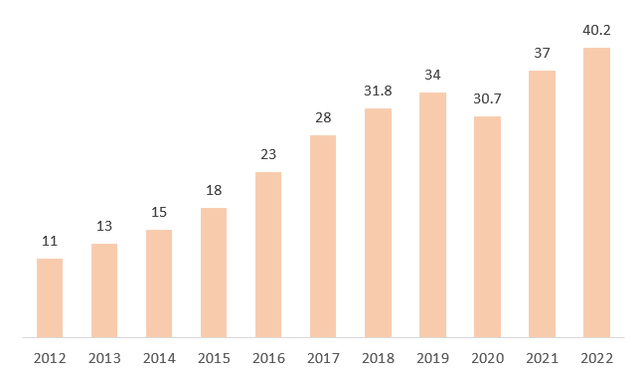

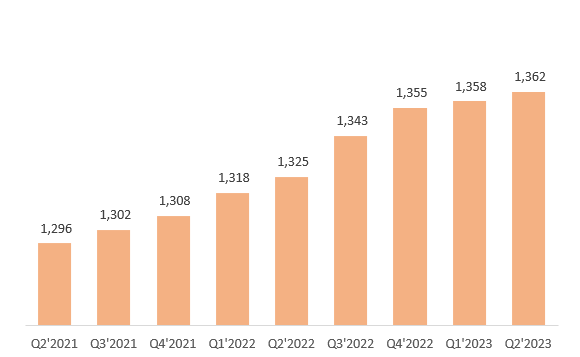

Boasting a whopping 40 million “Ultamate Reward” loyalty members in year-end 2022, Ulta’s brand reputation continues to be a linchpin of the company’s overall success. The below chart demonstrates Ulta’s ability to consistently grow its active loyalty member base. Following COVID-19 struggles, the retailer was able to grow its member base by 31% from 2020 – 2022.

Loyalty Members (Millions) (Author Created)

More impressively, a staggering 95% of Ulta’s revenue is derived from their loyalty members. With Ulta’s investment in its omnichannel growth, specifically e-commerce, the beauty retailer has cultivated a loyal and cult-like consumer base. In short, customers who spend at Ulta Beauty once are likely to be customers for life.

On the supply side of the equation, Ulta continues to onboard new, well-renowned brands such as Bubble, BYOMA, and Beautycounter, while fostering innovation and product growth from existing brands. Effectively, Ulta has created a competitive ecosystem where cosmetics and beauty brands vie for valuable shelf space within Ulta stores.

Growing Store Count & Same Store Sales

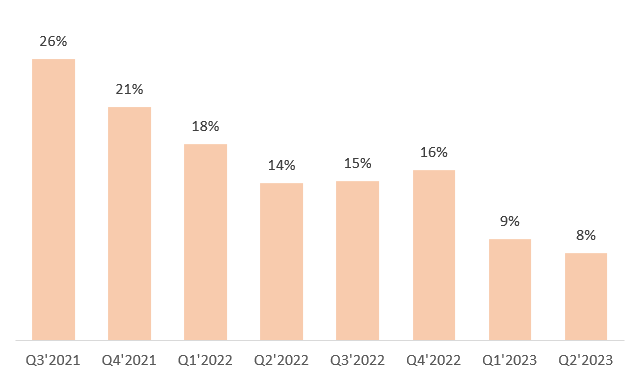

Since its inception, Ulta has stayed true to its store growth goals and has consistently continued to deliver on its promises. In fiscal year 2022, Ulta Beauty opened 47 net new stores, with no store closures. The chart below depicts the last 9 quarters of store growth for Ulta Beauty.

Author Created

Although comparable sales experienced a sequential decline in the first and second quarters of 2023, these figures remained strong at 9.3% and 8%, respectively. This acts as a positive signal to investors that the beauty retailer is not relying solely on its store count to bolster its top-line growth.

Author Created

The decline in comparable sales on a QoQ basis in 2023 is due to the unprecedented growth Ulta experienced post-COVID in 2021 and 2022. Ulta’s historical comparable sales over the last 10 years have been in the high single digits and low double digits, on par with its recent quarterly figures.

The twin engines fueling Ulta’s growth continue to be opening new stores while driving revenue growth and operational efficiencies within its existing store base.

Stellar Financials – Have Faith in Sales Growth

Despite short-term headwinds, Ulta’s financial position remains strong.

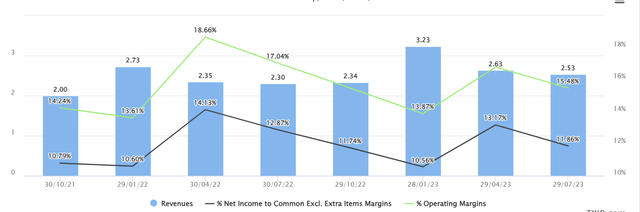

Tikr

As depicted above, Ulta continues to exhibit robust top-line growth on a quarter-over-quarter basis. The decrease in net and operating margins is a result of investments Ulta is making into its business to improve its operational efficiencies.

Causes for Concern?

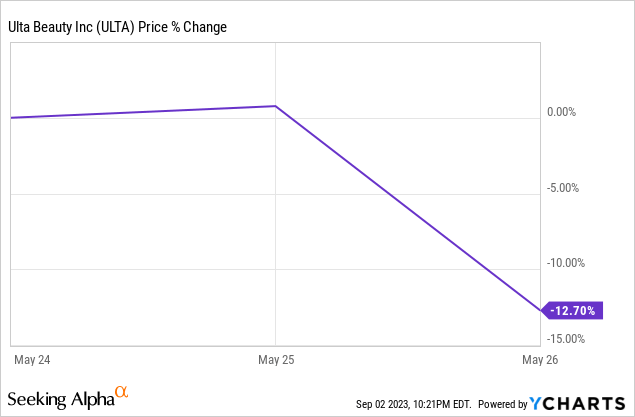

The last two quarterly earnings had the bears rapidly selling off Ulta stock. In Q1, Ulta Beauty declined by 13% following the earnings release.

Despite beating revenue expectations, concerns arose around profitability, specifically the decline in operating margin.

CFO Scott Settersten commented on the decrease:

Operating margin was 16.8% of sales, compared to 18.7% of sales in the first quarter of 2022. As expected, the decline in operating margin primarily reflects the impact of SG&A deleverage and lapping our extraordinary results in the first quarter of fiscal 2022.

In the 2nd quarter earnings call, management also alluded to potential negative EPS Growth in Q3 due to lower operating margins.

Mr. Settersten also commented, stating that:

Operating margin is going to be down significantly — you know, meaningfully versus what we saw earlier this year. And that’s going to result in, you know, negative EPS growth year over year for the third quarter.

With ULTA’s investments into its IT infrastructure and Enterprise Resource Planning through its Project SOAR initiative, management noted that this is the key reason that SG&A will see an incremental increase YoY, thereby putting pressure on its operating margin.

Furthermore, management also portrayed a level of uncertainty for Fiscal Year 2024 by not providing guidance to shareholders during this transitionary phase. CFO Scott Settersten advised investors that ULTA’s project initiatives should start to yield fruit in 2024 and beyond.

Yeah, and you’re exactly right. We’re not providing guidance for 2024 here today, but yeah, investors should expect that we will cultivate, recoup benefits from the significant investments that we’re making in our core systems here in ’22 into ’23 and that we’re going to see benefits materialize in 2024 and beyond. Again, you’ve heard us talk about these are major initiatives here that we expect to pay dividends for a number of years into the future. But I would — you know, I’d also caution investors, just to be prepared.

As depicted by the management excerpts above regarding uncertainty and unwillingness to provide guidance for 2024, ULTA’s stock price quickly declined from its all-time highs earlier in the year.

Trust the Management Team – Target Partnership

Historically, Ulta’s management team has demonstrated a consistent track record of achieving goals, objectives, and timelines. Thus, with management alluding to short-term pressure on operating margins and profitability due to ongoing investments into the business, this should not be a cause for concern for long-term investors.

In November 2020, Ulta announced its partnership with Target (TGT) to expand its retail presence in the US beauty market through a shop-in-shop concept.

The distinctive, branded shop-in-shop will operate as an extension of the welcoming Ulta Beauty experience, mirroring the retailers’ existing stores and designed to discover established and emerging prestige brands. With approximately 1,000 square feet of retail space, Ulta Beauty at Target will be prominently located next to the existing beauty section.

As of Fiscal Year 2022, Ulta had a presence in over 350 Target locations across America, with a long-term goal of 800 Target locations. As it stands, Ulta is well on track to hit its long-term shop-in-shop projections, achieving almost 50% of its target in the first two years.

Is the Thesis Still Intact?

While it has been a rocky start for Ulta in 2023, the long-term prospects and fundamentals of the business remain strong.

1. Strong Brand & Customer Loyalty

Despite short-term headwinds, Ulta continues to grow its loyalty membership count for the tenth consecutive year. Its strong brand awareness and loyalty act as a moat around Ulta’s business through network effects and intangible asset value (through its brand).

2. Growing Store Count and same-store sales

Ulta’s management team has continued to expand its store count and generate positive comp sales YoY and QoQ. An increase in its store count and comparable sales continue to act as twin engines that drive Ulta Beauty’s revenue growth, confirming the long-term investment thesis.

3. Stellar Financials & Valuation

At one of its lowest valuations in 5 years, Ulta’s 16x earnings multiple makes it an attractive long-term investment. Coupled with its debt-free balance sheet and robust top-line growth, Ulta Beauty looks more attractive than ever.

Thus, for the reasons outlined above, I will be instituting a “Buy” recommendation on Ulta Beauty. While short-term headwinds and pressure on its operating and gross margins may cause short-term declines in its stock price, Ulta remains poised for long-term growth and success as America’s leading beauty retailer.

Read the full article here