Intro

We wrote about Mayville Engineering Company, Inc. (NYSE:MEC) back in May of this year when we stated that momentum (regarding profitability) needed to continue in the company in earnest. Although the company’s Military, Powersports, and commercial vehicle segments demonstrated underlying top-line strength in the first quarter, profitability still looked constrained which saw Q1 GAAP EPS earnings of $0.12 per share miss estimates by a lofty $0.09 in the quarter. Suffice it to say, that when we tied in Mayville’s profitability trends, its valuation, and technical chart action, our rating three months ago for the company remained a ‘Hold’. Shares are down just over 14% since our post-Q1 commentary.

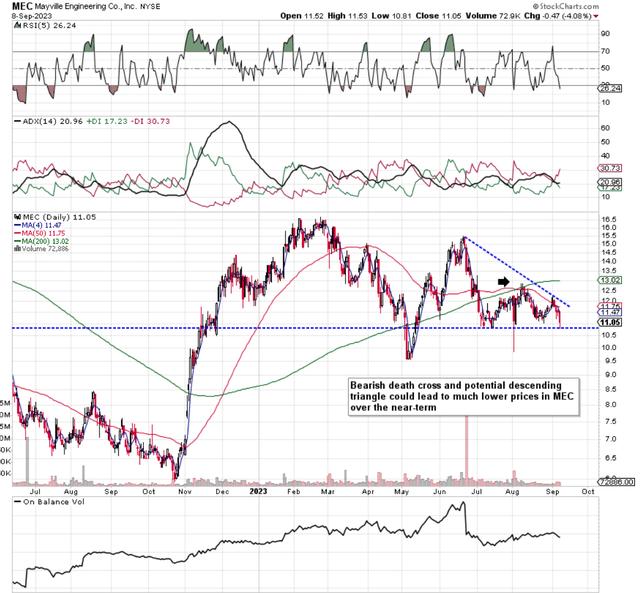

Unfortunately, Mayville reported a consecutive earnings miss in Q2 (GAAP earnings of $0.08 per share) on the 5th of August, where shares have continued their pattern of lower lows in the aftermath. Furthermore, the Q2 earnings miss precipitated a technical death cross (bearish crossover of the stock’s 50-day moving average below its corresponding 200-day moving average) so investors who remain long need to prepared for lower prices over the near term. Furthermore, with the contraction of volume over the past 10 weeks or so, we have seen lower highs in Mayville with support around the $11 level remaining firm. If this support level were to fail, however, the height of the triangle ($4+ per share) demonstrates that there would be plenty of downside risk in BEC if indeed the potential descending triangle (bearish) were to play itself out in full.

MEC Technical Chart (Stockcharts.com)

Q2 Earnings

The reported Q2 bottom-line miss primarily came about as a result of ongoing supply-chain headwinds & elevated costs including the ramp-up of the company’s Hazel Park manufacturing facility & various product launches. It is interesting though (despite MEC’s constrained profitability at present) that the market (being a predictive mechanism that is always attempting to ascertain future market conditions) has yet to price in more favorable market conditions going forward. We state this because Hazel Park (once 100% up and running) is expected to increase MEC’s EBITDA number by up to $20 million on an annual basis. Moreover, other investments such as the recent Mid-States Aluminium purchase are expected to make further inroads in the commercial vehicle & power sports segments but at what cost is the question.

Suffice it to say, although Mayville can continue to do everything possible on the front to improve its ‘value proposition’, the jury is still out on whether sustained demand will be there across all segments which would increase earnings meaningfully. We can already see this in the company’s forward-looking EPS revisions. Mayville’s fiscal 2023 EPS estimate of $0.76 per share has been dialed back by 27% over the past three months. The company’s fiscal 2024 estimate of $1.15 has been dialed down by 16% over the same period.

Growth Concerns

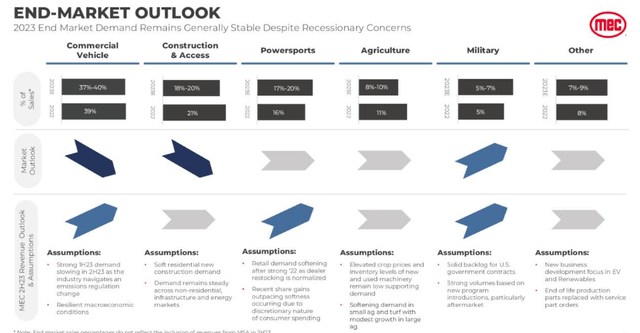

Although for example, the company’s Powersports & Military segments continue to report impressive growth rates (7.2% & 66% respectively in Q2), the faster growing Military segment only makes up approximately 7% of Mayville’s earnings whereas the Powersports segment makes up less than 20%. Suffice it to say, the lion’s shares of Mayville’s revenues stem from its Commercial Vehicle segment as well as its Construction and access segment (Almost 60% combined of the company’s sales number) so strength will continue to be needed here for some time to come until Mayville’s smaller segments can make up a bigger piece of the company’s revenues. Unfortunately, weakness is expected in the ‘Commercial Vehicle’ space as well as ‘Construction & Access’ over the latter part of the year due to regulatory changes & elevated interest rates respectively as we see below.

Mayville Q2 Earnings Presentation (Seeking Alpha)

Therefore, although Mayville may be trading with an extremely attractive valuation (forward book multiple of 1.6 & forward sales multiple of 0.38), investors need to take into account the company’s worrying technicals as well as the end-market outlook of the company’s largest markets. Furthermore, given that leverage has increased significantly at Mayville due to recent investments, the market will need to see the fruit of these investments before long in order to price shares higher over time.

Conclusion

Therefore to sum up, although shares of Mayville are down close to 13% year to date (which has made the valuation of the stock more compelling), we recommend that investors (due to lower demand and aligned technicals) do not add to long positions at this moment in time. We look forward to continued coverage.

Read the full article here