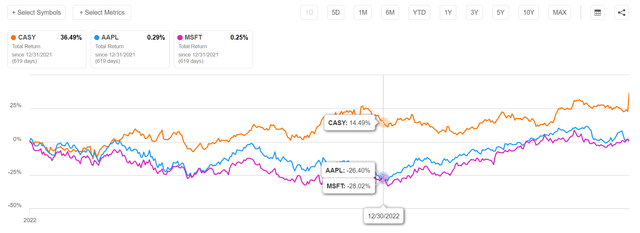

Quick, name a company that rallied 14% in 2022 and is up 21% YTD 2023. Is it Apple Inc. (AAPL)? Is it Microsoft Corp (MSFT)? No, it’s actually the convenience store operator, Casey’s General Stores, Inc. (NASDAQ:CASY) (Figure 1).

Figure 1 – Casey’s has outperformed AAPL and MSFT since end of 2021 (Seeking Alpha)

This little known convenience store operator has been able to beat market darlings like Apple and Microsoft since the end of 2021, and it shows no signs of slowing down, recently soaring 11% on the release of its Q1/F24 results. How good were these results and what’s in store for Casey’s in the future?

Casey’s General Stores Overview

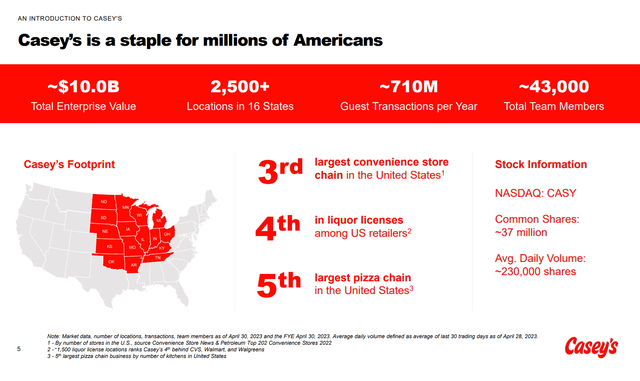

First, for those not familiar with Casey’s, the company is the 3rd largest operator of convenience stores in the U.S., with more than 2,500 stores in the U.S. Mid-Western states (Figure 2). However, what many readers may not know is that Casey’s is also the nation’s 4th largest liquor store and 5th largest pizza chain.

Figure 2 – Casey’s overview (Company’s investor presentation)

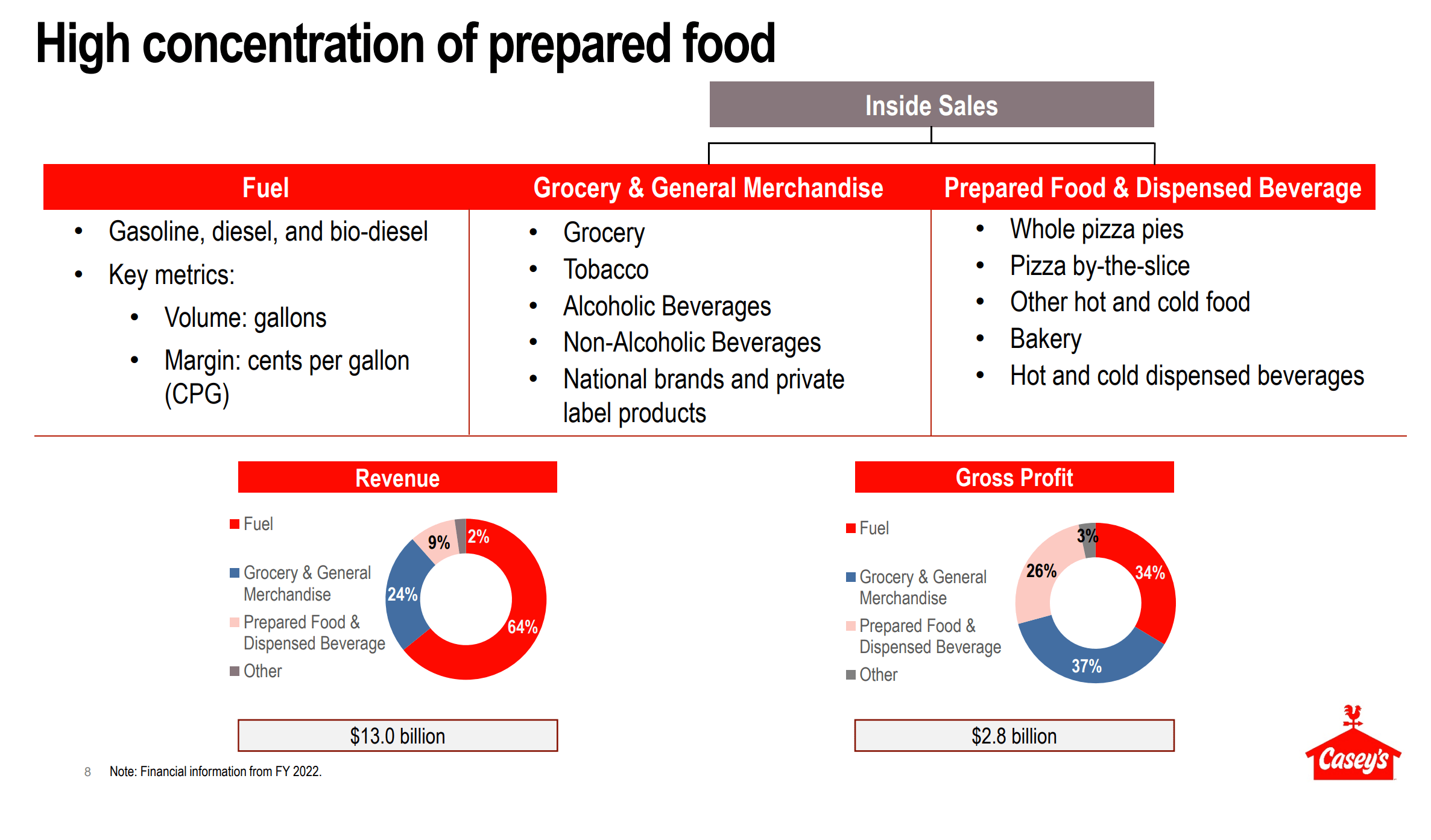

A key differentiating factor in the Casey’s story is that more than 50% of the company’s stores are located in rural towns with 5,000 people or less, so in addition to selling fuel, Casey’s also plays the role of grocery and general merchandise stores as well as fast food restaurants. This leads to Casey’s having a higher share of gross profit dollars from inside sales, and better gross margins than competitors. For Casey’s, approximately 2/3 of gross profit dollars are generated from inside sales (Figure 3).

Figure 3 – Casey’s derive 2/3 of gross profits from inside sales (Company investor presentation)

Casey’s also owns its own distribution centers (3 DCs provide most of Casey’s inside store goods), allowing the company to have better control over its value-chain and squeeze out additional operational efficiencies (Figure 4).

Figure 4 – Casey’s is vertically integrated with its own distribution centers (Company investor presentation)

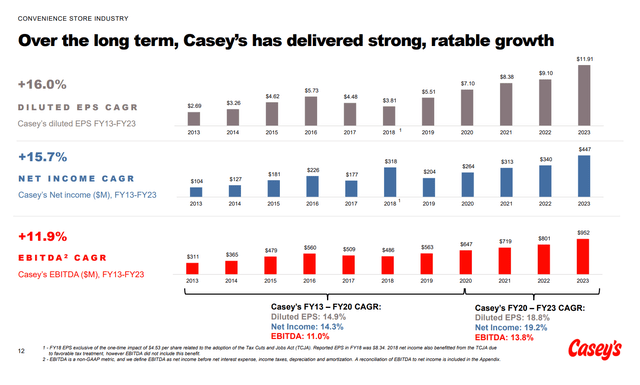

This has resulted in peer-leading financial performance, with Casey’s delivering consistent double-digit growth in EBITDA and earnings in the past decade (Figure 5).

Figure 5 – Casey’s has delivered consistent earnings growth (Company investor presentation)

I initiated on Casey’s last year, and readers may want to refer to that article for additional information on Casey’s.

Casey’s Q1 FY24 Results – Yet Another Financial Beat

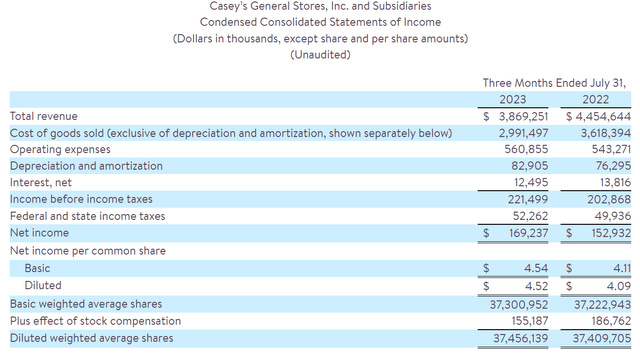

Recently, Casey’s reported its first quarter results for fiscal 2024, with revenues of $3.87 billion (-13.0% YoY) and dil. EPS of $4.52 (+10.5% YoY) (Figure 6). Revenues for Casey’s are dependent on fuel prices and can be volatile, but earnings were notably strong, beating consensus estimates by $1.19 / share.

Figure 6 – Casey’s Q1/F24 financial results (Company press release)

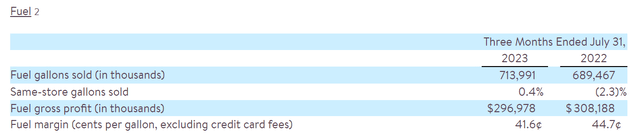

Operationally, Casey’s earnings beat was driven by a number of factors. First, fuel margins were strong, at 41.6 cents / gallon, compared to management’s guidance of mid-30s despite a steep decline in fuel prices from $4.49 in the year-ago period to $3.40 per gallon in Q1/F24 (Figure 7). Casey’s also sold 3.6% YoY more fuel this quarter.

Figure 7 – Fuel margins were strong (Company press release)

Inside sales were also strong, with a 5.4% YoY increase and a 12.1% 2-yr stacked growth rate with a 40.6% gross margins (Figure 8). The introduction of new prepared food items was called out by management for contributing to inside sales growth.

Figure 8 – Inside sales jumped 5.4% YoY (Company press release)

Furthermore, Casey’s gross margins benefited from private label goods, which offer customers a good value proposition while being margin accretive for the company (Figure 9).

Figure 9 – Private label goods helped margin (Company investor presentation)

How Long Can Fuel Margins Stay Elevated?

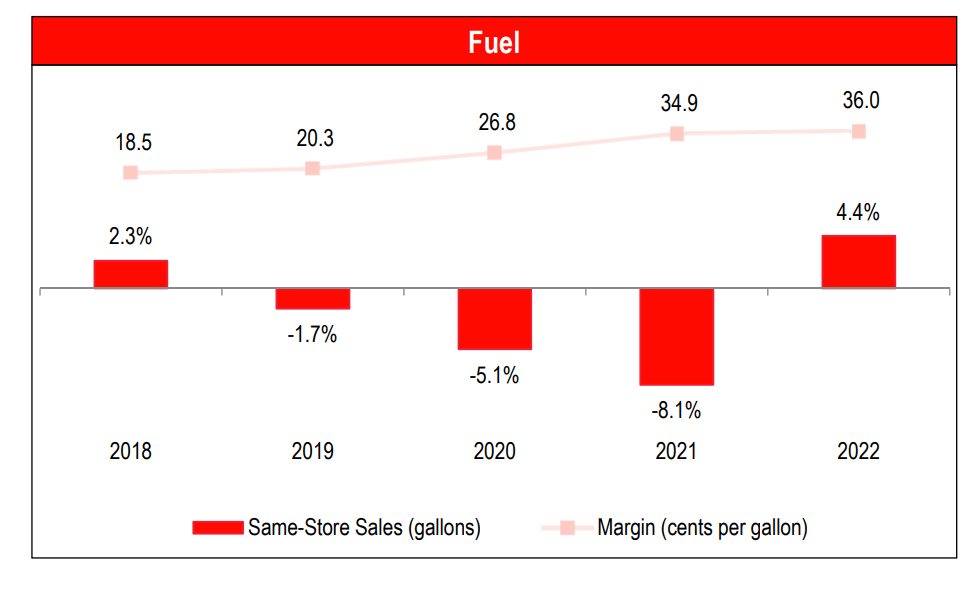

In my initiation article, I noted that tight supply/demand dynamics have been the main driver for higher fuel margins, as refining capacity had been taken offline in the U.S. due to environmental concerns in the last few years. This has helped push fuel margins up from the ~20 cent / gallon level to mid 30 cents range since 2020, and recently to the 40 cent range (Figure 10).

Figure 10 – Fuel margins have expanded on tight supply/demand dynamics (Company investor presentation)

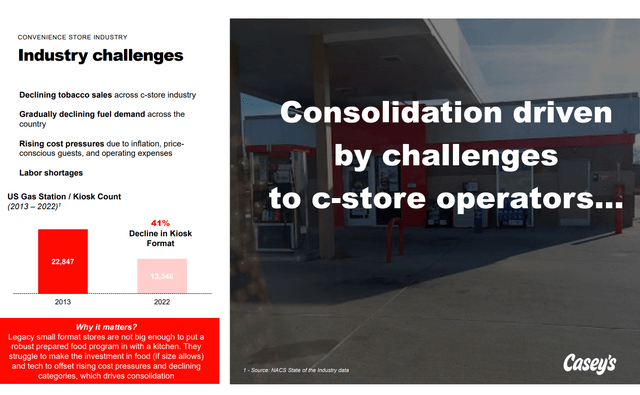

Furthermore, the decline of tobacco sales and limited inside sale categories have pressured the profitability of mom and pop convenience stores, forcing them to raise fuel prices to compensate (Figure 11). This has indirectly benefited large chains like Casey’s that have large format stores with attractive inside sales margins.

Figure 11 – Convenience store industry challenged by changing consumer patterns (Company investor presentation)

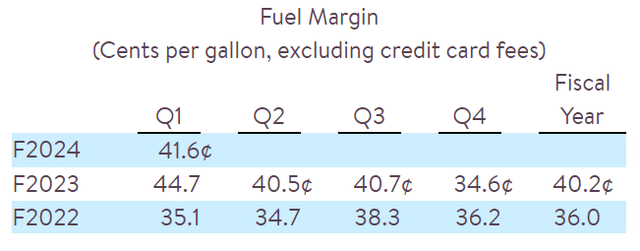

For fiscal 2024, Casey is guiding to fuel margins in the mid-30 cents, but recent results suggest they may stay elevated above that level. In fact, fuel margins have stayed above 34.6 cents for a record 9 straight quarters for Casey’s, significantly contributing to the company’s strong profitability (Figure 12).

Figure 12 – Casey’s fuel margins have stayed elevated for 9 quarters (Company press release)

While management has been coy about the sustainability of 40 cents+ fuel margins, there does not appear to be any near-term impetus for margins to return to historical sub-35 cent levels.

M&A Contributing To Growth

Another reason Casey’s jumped following the quarter was because Casey’s updated markets on the number of stores it is currently acquiring to 125, including 63 previously announced from EG group.

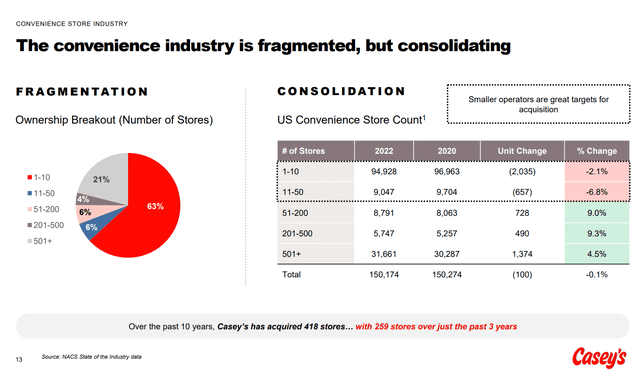

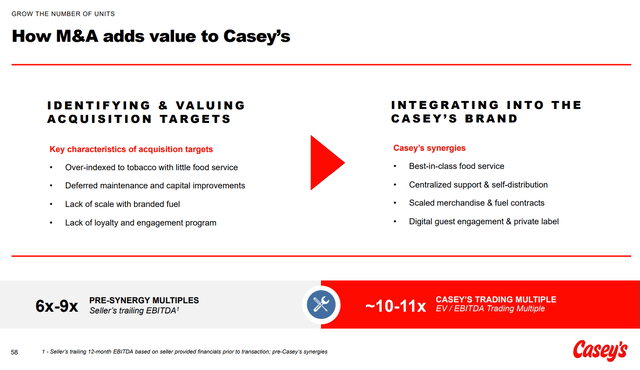

M&A has been a core part of Casey’s growth formula in recent years, as Casey’s is a natural consolidator within the fragmented convenience store industry (Figure 13).

Figure 13 – Convenience store industry ripe for consolidation (Company investor presentation)

Casey’s targets chains that are over-indexed to tobacco, with little food service offerings, and lack scale and capital. Casey’s is then able to acquire these units at a 6-9x pre-synergy EBITDA multiple, and after spending capital to remodel the stores, is able to get a valuation uplift to Casey’s 10-11x trading multiple (Figure 14).

Figure 14 – M&A adds value to Casey’s (Company investor presentation)

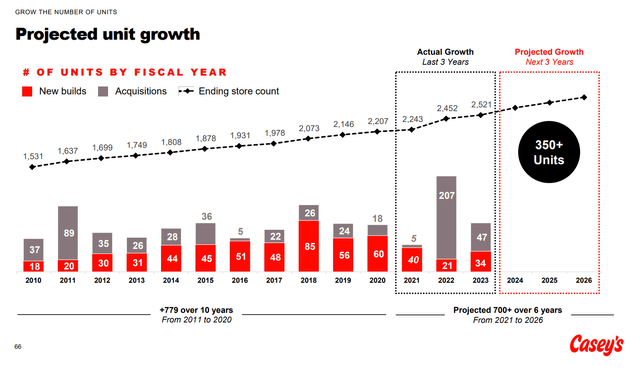

Overall, the company is guiding to growing units by 350 stores over the next 3 years, and with the deals in place, Casey’s is well on its way to surpassing those goals (Figure 15).

Figure 15 – Casey’s is guiding to add 350 stores in next 3 years (Company investor presentation)

Financials Are Setup For Beat-And-Raises

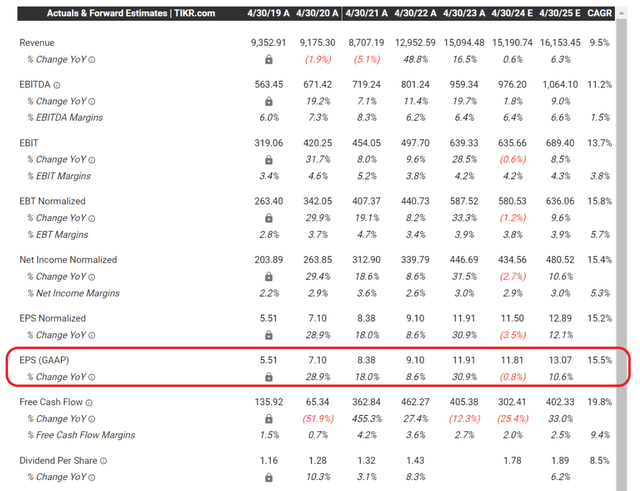

Looking forward, analysts are actually estimating a flat year in terms of EPS growth, from $11.91 in fiscal 2023 to $11.81 in fiscal 2024 (Figure 16).

Figure 16 – Wall Street estimates call for flat earnings growth (tikr.com)

However, given Casey’s strong Q1 results ($4.52 in dil. EPS, 10.5% YoY growth), Wall Street’s $11.81 / share F2024 figure seems very “beatable.”

In fact, with the company expected to add 150 stores (6% unit growth) in fiscal 2024, there is a very high likelihood that 2024 results could be much closer to analyst’s fiscal 2025 estimate of ~$13 / share.

But CASY Stock Valuation Is Elevated

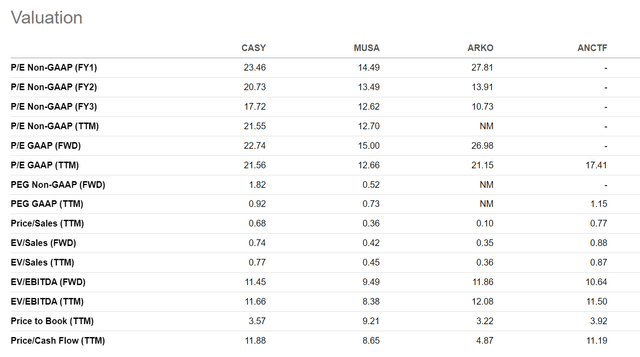

If there are any drawbacks to the Casey’s story, it is valuation. The company is currently trading at 21.6x trailing GAAP P/E, significantly higher than convenience store peers like Murphy USA Inc. (MUSA) and Alimentation Couche-Tard (OTCPK:ANCTF), and in line with Arko Corp. (ARKO) (Figure 17).

Figure 17 – Casey’s valuation is elevated compared to convenience store peers (Seeking Alpha)

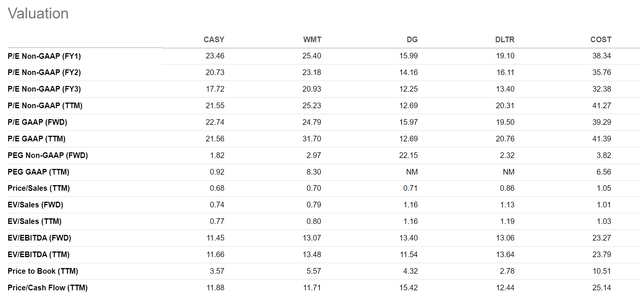

However, given 2/3 of Casey’s gross profits come from inside sales, perhaps investors should value Casey’s against retailing peers like Walmart (WMT), Dollar General (DG), Dollar Tree (DLTR), and Costco (COST) (Figure 18). Against this peer group, Casey’s valuation looks more sensible.

Figure 18 – Casey’s valuation is more reasonable compared to general merchandisers (Seeking Alpha)

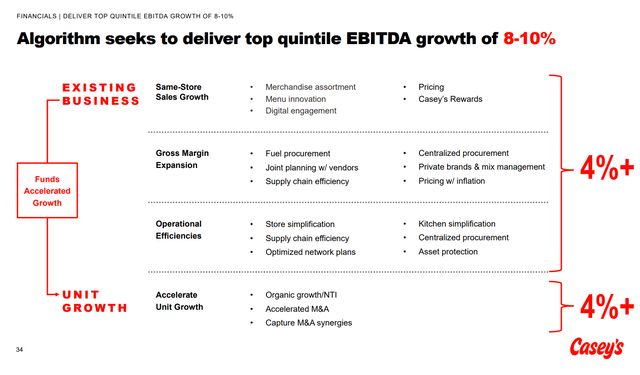

I believe Casey’s can maintain its elevated valuation multiples as long as fuel margin stays strong and Casey can continue to deliver on inside sales growth. With the market itself trading at a 20.2x Fwd P/E multiple, it is not a stretch for Casey’s to trade at 23.5x Fwd P/E, given its algorithm of targeting 8-10% long-term EBITDA growth and mid-teens EPS growth (Figure 19).

Figure 19 – Casey’s has an attractive growth algorithm (Company investor presentation)

Risks To Casey’s

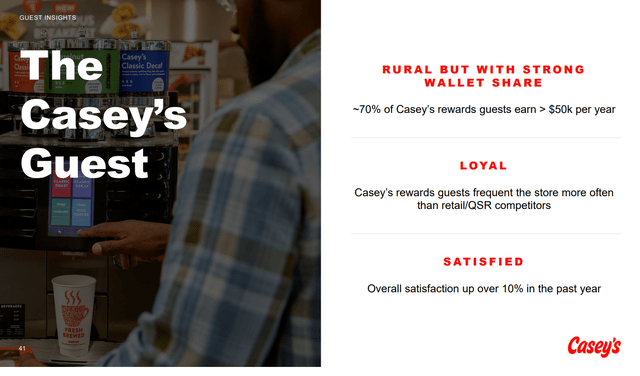

There are a number of risks to Casey’s that investors should be aware of. First, while inside sales growth have been strong, consumers are increasingly being squeezed in their pocketbooks from inflation. With the upcoming restart of student loan repayments, consumers may be less inclined to spend, especially those in the lower income cohorts. Fortunately, Casey’s is not overly indexed to low income consumers, as the company believes more than 70% of its customers make more than $50k per year (Figure 20).

Figure 20 – Casey’s is not overly exposed to low income consumers (Company investor presentation)

Another risk to Casey’s is fuel margins, which have stayed elevated in the past few years. With President Biden heading into a tough re-election campaign, investors should be prepared for heightened political rhetoric of “price gouging by energy companies,” especially if fuel prices start to rise in the coming months.

Finally, investors should note that Casey’s has deviated from its tradition of adding stores organically, with several large transactions completed in recent years. While large M&A transactions can add many stores at once, it also adds execution risk, as well as the risk of Casey’s overpaying.

Conclusion

Casey’s remains an extremely well-oiled machine (pardon the pun), consistently delivering double-digit earnings growth over the past decade. Investors have rewarded the company with a 23.5x Fwd P/E multiple, near the high end of peers. I believe Casey’s is a classic GARP story with consistent low single-digit unit growth, mid single-digit same store sales growth, and double-digit earnings growth. I rate Casey’s a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here