Introduction

ORIC Pharmaceuticals (NASDAQ:ORIC), a clinical-stage biopharmaceutical company, is dedicated to addressing drug resistance in cancer. Their clinical portfolio includes ORIC-114 for EGFR and HER2 mutations, ORIC-533 targeting CD73 to enhance chemotherapy and immunotherapy, and ORIC-944 for advanced prostate cancer. They are also engaged in early-stage projects to combat various other cancer resistance mechanisms.

The following article discusses ORIC’s financial health, promising pipeline targeting drug resistance in cancer, and investment potential. It recommends a “Buy” while acknowledging inherent risks.

Q2 Earnings Report

Looking at ORIC’s most recent earnings report, the company holds $273.7M in cash and equivalents, expected to last until late 2025. R&D expenses rose to $18.8M for Q2 2023, up $5M from the same quarter last year, mainly due to product advancement and personnel costs. G&A expenses dropped slightly to $6.2M this quarter, a decrease of $0.7M, primarily attributed to reduced professional fees.

Cash Runway & Liquidity

Turning to ORIC’s balance sheet, the company had cash and cash equivalents of $103.7M, short-term investments of $160.5M, and long-term investments of $9.6M, summing up to a total of $273.7M in highly liquid assets. The “Net cash used in operating activities” for the first six months of 2023 was $41.8M, yielding a monthly cash burn rate of approximately $7M. Calculating the cash runway, the firm has about 39 months, assuming the current burn rate persists. However, this is based on past data and may not accurately reflect future performance.

The company appears to have a strong liquidity position with $273.8M in liquid assets and only $23M in total liabilities. ORIC does not show any substantial debt on its balance sheet. Given its substantial liquid assets and relatively low cash burn, securing additional financing, if needed, appears plausible, though the company’s existing resources seem robust for the foreseeable future. These are my personal observations, and other analysts might interpret the data differently.

Capital Structure, Growth, & Momentum

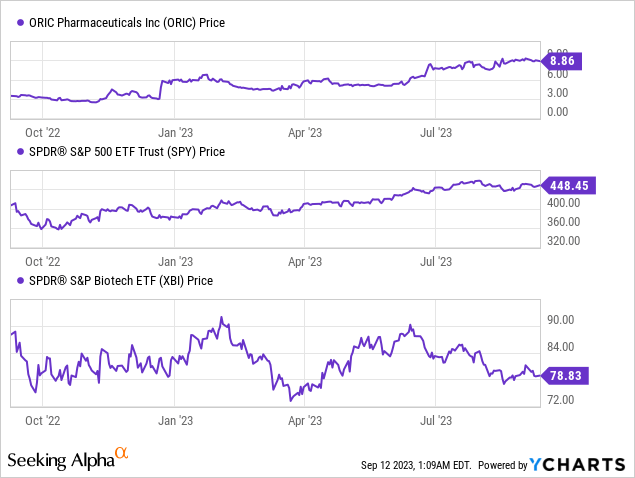

According to Seeking Alpha data, ORIC exhibits a balanced capital structure with a market capitalization of $490.52M and modest debt levels. The high cash reserves relative to debt imply a strong liquidity position. Enterprise value stands at $237.55M. The company is in the clinical-stage, focusing on drug resistance in cancer; thus, its absence of sales and negative EPS are not alarming but rather typical. In terms of stock momentum, ORIC has been on a strong upward trajectory over the past year, vastly outperforming the S&P 500.

A Robust Pipeline with Promising Drug Candidates

ORIC has a robust pipeline featuring three primary drug candidates. The first, ORIC-114, is an irreversible EGFR/HER2 inhibitor currently undergoing a Phase 1b trial for treating advanced solid tumors. Notably, its irreversible action allows for sustained target engagement, potentially offering improved therapeutic outcomes compared to reversible counterparts like Lapatinib. This drug also stands out for its brain-penetrating capability, enabling it to address hard-to-treat CNS metastases. The Phase 1b trial is unique in including patients with asymptomatic CNS metastases, either treated or untreated, making ORIC-114 potentially more adaptable and potent in its category. The company plans to present two abstracts at the upcoming ESMO Congress, which could provide further insights into its effectiveness.

The second drug, ORIC-533, is an oral inhibitor targeting CD73. It’s currently in a Phase 1b trial for patients suffering from relapsed or refractory multiple myeloma. ORIC-533 aims to improve responses to chemotherapy and immunotherapy, and initial data is eagerly anticipated in the fourth quarter of 2023.

Lastly, ORIC-944, an allosteric inhibitor of PRC2, is in a Phase 1b trial focusing on advanced prostate cancer. This inhibitor may offer new avenues for treating this type of cancer, and preliminary data is expected to be released in the first quarter of 2024.

My Analysis & Recommendation

In sum, ORIC Pharmaceuticals shows signs of being an enticing investment, especially given its early-phase pipeline with standouts like ORIC-114. ORIC’s strategic concentration on dismantling drug resistance in multiple forms of cancer sets it apart as a unique investment opportunity. Moreover, investments from biotech giants like Pfizer (PFE) and respected institutional investors such as Millennium Management, EcoR1 Capital, and Boxer Capital, add a layer of credibility to ORIC’s endeavors.

However, it’s crucial for investors to temper enthusiasm with caution. The company is in the clinical stage, meaning its pipelines are far from commercial realization. Efficacy must be proven in increasingly rigorous clinical trials, and any setbacks could take a toll on the stock price. Given that analyst revenue projections are currently unavailable, the risk profile is high. Investors should look forward to key data readouts from Phase 1b trials for ORIC-114 and ORIC-533, particularly at the upcoming ESMO Congress and in Q4 2023, respectively.

From a financial standpoint, ORIC is well-capitalized, with a cash runway stretching into late 2025. The company has managed its finances wisely, given its relatively low monthly cash burn rate, which leaves ample room for R&D investment. Still, the burn rate could increase as the pipeline progresses through clinical trials, so continued financial diligence is crucial.

My investment recommendation is “Buy.” Despite the inherent risks associated with early-stage biotech companies, ORIC’s promising pipeline, strong financial position, and backing from credible investors make it a compelling investment opportunity. Keep a close eye on upcoming clinical data and be prepared to reassess should any red flags emerge.

Risks to Thesis

While ORIC Pharmaceuticals presents a compelling investment case, several risks may contradict my “Buy” recommendation. Firstly, the clinical trials are in early stages; Phase 1b data isn’t necessarily indicative of future success in more rigorous trials. Efficacy has yet to be proven. Secondly, ORIC’s specialization in overcoming drug resistance could pigeonhole it, making diversification difficult. Thirdly, although R&D expenses increased mainly due to product advancement, escalating costs could strain resources if the cash burn rate rises unexpectedly. Lastly, positive stock momentum can be a double-edged sword: high expectations are built into the stock price, which leaves little room for error. Monitoring clinical trial results is crucial for recalibrating investment thesis.

Read the full article here