Investment action

Based on my current outlook and analysis of Luminar Technologies (NASDAQ:LAZR), I recommend a buy rating. LAZR continues to stay on track toward meeting its milestone and has reiterated its guidance for positive non-GAAP gross profit in 4Q23 and >100% revenue growth. Both the commercialization and R&D efforts are also making good progress. I believe the valuation today provides a very attractive risk-reward situation if the business can hit its FY30 targets as stated in the SPAC deck.

Basic Info

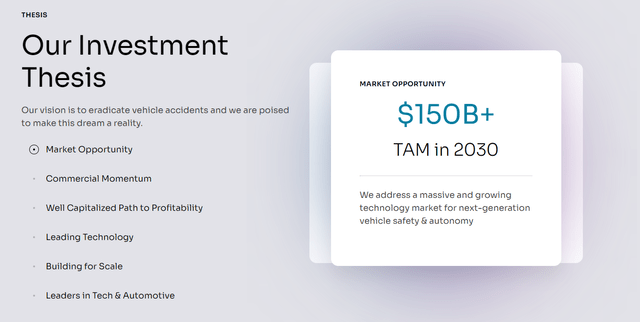

LAZR is developing solutions to become the first automotive technology company to implement fully autonomous and highly secure features across a wide range of vehicle types. LAZR was established in 2012 by Founder Austin Russell, who developed a novel lidar from the chip up. According to the homepage, the company claims to have developed a lidar sensor that grants automakers access to cutting-edge safety and autonomy systems. In terms of industry, this is a massive market expected to be worth over $150 billion by the year 2030.

LAZR

Review

The 2Q23 results for LAZR were in line with projections, and the company made significant headway toward all of its milestones. In my opinion, the best way to look at LAZR as an investment at this stage is to focus on whether the business is tracking qualitative milestones instead of the intra-quarter figures. Ultimately, whether the business is worth a lot more or less depends on them delivering the end product that they are heavily investing in R&D today. Thus, although I recognize that management may fall short of their 4Q23 target of positive non-GAAP gross margin, I am not overly concerned about this being the second consecutive quarter of missed gross margin expectations. On a side note, this might lead to the stock price facing near-term pressure until LAZR shows signs of improving gross margin.

Nevertheless, I believe that the positive aspects outweigh the drawbacks. Firstly, the management has restated their guidance to attaining a favorable non-GAAP gross margin during 4Q23 and has also reiterated guidance suggesting a growth rate surpassing 100% for the FY23. Furthermore, the organization is effectively implementing its strategies with established collaborators such as Mobileye, Polestar, and Nissan. In addition, LAZR is currently engaged in the establishment of fresh partnership, such as the one with Plus for the purpose of enhancing their commercial trucking fleet. Moreover, LAZR Semiconductor Inc. is in the process of developing a new application-specific integrated circuit (ASIC), while also expanding its presence in the optical communication sector for AI/GPU systems by means of LAZR Photodetectors.

From a commercial perspective, it sure seems like LAZR is progressing well. Even on the R&D end, I am positive that LAZR can continue to enhance its offerings after listening to the J.P. Morgan Auto Conference. After acquiring mapping company Civil Maps for $6 million, LAZR is in the process of creating a mapping engine. This engine will utilize the data from LiDAR sensors to enhance maps, a significant departure from the industry’s current reliance on camera data. The potential benefits of this development are substantial, as it creates a lucrative revenue stream for LAZR. Specifically, as this mapping engine is developed in the coming years, vehicles on the road will have the capability to gather real-time data, and LAZR can collaborate with OEM partners to monetize this LiDAR data. According to management, the level of interest from OEMs has exceeded expectations, with LAZR already securing its first contract with a major OEM to jointly develop this technology.

Another noteworthy moment during the conference was the highlight that Nvidia (NVDA) is in the development of a comprehensive software suite named Hyperion, which incorporates LAZR’s LiDAR technology for Mercedes-Benz’s autonomous driving system. While I may not possess exact technical details, I interpret this collaboration as a strong endorsement of LAZR’s standing in the industry, given Nvidia’s willingness to partner with them. It’s important to emphasize that this integration specifically pertains to LAZR’s LiDAR, considering the unique characteristics of point cloud data from different LiDAR manufacturers. Consequently, I believe this positions LAZR favorably to serve as the primary reference LiDAR on the platform, given the substantial time and resources required for integrating alternative LiDAR solutions.

Regarding the delayed launch of Volvo’s EX90, I perceive it as an exceptional occurrence unlikely to be repeated. Management expresses confidence that LAZR will achieve production readiness by year-end. In the most pessimistic scenario, even if there are further delays with LAZR, the consequences might not be as severe as anticipated, such as Volvo opting not to use LAZR. This is because Volvo has actively promoted its LiDAR sensor and roof design, aiming to make LiDAR a standard feature in all their vehicles. During the conference, management emphasized that the probability of Volvo deviating from this plan is exceedingly low.

Financial review

LAZR currently has a net debt of $211 million ($636 million in debt and $422 million in cash). The debt consists mainly of a convertible debt of $625 million which is expected to mature in CY26, hence there is not so much of a liquidity risk yet, in this front. However, one thing to note is that the business has been burning a lot of cash so far. Using consensus forward EBITDA estimates, LAZR is expected to burn around $500 million. As I see it, there is a good chance that LAZR will need to raise more debt or equity at some point.

Valuation

The way I value LAZR is based on its long-term potential, as I believe the near-term results are not indicative of its intrinsic value. Looking at LAZR SPAC’s presentation, they are targeting a total revenue of $5 billion and more than $2.5 billion in EBITDA. Given the strong secular trend for autonomous vehicles, which means higher demand for lidar, I believe LAZR will be able to achieve its FY30 targets eventually. If we assume the business trades at an average market (S&P) multiple of 11x EBITDA, the business would have an enterprise value of $27.5 billion, which is substantially higher than the $2.3 billion enterprise value today. In fact, the upside might be even larger as the stock could be trading at more than 11x EBITDA, given that it should continue to grow at a healthy rate as the industry is still new (FY30 is only 7 years away), and it has a higher margin profile than the market.

Risk and final thoughts

If the number of cars with L3 technology lags behind projections, LAZR’s sales could be lower than expected. OEMs may also be more hesitant than usual to adopt higher-level software components, such as the perception software offered by LiDAR vendors. Despite LAZR’s technical advantages, this caution could restrict its market potential.

All in all, I recommend a buy rating for LAZR based on its promising trajectory and strategic developments. While the company’s recent quarterly results align with expectations, the focus should be on qualitative milestones and the long-term potential. Collaborations with established partners like Mobileye, Polestar, and Nissan, as well as the pursuit of new partnerships like the one with Plus, underscore LAZR’s commercial progress. Furthermore, LAZR’s involvement in developing a mapping engine and its partnership with Nvidia demonstrate its industry recognition and potential for future growth.

Read the full article here