Investment Rundown

One of the key issues with Rekor Systems Inc (NASDAQ:REKR) right now has to be the massive runup the share price has had in the last few months. Up over 200% in just 12 months is not seen very often and the leading cause has been the AI hype I think. REKR is still a very small company with a market cap of just $250 million but has already managed to grow exponentially. Looking at the last earnings report the company is making very strong improvements in regard to the recurring revenues of the business.

Based on the sales multiply, the company extrudes a significant premium at 132% right now. I don’t think it’s worth getting into REKR right now, or at the very least until we see consecutive quarters with positive EPS being posted. That still seems to be quite some years out. The massive runup also includes the risk of a significant correction in the near term. The downside seems far greater than the upside until we get some clarification about the actual earnings opportunity of REKR. For this reason, I am rating REKR a sell right now.

Company Segments

REKR is a technology firm specializing in the provision of intelligent infrastructure solutions tailored to the needs of transportation management, public safety, and urban mobility markets. Operating in the United States, Canada, and various international locations, the company employs cutting-edge technologies such as artificial intelligence (AI), machine learning, and comprehensive data analytics to bolster the development of intelligent infrastructure systems that facilitate and enhance smart mobility initiatives. With a commitment to innovation and data-driven solutions, REKR plays a crucial role in optimizing various aspects of urban and transportation management.

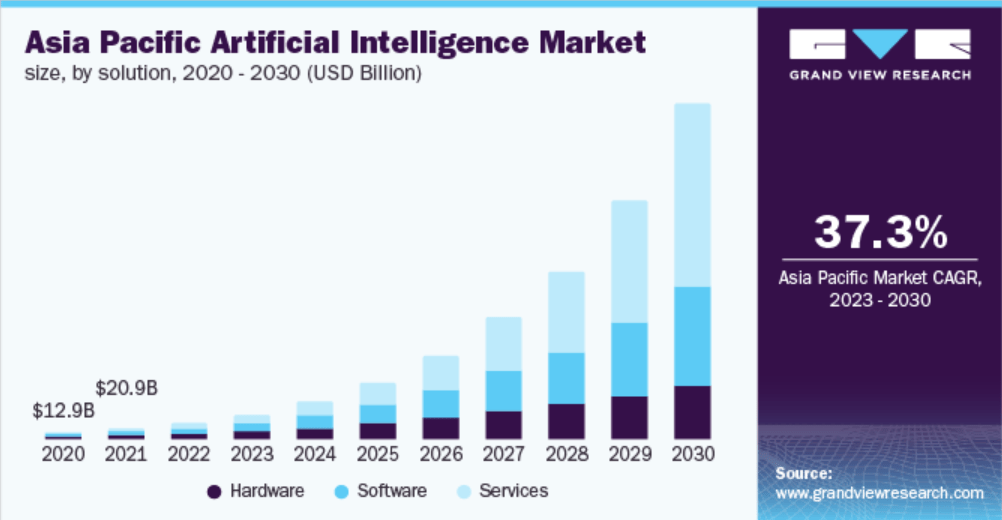

Market Outlook (grandviewresearch)

AI is going to be one of the fastest growing markets in the world for the next decade at least as the application of the tools and services are everywhere. As we know with REKR, the area is primarily around its usefulness in traffic and infrastructure solutions. Looking at the broader market for AI though by 2030 the Asia Pacific region alone is expected to see a CAGR of 37.3% from now until 2030. Just last year the market was valued at $135 billion and seeing similarly high double-digit growth in the US market I think is realistic.

Earnings Highlights

Looking at the results from the last quarter, it seems that REKR has had another solid push of momentum as the recurring revenues grew impressively to $5.8 million, up from $2.1 million a year prior.

Income Statements (Earnings Report)

The strong top-line results however don’t reflect the fact that the bottom line is still very much in the negative as REKR had a net loss of $11 million recently. With the cash position at under $3 million, REKR is unable to meet obligations and the continuation of diluting shares will happen. Since 2020 the company has doubled the outstanding shares, which is quite worrying. But then again, it’s not a very uncommon practice among smaller and quickly growing companies. Given the massive run-up of the share price in the last 12 months, I think from REKR’s point of view it makes a lot of sense to raise capital through dilution right now as the premium is so high and the reward so appealing. This will of course hurt shareholders and I would rather stay on the sidelines for now, resulting in my sell rating.

Risks

Given the limited cash runway the company currently has, relying on this approach to address its liquidity challenges carries a significant level of risk. Should the company fail to execute this strategy successfully, it may face considerable uncertainties in terms of its path forward and financial stability. It’s imperative for the company to effectively implement this plan to navigate its way to a more secure financial future.

Operating Expenses (Seeking Alpha)

REKR is facing record levels of operating expenses as they are trying to expand but also expand the margins at the same time.

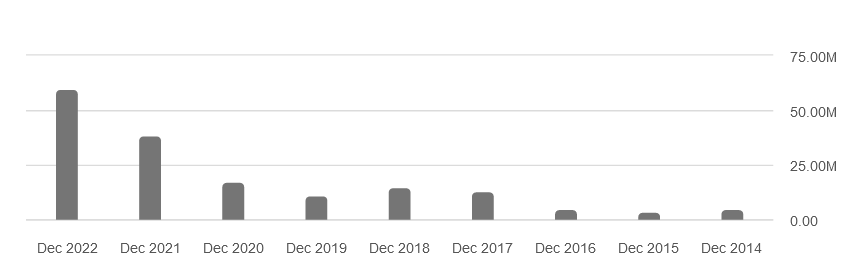

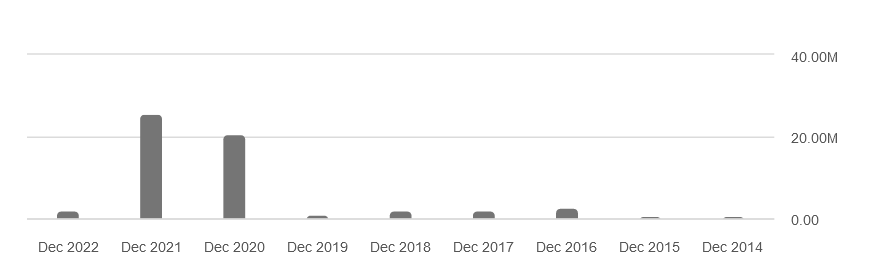

Cash Position (Seeking Alpha)

The cash position has been very volatile in the last few quarters and years and once again sits at some of the lowest levels. The likelihood of a significant share dilution is certainly left on the table still, in my opinion.

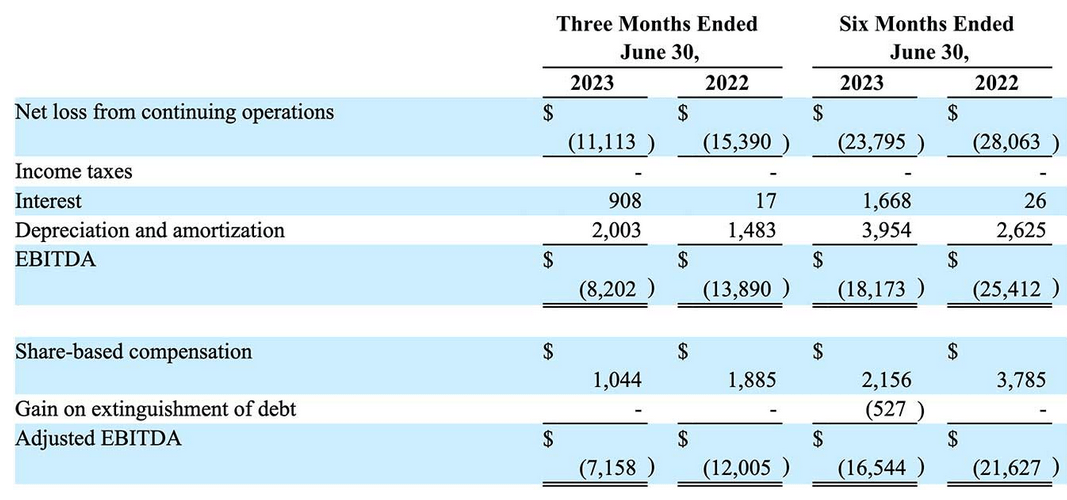

Looking ahead to the long term, assuming the company effectively resolves its short-term liquidity challenges, its strategic vision revolves around the acquisition of a substantial portfolio of government contracts spanning five to ten years. The ultimate goal is to secure a critical mass of these contracts, which would then pave the way for the company to tap into conventional debt financing through commercial banks. However, it’s worth noting that management is keen on expediting this process. This urgency is evident in their projections, with the expectation that EBITDA will reach breakeven by the third quarter of 2023, possibly even achieving some level of profitability. The risk, however, comes forth as a failure in achieving EBITDA breakeven in 2023 will likely send the stock price down significantly as its growth prospects it will have to be redetermined. The last quarter still showed an EBITDA loss of $7.2 million, so a lot of work is necessary to make the goal a reality.

Final Words

REKR is a rapidly growing company, but the last 12 months have opened up the possibility of a significant correction in the share price in my opinion. The company is bleeding cash as it struggles to raise the EBITDA to a breakeven level quickly enough. The top line may be growing quickly, but it needs to trickle down and be visible in the net incomes as well. I think we are many years out until REKR becomes profitable. The implied volatility in the meantime and the likelihood of a large correction leave me rating REKR a sell for now.

Read the full article here