ASML (NASDAQ:ASML, OTCPK:ASMLF) is down around 5% from my last article on the company in May this year. The company currently takes up around 6% of my long-term stock portfolio and in this article, I plan on going into detail about how I’ll deal with the position since a lot of things have changed since my latest article.

The Business

The Dutch company ASML is an expert in creating cutting-edge technological solutions, particularly in the area of lithography, which benefits the semiconductor industry. An important stage in the production of microchips is the transfer of a design onto a silicon wafer using the lithographic technique. The circuitry of electrical devices is built on top of these microchips.

A silicon wafer is covered with photo-resist, a light-sensitive substance, during the lithography process. Then, a photochemical reaction is started by exposing this substance to light with a certain pattern. The parts that are exposed to the light either become more or less soluble, depending on the type of resist utilized. After that, the resist’s modified or unaffected regions are eliminated, leaving the wafer’s surface with a pattern. The actual circuit components are produced by later procedures like etching and depositing using this layout as a guide.

ASML creates lithography technologies that make use of many forms of light, including ultraviolet and extreme ultraviolet (EUV), to keep pushing the limits of miniaturization. These methods allow for the careful control of light and pattern transfer, assisted by cutting-edge optics and computer algorithms, enabling the creation of ever more intricate and accurate microchips. ASML has solidified its position as the leading supplier of cutting-edge lithography solutions, holding a total monopoly in the most cutting-edge technology category, Extreme Ultraviolet (EUV), and having over a 90% revenue market share in the entire lithography equipment industry. Using this latter technique, cutting-edge microchips with feature sizes of 7nm, 5nm, or even 3nm may be created.

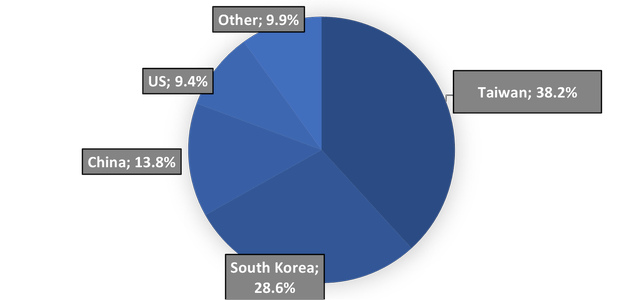

Geographically speaking, ASML’s business in 2022 breaks down as follows:

ASML’s countries of operation 2022 (marketscreener.com)

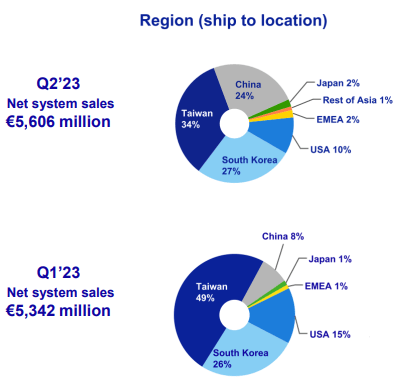

In their latest quarterly results, however, the company declared a higher China focus:

ASML’s countries of operation Q1 & Q2 2023 (asml.com/en/investors)

This seems very worrying at first glance, as the ongoing “Cold War” or Trade War between the US and China could negatively impact ASML’s business. Since ‘the West’ is banning certain companies from selling high quality technology in China. Especially now if the company is currently relying close to a quarter of its revenue on the Chinese market, as of Q2 2023.

According to the CEO Peter Wennink in the latest earnings call, this sudden boom in Chinese sales comes from strong demand for more mature and mid-critical nodes and it actually offset some demand delays in the overall DUV market.

He also laid emphasis on the fact that ASML’s business of EUV tools – the more advanced, macroeconomic important nodes – is already restricted and their business won’t be further impacted by the export control regulations:

As a reminder, sales of ASML’s EUV tools have already been restricted and the business in China is predominately focused on mature or mid-critical nodes. The new Dutch export control regulations will come into effect on September 1, 2023. There were also some reports in the media recently about additional US export controls. Of course, we will and cannot respond to speculation. However, based on our current understanding, we do not expect to change our previously communicated view. Therefore, based on everything we have been made aware of as of today, we do not expect the Dutch and potential additional US measures to have a material impact on our financial outlook for 2023 nor on our longer-term scenarios.

The Fundamentals

Global developments in the electronics sector, supported by a successful and creative environment, are expected to support semiconductor market growth. Demand for ASML’s goods and services is rising as a result of these developments and an increase in the complexity of lithography. Offering affordable solutions for both cutting-edge and established technologies, the company’s broad product portfolio is deliberately matched with client demands. According to financial predictions, ASML may generate annual revenues of between €30 and €40 billion by 2025 and between €44 and €60 billion by 2030, with rising gross margins.

In order to fulfill current and future demand, ASML is actively ramping up and improving manufacturing capacity with its supply chain partners. According to the company’s 2022 Annual Report, it is also moving quickly to implement its ESG Sustainability plan. In addition, ASML intends to keep giving back a sizable sum of money to shareholders via a combination of rising dividends and share repurchases.

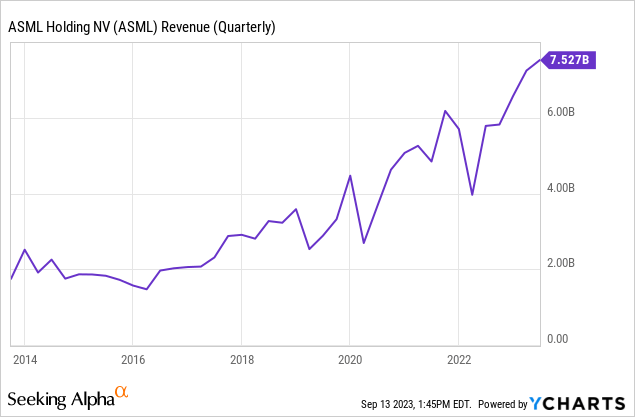

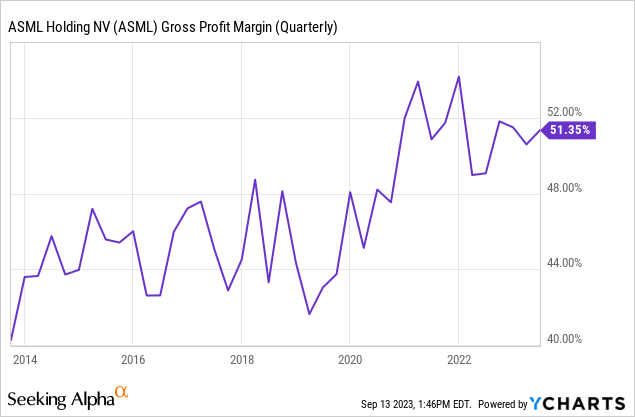

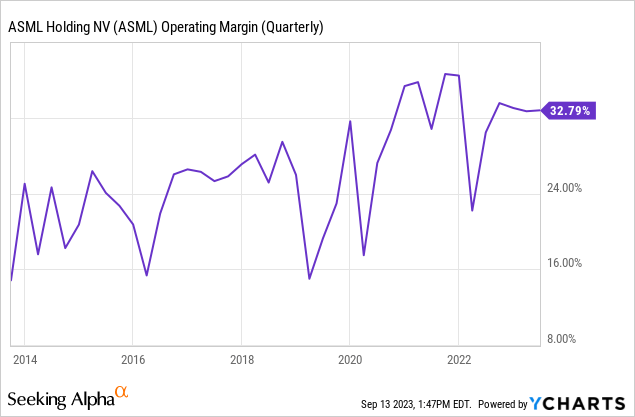

ASML achieved a very solid quarterly revenue of $7.5 billion last quarter, that’s YoY growth rate of ~30%. The company managed to achieve this while also consistently increasing its Gross and Operating Margin.

Outlook

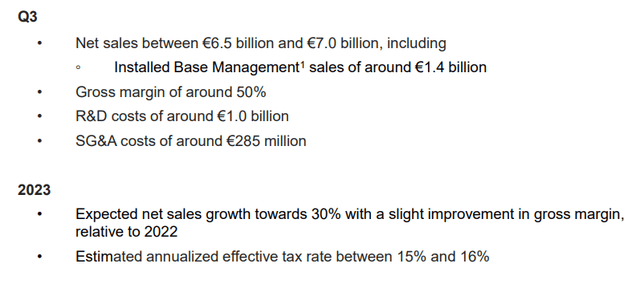

ASML’s management has updated its outlook for Q3 2023 and FY2023. They now expect a YoY revenue growth of 30% and a slight improvement in gross margin compared to 2022.

ASML Outlook Q2 2023 (asml.com/en/investor)

For 2025 and 2030 we can refer to ASML’s investor days from 2022. Here they gave the revenue guidance of €30 and €40 billion in 2025 and between €44 and €60 billion in 2030.

ASML Investor Days 2022 (asml.com/en/investor)

Generally, the CEO of ASML also seems very optimistic for the future and states that the longer-term megatrends discussed at Investor Day 2022 are expanding the application area and driving demand for advanced and mature nodes despite the short-term uncertainties. Demand for their goods and services is being driven by secular growth drivers in semiconductor end markets including electrification and AI as well as rising lithography intensity on upcoming technology nodes.

Subsidies As A Major Tailwind

As already stated in my last article on ASML the current subsidies in the semiconductor market could heavily benefit ASML.

Through the high concentration of the chip market in East Asia – around 75% of the world’s chips are manufactured there – other countries try to narrow the gap here through massive subsidies. As a result, the semiconductor sector has received around $52 billion from the US and €43 billion from Europe in subsidies. By aiding companies with the purchase of new manufacturing equipment or the development of existing capacity, these investments highlight the strategic importance of the sector and the need to boost local production capacities.

As businesses like Intel (INTC) for example transition to a business model that is more and more focused on manufacturing, similar to TSMC, they will require more advanced technology. As a result of greater governmental support for and financing for the semiconductor sector, companies like ASML, which offers crucial production equipment and technologies, will definitely see a rise in demand. Political leaders’ growing acknowledgment of and support for the sector may result in growth opportunities that encourage capital investment and technical innovation.

Recession As A Major Risk

Experts are still expecting a global recession for late 2023 or early 2024. This might provide ASML with immediate difficulties. Although it’s important to remember that the semiconductor sector has a history of being highly cyclical, I’m however still confident in the continuation of its overall growth trajectory. The global economy’s growing reliance on semiconductor technology makes it probable that the industry will continue to grow gradually, even if there are a few minor hiccups along the way.

Valuation

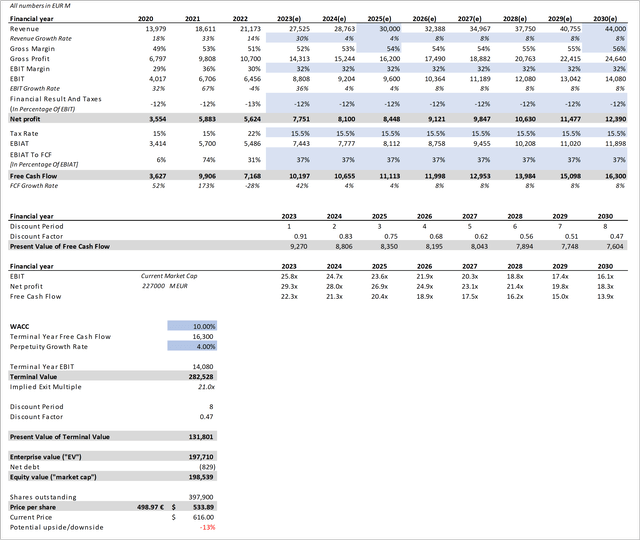

As always, we now take a look at ASML’s valuation. I believe a Discounted Cash Flow Analysis is very fitting, to evaluate this high quality, monopolistic semiconductor stock. A peer group analysis poses the problem that suitable competitors for ASML are just very hard to find and if you find some similar companies, they can’t be compared 100%. I created a Discounted Cash Flow Analysis for management’s bear and bull cases. Even though I believe their own goals seem to be very pessimistic.

Bear Case

- Revenue and Gross Margin: Like mentioned, the revenue and gross margins assumptions for the bear case, are the low end of management’s expectations for 2025 and 2030. The revenue between these years were projected using a linear growth rate p.a.

- EBIT Margin: I averaged out the last three years and assumed that the margins would stay flat at the three-year average of 32%. In the last quarter, they managed to achieve 32.8%. So, this seems reasonable.

- Financial Result And Taxes: Here I again averaged out the last three years and therefore used -12% on the EBIT to calculate the net profit.

- Tax Rate: Here I used 15.5% as this is right in the range of ASML’s guidance for 2023 and is in the range of 2020 and 2021.

- Free Cash Flow: From here on I used the tax rate to calculate the EBIAT and then tried to determine a usable EBIAT to Free Cash Flow ratio. By averaging out the last three years, we get a ratio of 37%. This looks reasonable as in 2020 we have a clear outlier with 6% and in 2021 with 74%

- WACC: For the WACC I used 10%, which is right around ASML’s current WACC.

- Perpetuity Growth Rate: For the perpetuity growth rate I assumed 4%, while this is higher than in most of my DCFs, I believe that a semiconductor stock and ASML deserve a higher growth rate here.

Discounted Cash Flow Analysis ASML Bear Case (seekingalpha.com, ASML.com, own assumptions)

With this bear case, we get a price target of ~ €500 or ~$534, suggesting that the company could be overvalued by around 13% with these assumptions.

Bull Case

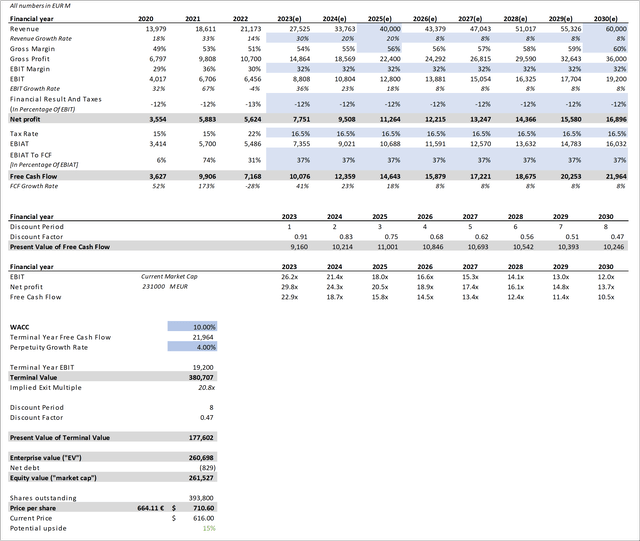

For the bull case, we assumed the high end of management’s revenue and gross margin guidance for 2025 and 2030. So €40 billion and 56% in 2025 and €60 billion and 60% in 2030. Other metrics stayed the same.

Cash Flow Analysis ASML Bull Case (seekingalpha.com, ASML.com, own assumptions)

Within our bull case scenario, we arrive at a price target of ~ €664 or ~$710, meaning that ASML is undervalued by 15% in the bull case.

Conclusion

With our Discounted Cash Flow Analyses we get a price range of $534 to $710. This results in a potential valuation gap of -13% to 15%. With almost the same gap in both directions for the bear and bull case, one could argue that the ‘Base’ Case is exactly between the two and the company could therefore be fairly valued right now.

Given the very high quality, the monopolistic market standing in a very geopolitical important industry, and the fact that management’s bull case for 2030 seems to be on the more conservative side – considering that they ‘only’ assume an annual revenue growth rate of 14% compared to ASML’s ten years average of almost 20% – the company is at a solid entry point in my opinion. That’s why I currently rate the company as a ‘Buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here