The Chemours Company (NYSE:CC) has remained rather stagnant over the past decade with several price fluctuations due to volume volatility. I believe that Chemours is currently a buy due to the firm’s solid ability to create shareholder value, optimize its portfolio to stimulate growth, and the firm’s undervaluation assuming my DCF values.

Business Overview

The Chemours Company provides performance chemicals to North America, Asia Pacific, Europe, the Middle East, Africa, and Latin America. Their organizational structure is divided into three primary segments: Advanced Performance Materials, Thermal & Specialized Solutions, and Titanium Technologies. The business sells the TiO2 pigment Ti-Pure, known for offering crucial characteristics like whiteness, brightness, durability, and protection, through the Titanium Technologies section. This pigment is widely used in many different contexts, including industrial and architectural coatings, plastic packaging, laminate sheets, and coated paperboard. Refrigerants, thermal management solutions, foam blowing agents, propellants, and specialty solvents are just a few of the products offered in the Thermal & Specialized Solutions area.

The product portfolio of the Advanced Performance Materials division is broad and includes industrial resins, customized goods, coatings, and membranes that serve a variety of industries, including consumer electronics, energy, transportation, and healthcare. Products are distributed using a combination of direct and indirect channels, including distributors, resellers, and direct sales.

Chemours Company

Financials

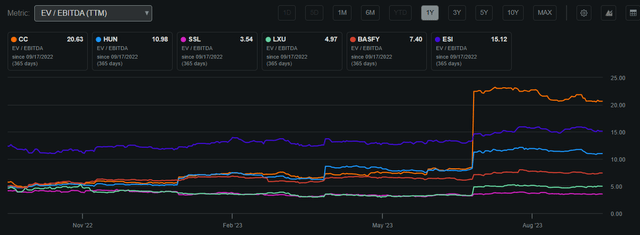

The current market capitalization of Chemours is assessed at ~$4.72 billion. As of now, the stock is being traded at $31.85, just below its 200-day moving average of $32.54. Notably, with an EV/EBITDA ratio of 20.63, Chemours is trading at a premium in comparison to its industry peers. This indicates a potential overvaluation, a point elaborated on in the valuation section of this analysis.

Chemours EV/EBITDA Compared to Peers (Seeking Alpha)

The Chemours Company allocates a 3.14% dividend to its shareholders, reflecting a prudent 30.12% payout ratio. This showcases Chemours’ capability to deliver value to shareholders through multiple channels while ensuring sufficient Free Cash Flow to bolster capital and expand its core operations. Demonstrating a commendable 5-year dividend growth rate of approximately 10%, Chemours underscores its dedication to offering a consistent income stream to its shareholders.

Furthermore, Chemours actively enhances shareholder value by repurchasing company shares, as evidenced by the annual shares outstanding data. This strategic move allows the company to seize opportunities with undervalued shares in recent years, thereby effectively augmenting its Earnings Per Share. Given the firm’s ROIC at 4%, these avenues for growth prove advantageous for Chemours, considering that reinvesting all FCF might not yield adequate returns for shareholders.

Chemours Annual Shares Outstanding (TradingView) Share Performance (Seeking Alpha)

Earnings

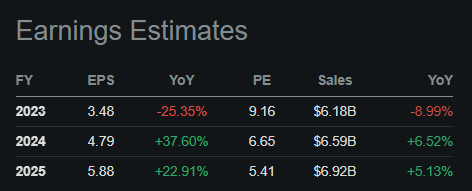

In Q2 2023, The Chemours Company reported a blend of financial outcomes. It exceeded earnings per share expectations by $0.03, reaching $1.10. However, it fell short of revenue expectations by $42.6 million, totaling $1.64 billion, marking a 14.2% year-on-year decline. This hints at a slight vulnerability to prevailing macroeconomic challenges. Forecasts, however, anticipate a rapid rebound attributed to a decline in inflationary pressures and recovering inventories across various firms. In my assessment, closely monitoring the persistent inflationary trends in the short term is advisable to validate the anticipated recovery.

Earnings Estimates (Seeking Alpha)

Performance Compared to the Broader Market

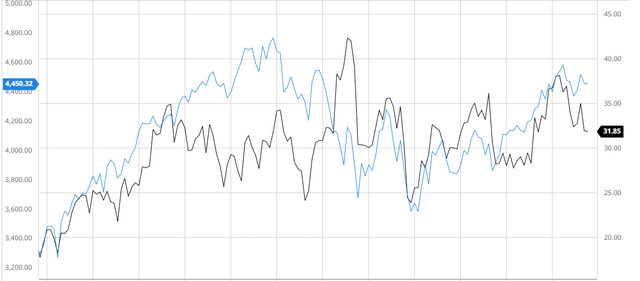

Over the past 3 years, Chemours has underperformed the S&P 500 when adjusting for dividends. Although the firm has underperformed as of today’s prices, Chemours has demonstrated its solid ability to allocate FCF to stimulate growth and create shareholder value due to tracking the S&P almost exactly. As a chemicals company, this is still rather impressive and demonstrates the long-term compounding potential this company holds.

Chemours Compared to the S&P 500 3Y (Created by author using Bar Charts)

Analyst Consensus

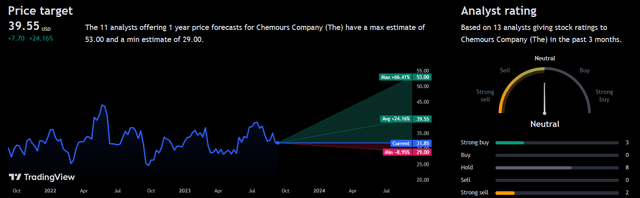

Analysts currently rate Chemours as a “hold” with multiple ratings across the board. This demonstrates the level of divide on whether the firm would recover from this cyclical downturn based on macro factors. But prospects currently look promising with an average price of $39.55 presenting a potential 24.16% upside.

Analyst Consensus (TradingView)

Balance Sheet

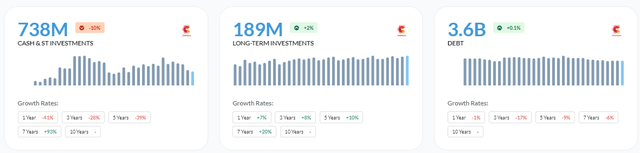

Examining Chemours’ balance sheet, it appears the firm carries a slightly higher leverage than my preference, but I anticipate no substantial long-term risk. The gradual reduction of debt and a decline in interest expenses, coupled with the projected increase in earnings, reassure me regarding the interest coverage of 0.48. This lower coverage is primarily a result of a temporary decline in operating income, which is expected to bounce back. Additionally, the company maintains satisfactory liquidity, evident from its current ratio of 1.54 and Altman-Z-Score of 1.74. While the interest coverage does present a concern, I am confident that it has been adequately addressed and factored into the valuation analysis discussed in the subsequent section of this article.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

Valuation

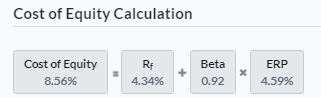

In order to determine a precise fair value for Chemours, it is imperative to compute an appropriate discount rate, considering both the Cost of Equity and the Weighted Average Cost of Capital. Initially, I established Chemours’ Cost of Equity at 8.56% by referencing a risk-free rate of 4.34%, aligning with the present 10-year treasury yield.

Cost of Equity Calculation (Created by author using Alpha Spread)

Assuming the above calculations, I was able to calculate a WACC of 6.66% which is below the industry average of 9.89%.

WACC Calculation (Created by author using Alpha Spread)

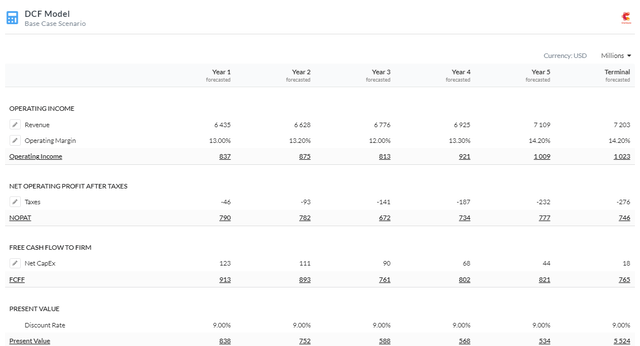

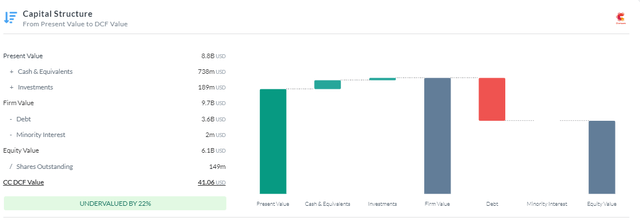

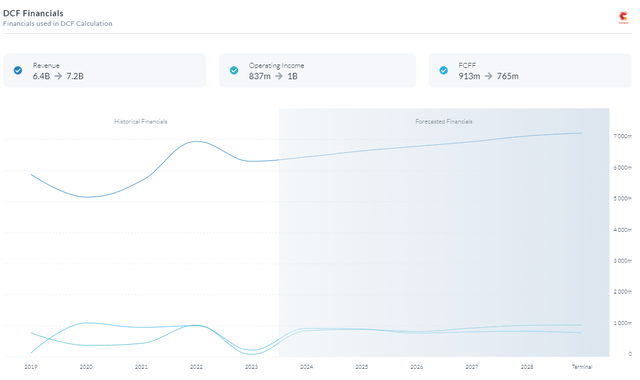

Now that I have calculated the appropriate discount rate for holding Chemours’ equity, I added a 2.34% risk premium resulting in a 9% discount rate to account for its current balance sheet situation, macro headwinds, and cyclical declines all resulting in strained FCF which could reduce future compounding opportunity. I decided to use a 5Y Firm Model DCF using FCFF while assuming analyst estimates in regard to my revenue and margin projections which resulted in a fair value of ~$41.06 which indicates Chemours is undervalued by ~22%.

5Y Firm Model DCF Using FCFF (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Portfolio Optimization Resulting in Compounding Growth

The Chemours Company considers portfolio optimization to be a key component of its overall business strategy. The company’s choice to sell off its non-core operations and assets is a remarkable illustration of this tactic in action. Chemours saw that it could unlock value and improve its overall financial performance by simplifying its portfolio and selling off companies that didn’t complement its core competencies and strategic direction.

One such divestiture was the sale of its Mining Solutions business in 2022. Even though this business was profitable, Chemours decided to sell it in order to concentrate more on its portfolio’s higher-growth areas, such as Titanium Technologies and Fluoroproducts. Chemours sought to focus more attention and resources on markets with significant growth prospects and profits by selling non-core assets.

By using this portfolio optimization method, Chemours is able to lessen its exposure to certain market risks while also allocating resources more effectively. Chemours increases its overall resilience and capacity to provide long-term value to shareholders by focusing on businesses where it has a competitive edge and where it can foster innovation and growth. The company’s dedication to generating sustainable and profitable growth is in line with this strategic approach to portfolio optimization, which also makes sure that the portfolio is flexible and adaptive to shifting market conditions.

I believe that although this reduces the diversification of the firm’s product portfolio, focusing on high-growth segments will bolster long-term cashflows and enable the firm to focus on fewer segments resulting in potential outperformance if cash flow is allocated effectively.

Risks

Environmental Liability and Remediation Costs: Due to current or previous operations, Chemours may be held responsible for environmental damage. Environmental cleanup, trash disposal, or legal activities might result in significant remediation expenses that have an adverse financial impact on the business.

Raw Material Supply and Price Fluctuations: The cost and profit margins of Chemours’ manufacturing can be considerably impacted by the availability and cost of raw materials including titanium dioxide, fluorspar, and refrigerants. Price changes or supply chain interruptions may have an effect on profitability.

Conclusion

To summarize, I believe that Chemours is currently a buy due to the firm’s solid ability to create shareholder value, optimize its portfolio to stimulate growth, and the firm’s undervaluation assuming my DCF values.

Read the full article here