Introduction.

This article compares and analyses three key financial markets — commercial paper, short-term Treasuries, and equities. These dominant markets no longer function efficiently. Especially the commercial paper (CP) market. During the last two major financial crises – the ’08 financial crisis and the COVID-19 crisis – the commercial paper market collapsed completely.

Interestingly, the evolution of these three markets over the last decade or so has resulted in very similar insider-dominant market structures. Despite the seeming likelihood that the advent of electronic trading would produce a level playing field for both investors and dealers, the actual result has been quite the opposite.

It is ironic that while the advent of electronic trading has reduced the cost of trading for all of us, insiders have captured more of the resource cost savings than outsiders have. Moreover, it is disappointing that electronic trading has not reduced the risk of market collapse.

The article considers a fix for the common failures of the three markets. It also suggests a path for existing or new firms to reap the benefits of building a combination of the three markets that is more efficient.

The article begins with a brief description of each market and an examination of its failings. It then summarizes the important common features of the three markets. Finally, it proposes a common fix.

I lean heavily on three sources — an article written by BlackRock executives here, an article written by the staff of the New York Fed here, and an article by the SEC staff here. The BlackRock article provides a description and analysis of the CP market. The New York Fed and SEC articles provide a description and analysis of the Treasury bill market. The failings of the three markets are quite similar, although they differ in the extent of market instability. The specific detailed recommendations are my own.

The Commercial Paper Market.

Structure of the CP market.

CP is considered a cash equivalent for accounting purposes. As a result, CP is held in a wide variety of portfolios, including in-house managed cash portfolios, outsourced cash portfolios, custodial sweep accounts, and Money Market Mutual Funds (MMFs). The distribution of CP holders has changed significantly over the past decade. In December 2007, just prior to the Global Financial Crisis (GFC), MMFs comprised 39% of the investor base, whereas as of December 2019, less than 23% of CP was held by MMFs. Today, the largest investor category is nonfinancial corporate business, which reflects the buildup of cash on corporate balance sheets.

Banks act as intermediaries in the CP market, purchasing paper and then re-selling to investors. Many smaller issuers rely on banks to serve as dealers. Banks also serve as key liquidity providers in the CP market. Banks that deal in CP expect originators to issue their CP only to a single bank. Dealer banks are thus a single source of liquidity for each issue.

Since CP maturities are short, ranging from days to months up to 270 days, most investors purchase at issuance and hold until maturity. As a result, the CP secondary market is relatively small. Many investors roll over maturing CP by purchasing new issues as their holdings mature. If investors sell CP before maturity, they typically sell it back to the same CP dealer that originally offered the paper. In fact, many banks are unwilling to bid on paper from issuers where they are not a named dealer on that program. This single source of liquidity model failed during the COVID-19 Crisis, particularly, when banks needed to protect their balance sheets and hold liquidity to comply with capital and liquidity regulations. In this environment, investors were unable to sell the CP they were holding. This contrasts with the more diversified sources of liquidity found for financial instruments that are either exchange-traded (e.g., equities, ETFs) or encourage the participation of multiple market makers (e.g., cleared derivatives).

The de facto monopoly that a CP issuing dealer has in providing liquidity presents the very real possibility that the dealer can step away from the paper, in stark contrast to other financial instruments from equities to bitcoin.

The Commercial Paper Market’s Recent Failures.

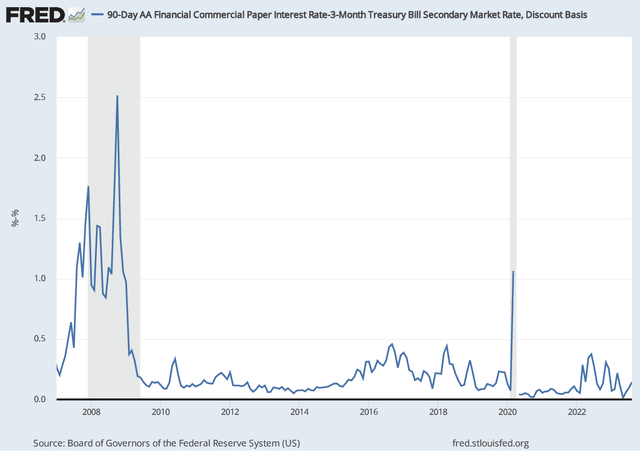

A major contribution of a stable liquid bellwether CP market is investor access to a daily measure of the added cost assessed by investors to bear short-term credit risk. The graphic below describes the recent history of the CP 3-month Treasury bill spread. Note the series break during the COVID Crisis in 2020.

Risky vs Riskless Debt (Author (FRED)) |

The commercial paper market has proven problematic during the return to nonzero interest rates. It has collapsed with recent significant financial crises – the GFC and the COVID-19 crisis.

In contrast to commercial-paper-based asset yields, the once-dominant London Interbank Offered Rate (LIBOR) provided a more stable measure of the cost of credit-risky short-term debt. The market for London bank-to-bank deposits remained stable and available during financial crises. However, financial regulators concerned with the possibility that the illiquid LIBOR spot market was manipulated have phased out LIBOR. With the demise of LIBOR, the markets for short-term risky debt no longer feature a reliable bellwether.

I have argued elsewhere that there is a way to rectify the shortcomings of the two short-term debt markets. My fix is consistent with recommendations by the three cited author groups. Every market would benefit from an exchange-based all-to-all traded instrument. An all-to-all exchange would be more efficient than the current “single source of liquidity” market structure. An all-to-all market allows any market participant to trade directly with any other market participant.

I have edited this quote from the BlackRock article.

“Short-term funding markets are critical for financing governments, banks, and non-financial companies. Likewise, these markets provide important investment opportunities for investors seeking some improved return on near-risk-free assets, mainly Treasuries. However, in mid-March 2020, short-term funding markets essentially closed. For close to two weeks, there was no bid in the secondary market in the US for much of the commercial paper (CP) assets. Even Treasury bills came under pressure and primary issuance for corporate issuers abruptly halted. In normal markets, banks play a critical role as intermediaries and liquidity providers for both the primary and the secondary markets. However, as the potential impact of the COVID-19 Crisis became clearer, banks understandably withdrew from the short-term markets to protect their own capital and liquidity and to maintain compliance with their regulatory requirements. In assessing short-term markets in March of 2020, the structural aspects of the overall market need to be considered in addition to the performance of its individual components. For instance, one might ask, ‘Why could you buy/sell bitcoin when you faced no bid on commercial paper.’ The answer is that bitcoin is traded on an exchange rather than through a highly regulated intermediary using its own leveraged balance sheet. Similarly, fixed-income exchange-traded funds (ETFs) were trading in March, even when the underlying bonds in which they invested were not. The derivatives market also performed well, given the post-GFC reform that required the over-the-counter (OTC) derivatives market to move from primarily bilateral contracts to central clearinghouses or Clearing Counterparties (CCPs). This requirement provided more transparency, standardization, and liquidity and contributed to the strong performance of the derivatives market during the COVID-19 Crisis. Many different investors facing different constraints and seeking different objectives hold CP. Addressing problems in the CP markets requires more than reforms to Money Market Funds (MMFs), which represent less than 25% of the CP investor base. While there is a small secondary market, typically CP will only be bid on by the bank that originally offered the paper. The COVID-19 Crisis underscores the need to consider improving the liquidity of CP by making changes in the market structure for CP and other short-term instruments.”

The Treasury Bill Market.

The Structure of the Treasury Bill Market.

A second important short-term credit-riskless instrument that pays insider yields to dealers and outside yields to investors is Treasury bills. It is generally agreed among practitioners that the U.S. Treasury market is the deepest and most liquid securities market in the world. It plays a critical role in the U.S. and global financial systems.

US Treasury securities trade in a multiple dealer, over-the-counter secondary market. The predominant market makers are the primary government securities dealers, those having a trading relationship with the Federal Reserve Bank of New York. Dealers trade with the Fed, their customers, and one another. Nearly all interdealer trading occurs through interdealer brokers (IDBs), which match buyers and sellers, while ensuring anonymity, even after a trade.

On the other hand, dealers in over-the-counter transactions handle nearly all investor purchases and sales of Treasury securities. This expensive use of the capital of each dealer with no pooling of identical risk limits the marginal ability of dealers to allocate space on their balance sheets. A loss of market functionality is thus possible. This occurred in March 2020, spurring the Federal Reserve to initiate asset purchases to support market functioning. It also led to extensive study and ongoing discussions of how Treasury market resilience might be improved and to various policy initiatives to promote a more resilient market.

The secondary market for Treasury securities has experienced several episodes of abrupt and severe deterioration in the functioning of some market segments, although the market has evolved significantly in recent decades, including changes in technology.

The cash secondary market for U.S. Treasury securities has two main components, the interdealer cash market and the customer-to-dealer market. Like commercial paper, it is an insider-outsider market.

- The interdealer (inside) spot market. In the interdealer cash market, trading is generally among the dealers and principal trading firms (PTFs). PTFs trade as principals for their own accounts and generally use automated trading strategies. Most interdealer cash trading takes place on electronic platforms provided by interdealer brokers (IDBs) which operate central limit order books.

Electronic interdealer cash trading is concentrated in the most recently issued, or on-the-run, Treasury notes and bonds, consistent with the highly automated trading system (ATS) and interdealer volumes for such securities. Most interdealer trading of seasoned, or off-the-run, notes and bonds occurs on voice and manual-assisted platforms for which trading is less automated and at slower speeds.

- The dealer-to-customer (outside) market. In the dealer-to-customer market, dealers buy securities from and sell securities to a variety of clients, including, but not limited to, foreign central banks, asset managers, pension funds, and hedge funds. A range of trading methods is used, including electronic request-for-quote trading and voice trading.

The interdealer market focuses on a few bellwether issues to promote liquidity. In addition, the interdealer market uses the more efficient CCPs. Typically, but not always, the CCP includes a clearinghouse that acts as a counterparty to each side of its members’ transactions and guarantees their performance.

Before the introduction of electronic trading, dealers had been the predominant participants in the interdealer market. PTFs first gained access to electronic trading platforms in the cash market in the mid-2000s, and by 2014, these platforms represented most trading activity in the futures and electronically brokered interdealer cash markets.

Dealers temporarily warehouse customer sales and purchases on their balance sheets until laying off excess inventories with other customers or dealers. This results in a dependence of market liquidity on intermediary funding liquidity. Because of debt overhang, equity and debt financing of market-making inventories impose costs on dealer shareholders that reduce the aggressiveness of dealer liquidity provision. There is an obvious connection between asset pricing and the balance sheet costs of dealers.

Market participants understand that a predominant driver of Treasury market illiquidity is interest rate volatility. Volatility increases the riskiness of intermediating markets, leading to wider bid-ask spreads and reduced depth.

The Treasury Bill Market’s Recent Failures.

While the disruptions to the Treasury market at the onset of the COVID-19 pandemic in March 2020 were unique and unprecedented in nature, they have some similarities with other recent market disruptions, including the October 2014 flash rally and the September 2019 repo market pressures.

A recurring theme is that trading volumes and demand for intermediation can surge suddenly, but intermediaries’ willingness or capacity to respond can be relatively inelastic compared with these surges, potentially leading to rapid deterioration in market functioning.

Prices in the cash, repo, and futures markets are linked because it is possible to purchase a Treasury security in the cash market, finance the purchase in the repo market, sell the corresponding futures contract short, and then deliver the security in satisfaction of the futures contract when the futures contract expires.

Positive changes in the Treasury bill market.

A key advantage to a market structured around all-to-all platforms is the reduced inventory of Treasuries needed by PTFs to support market liquidity. From the point of view of PTFs, the when-issued Treasuries market is often more attractive than the markets for seasoned issues, since when-issued Treasuries require no inventories.

Much like the equities markets before them, the debt markets have taken advantage of electronic trading platforms to trade using electronic algorithms.

Parallels between the changes in the structure of the equities markets and the structure of the Treasuries market are apparent. (See my discussion of the structure of the equities markets here and elsewhere). PTFs in Treasuries trading, much like Wholesalers (Citadel, Virtu) in equities trading, have become intermediaries between investors and CCPs. Ironically, both markets have regressed from the once more efficient exchange trading structure to the now more costly OTC trading method.

The Common Properties of the Three Market Structures.

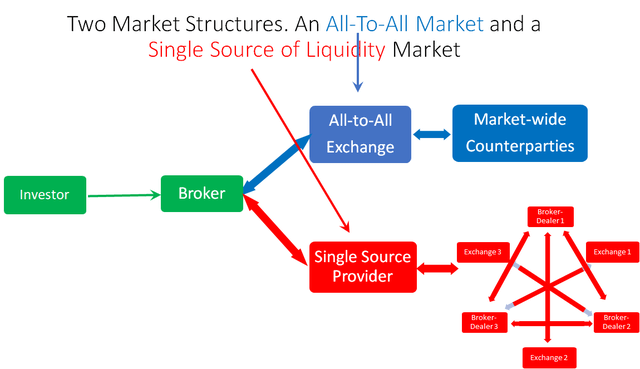

The graphic below displays the common market structure of the three markets.

Two Market Structures (Author)

.

Neither debt market has an all-to-all provider. None of the three markets has a single source provider.

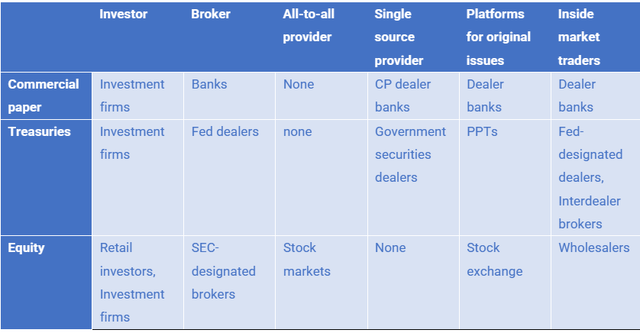

The table below shows the specific names of each market function provider in each of the three markets.

Market participants in the three markets (Author)

An explanation of the table follows.

- Investors. An investor is either an institution or an individual. The role of the broker is to access securities on the investor’s behalf. In the olden days, before electronic trading became the norm, it was reasonable to suppose that the broker represented the interests of the investor.

- Brokers. Electronic trading, although far less expensive and more efficient in filling orders than the old phone-based broker-to-trader relationship, had several negative effects on the incentives of brokers. Most importantly, brokers realigned their loyalties, becoming agents for insiders and giving lip service to outsiders.

- All-to-all providers. All-to-all providers exist only in the stock market. Even there, they serve insiders such as high-frequency traders and wholesalers, not investors.

- Single source provider. Only the futures markets are single source providers among exchanges. The futures exchange practices of listing the instruments they trade and require that the exchange clearinghouse be the counterparty to every open position guarantee it.

Recommendations.

A customer-facing market.

What should change to make trading in the three markets more efficient and more accessible to retail investors? Lower resource costs and best execution for both outsiders and insiders are the key considerations. Here are some proposals that in many ways parallel my earlier proposals for improving the equities markets.

In the market for Treasuries:

- The deliverable instrument should not depend on the Treasury’s auction schedule. Why separate the Treasury market’s bellwether index from the Treasury’s auctions? These reasons:

- First, to assure market stability and reliability, there should be a direct link between the spot and futures markets that simultaneously price the Treasury-based instrument. That is, if the buyer fully performs her duties, the exchange should issue the deliverable instrument directly. If the buyer has bought a futures contract promising delivery of a financial instrument at a specified future day and time, the resulting performance risk should be exposure to the exchange’s performance only.

- Any futures contracts listed before the Treasury issues a security would limit the Treasury’s ability to manage its auction.

Most financial futures contract markets create the connection between futures prices and spot prices in one of two ways.

- The futures markets force cash market linkage with futures by settling the futures price at a cash market price measured at a specific time and day. Since the introduction of S&P futures and Eurodollar futures, this method, called “cash settlement”, has dominated newly introduced futures contracts settlement methodologies. The problem with this method is that there is no direct interaction between the spot and futures markets. I cannot buy an S&P futures contract, for example, and walk away with a spot S&P-based EFT.

- The futures settle when the seller delivers the spot security to the buyer, as for example, with the Treasury bond futures contracts. This is a three-day process, and the seller transfers the deliverable Treasury directly to the buyer. Once the seller notifies the exchange of its intention to deliver, the exchange clearinghouse is no longer the intermediary – that is the clearinghouse is no longer seller to buyer and buyer to seller. Thus, there is no sense in which the exchange delivers the instrument received by the buyer independently of the seller’s performance.

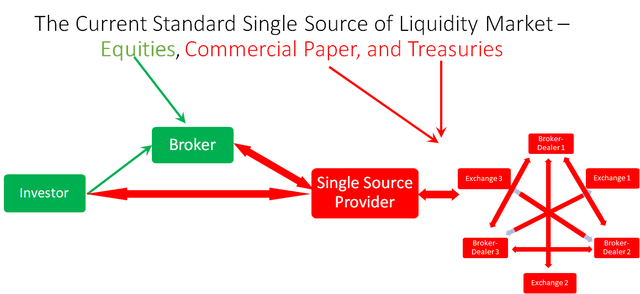

The graphic below expands the single source market structure to compare the equities market structure to the market structure of the two debt markets.

A Single Source of Liquidity Market (Author)

The graphic illustrates the primary distinction between equities and the two debt markets; to wit the equities markets, insert a broker between the single source provider and the investor. This turns the broker into a customer of the single source provider as broker payments are no longer fees paid by investors but instead payments for order flow paid by wholesalers.

The recommendations for common market structure change.

- All-to-all market. Single source provider.

There are four key benefits to an all-to-all, single source provider market that lists, clears, and serves as a counterparty to every market participant.

· Every trader would see the same prices. No inside market.

· Counterparties would be anonymous to all but the clearinghouse.

· The single source provider, the exchange clearinghouse, always has equal seller and buyer open interest, bringing exchange market risk to a minimum.

· Responsibility for management of instances of market instability is clearly assigned to the exchange.

-

Futures-market-like clearing.

The exchange transfers ownership only on a trader’s market exit and entrance. Futures trading reduces the cost of clearing by retaining control of both long and short positions.

-

Exchange-originated securities.

The exchange would list asset-backed securities. The objective of the exchange would be to transform ordinary securities designed to meet the needs of issuers into exchange-listed securities that meet the needs of investors. This would reverse the current market intermediators’ shift in focus to issuers instead of investors.

-

No fourth-party clearing (no DTCC).

Eliminate fourth-party clearing. The exchange provides clearing services. This might reduce the cost of clearing to a point where the exchange-originated securities have greater market value than that of similar securities traded in other marketplaces.

Conclusion.

The three markets I examine have benefitted greatly from electronic trading. However, electronic trading has also had several negative effects. Chief among these: market outsiders, mainly investment firms and retail investors, receive lower quality prices than insiders. An all-to-all, single source provider can eliminate the possibility of an insider market if investors choose to use it. To assure investor access, the new market provider will need to attract retail and institutional broker participation. Failing this, the exchange could open a brokerage subsidiary.

This new exchange could guarantee a lower cost structure by eliminating market dealer intermediaries and the outdated DTCC clearing system. Combined with a simpler market structure and lower clearing costs, it seems inevitable that it would outperform the other market structures.

The primary barrier to an exchange with the recommended properties succeeding is the likely blacklisting of the exchange by market insiders. This was a major concern for financial futures markets when they were beginning in the ’70s and ’80s. However, the success of financial futures changed the attitude of insiders. Should the new exchange successfully attract customer business, there is no reason the new venture should not do the same.

Read the full article here