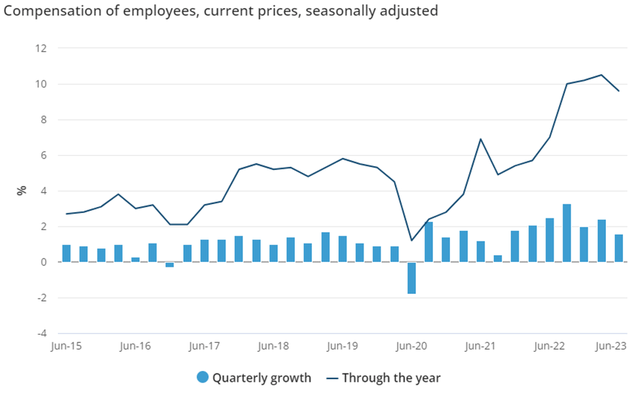

Australia’s recently released Q2 GDP report may have confirmed the economy’s resilience through the tightening cycle so far, but there were plenty of negatives as well. Most notably, nominal labor costs (against productivity declines) aren’t likely to ease anytime soon amid further upward pressure from the big July minimum wage hike and rising rents, particularly in Sydney and Melbourne. Thus, there’s a clear risk of an extended rate hike cycle by the Reserve Bank of Australia (i.e., the Australian central bank) in reaction to ‘sticky’ core inflation. Not only will further tightening hit equity valuations, but it also compounds ongoing consumer difficulties, which, per the ‘family finances’ component of this month’s consumer sentiment index, is worsening to levels not seen since prior recessions.

Australian Bureau of Statistics

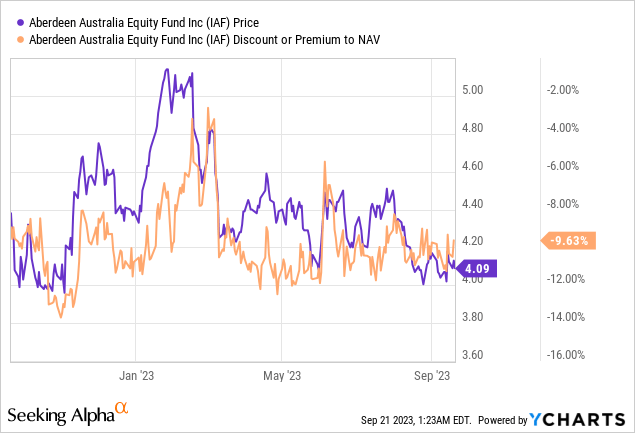

Unlike in other developed markets, rates are really starting to bite now that Australia has reached its ‘mortgage cliff.’ Recent trading updates confirm as much, with net earnings revisions turning strongly negative, as corporate margins face pressure from all sides (higher labor costs and weaker revenue), particularly for more rate-sensitive sectors. Combined with underwhelming Chinese stimulus measures thus far, offering little offset to demand weakness for energy or bulk commodities from its ongoing property troubles, the abrdn Australia Equity Fund (NYSE:IAF) looks set to take more hits going forward. The pricey stock valuations don’t help either – Australian large caps command a ~16x fwd earnings multiple vs. consensus estimates for a high-single-digit % earnings decline this year. Even at a slightly wider than average ~10% NAV discount, I won’t be adding the abrdn Australia Equity Fund to my portfolio anytime soon.

Fund Overview – A Pricey Australian Blue-Chip Investment Vehicle

The abrdn-managed Australia Equity Fund is an active closed-end fund that targets absolute return outperformance relative to its benchmark, the market-cap weighted ASX 200 Index. In addition to the classic abrdn focus on fundamental bottom-up stock selection for capital appreciation, the fund also prioritizes income generation (mainly via dividend-paying holdings).

Amid recent months’ Australian market weakness, IAF has seen its net asset base decline to $119m ($129m of managed assets). Its pricey 1.67% gross expense ratio (1.55% net) hasn’t changed, though, placing it at the upper end of abrdn’s actively managed fund offerings. Despite the high cost (~95bps goes to management fees), IAF is very much a ‘closet index’ fund, going by its relatively low active share (42.9). Given that actual index funds like the iShares MSCI Australia ETF (EWA) charge a far lower ~0.5% in expenses, investors should weigh the cost/benefit of IAF’s fee structure carefully.

abrdn

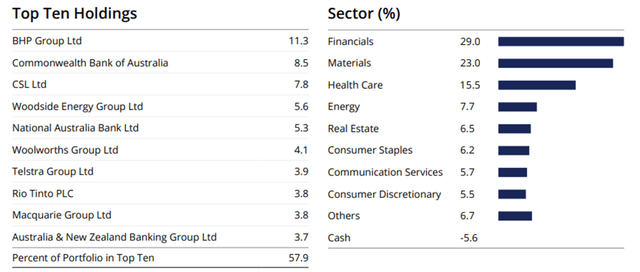

Given the fund’s low portfolio turnover, IAF’s composition doesn’t typically fluctuate too widely. In line with this view, the sector allocation remains largely in line with prior reporting, with Financials still leading the way, albeit at a higher 29.0%. Materials (23.0) and Health Care (15.5%) also remain the other major sector exposures. There’s been some reshuffling in the smaller sector allocations, with Consumer Staples now down to 6.2% in favor of Energy (7.7%) and Real Estate (6.5%). At a significant 81.7% portfolio contribution from its top five sectors, IAF investors should be mindful of the sector-specific concentration here.

The fund’s single-stock allocation is also largely in line with the changes in its ASX 200 benchmark, with mining conglomerate BHP Group (BHP) still the top holding at 11.3%. Biotechnology company CSL Limited (OTCQX:CSLLY) has declined to 7.8% and has been replaced by the Commonwealth Bank of Australia (OTCPK:CBAUF) as the second largest holding at 8.5%. On a cumulative basis, the top ten holdings now account for a larger ~58% of the overall portfolio, so IAF’s fortunes will be tied even more closely to these names going forward.

abrdn

Fund Performance – Steady Income; Sub-Par Capital Gains

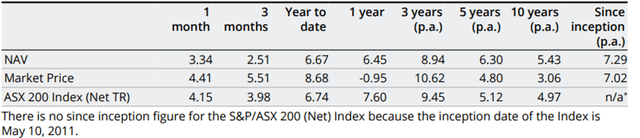

The fund has suffered further declines in recent months, with the one-year performance (in market price terms) now at -1.0%. By comparison, its benchmark ASX 200 index has returned +7.6%; even on an NAV basis (including fees and operating expenses), the fund has underperformed by over one % point. Meanwhile, investors who opted for the low-cost EWA fund would have seen a +10.5% return over the same period.

Zooming out, IAF has still outpaced its benchmark, though not by very much – per its latest factsheet, the fund’s NAV return over the last decade stands at +5.4% (vs. the ASX 200 at 5.0%). However, investing in IAF entails an NAV discount, which takes the 10-year total return down to a lackluster +3.1%. Over three and five-year timelines, the fund has underperformed by similarly wide margins in market price terms, so investors should carefully weigh the risk/reward here.

abrdn

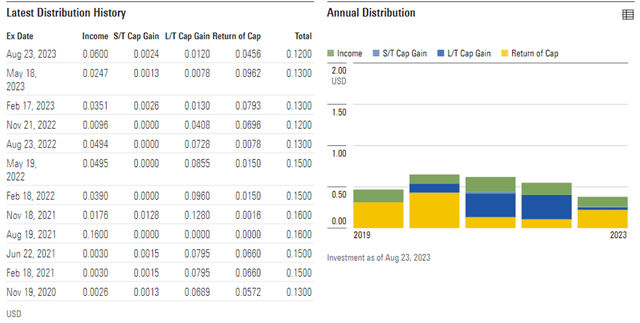

While investing in Australia comes with relatively high dividend yields, there is also an element of cyclicality in the income. IAF’s sector skew toward the major banks helps to mitigate this risk somewhat, though the fund’s exposure to materials and energy mean distributions could still drop off in a downcycle. Payouts through Q3 this year are already pacing below last year’s low-teens % total yield (~4% from the income portion excluding capital gains), and I see this slowdown extending into the next year due to China-led commodity price declines. Combined with the fund’s relative underperformance and the availability of lower fee options, I don’t see the NAV discount narrowing anytime soon – even from the current ~10%.

Morningstar

Risk/Reward Skews Negative for this Australian Fund

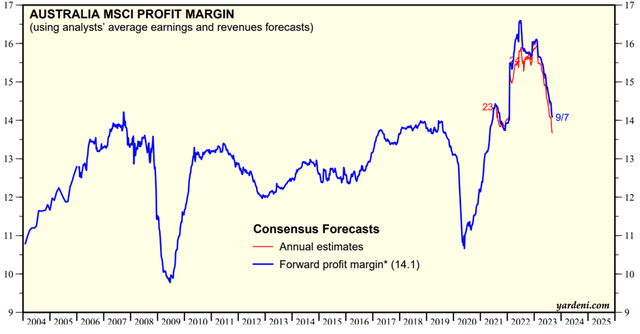

By all accounts, the Australian market isn’t looking great right now. Wage inflation pressures are already high (nominal unit labor costs up +7.5% YoY in Q2) and will stay high as increased minimum wage rates kick in. For corporate margins, expect even more cost pressures as a combination of sticky inflation and surging city rents drive a push for the next round of wage negotiations. Consumers are already feeling the heat as well (per the September headline consumer sentiment index decline), paving the way for more earnings resets for domestic-oriented stocks.

And for Australia’s major exporters (mainly energy and materials), a slowdown in US/EU and a balance sheet recession scenario for Chinese property adds a major overhang on their mid-term earnings outlook. In the meantime, the RBA’s inability to tame inflation likely means more tightening ahead, which will weigh on an equity market that continues to price in a fair bit of optimism (high-teens P/E) – despite the wave of negative earnings revisions over the last month. For now, investors would do well to look beyond Australia and the pricey IAF fund.

Yardeni

Read the full article here