Recently the Japanese equity market has rallied to a muti decade-high causing many investors to rethink their bearish outlook on Japan. This has caused growing sentiment that potentially Japan has turned a corner in that after many decades the economy could see robust growth and buying the cheaply priced equity market could be a great way to play it.

I’m very conflicted in the short to medium term. On the one hand, the valuations are very cheap in Japan and companies are starting to realise they need to be more efficient with their capital. On the other hand, Japan continues to have a negative interest rate policy and the need for future hawkish monetary policy isn’t being priced in. I’ll lay out both sides of the thesis and why Japan is on my watchlist but I’m not yet buying.

Japan As A Deep Value Play

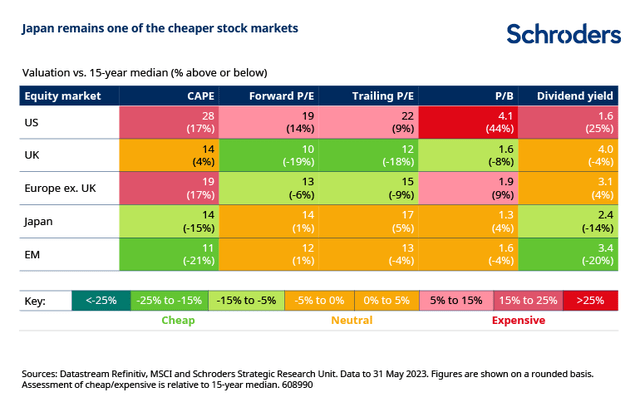

Usually, the first reason investors are attracted to Japan is valuation. Below is the valuation of Japanese equities relative to other developed markets:

Schroders

Source

Japan offers something few other countries’ equities markets can. While there are other countries that have cheap valuations they are usually frontier market countries that have political and economic stability issues. And while there are some developed countries like the UK or many middle-income countries with reasonable valuations on their equity markets they usually don’t have the wide scope of listings that Japan has; for reference, the Tokyo Stock Exchange has 3899 listings at the time of writing.

The Growth Thesis

Cheap valuations aren’t enough. What Japan has historically had is a stagnant GDP over the last three decades causing little to no growth in earnings, and along with that capital allocation from Japanese companies has been abysmal making for low ROIC.

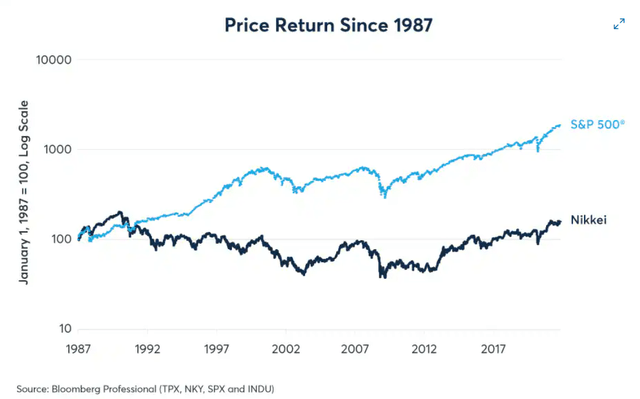

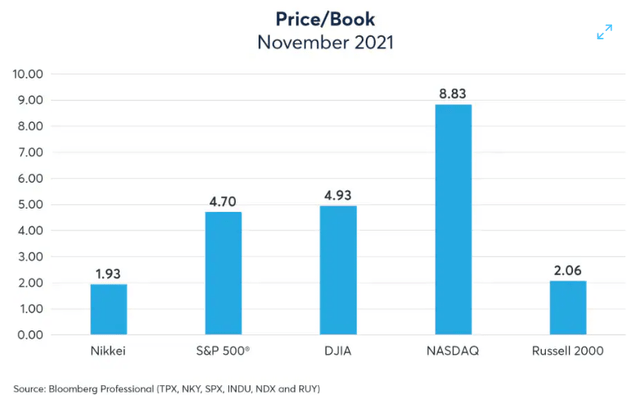

In the past, if investors compared the Japanese market to the US market the Japanese market offered lower valuations but no growth while the US did the opposite. For example, you as an investor have two choices: the first choice is a growth stock that is going for 20x earnings whose earnings will consistently grow 10% per year for the next 30 years; the second choice is a value stock going for 8x earnings with no earnings growth in the long run and the management team will reinvest the earnings at a low ROE.

In the long run, the first choice wins. Even though the second choice is cheaper, the maximum return will be 12.5% if all the capital is returned to the investor via a dividend, or worse it will be retained in the company making very little in returns. This is essentially the comparison that investors have been making between the US and Japan, as can be seen in the charts below:

CME Group

Source

CME Group

Source

Now things look to be turning a corner. Japan is seeing higher growth and higher inflation, which it hasn’t seen since 2015. Along with this companies are starting to focus on increasing their ROE.

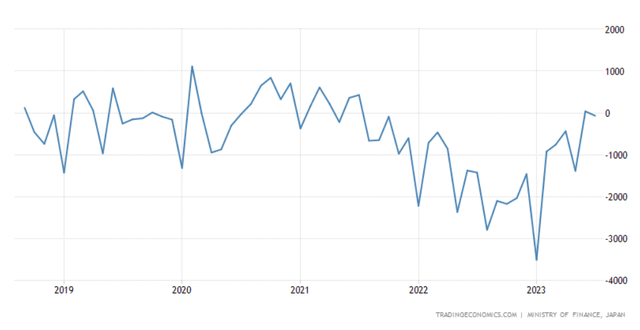

The major area of sustainable growth has been the balance of trade:

Trading Economics

Source

As can be seen, the balance of trade has become positive for the first time in two years. This is due to both a decline in imports and an increase in exports.

The biggest reason that the balance of trade has become positive is the very weak yen. As the yen has weakened against not just hard currencies but against competitor nations’ currencies like the Chinese Yuan, Japanese exports have become cheaper compared to their Chinese counterparts. On top of that the dollar is strong and the American consumer is spending more than expected over the last year. This all creates demand for Japanese exports. At the same time higher inflation and a weak yen have made for lower imports.

The BOJ’s weak yen policy is likely to continue as long as the benefits of a weak yen don’t outweigh the downside which is high inflation.

This trend doesn’t seem to be short-term in nature due to increasing geopolitical tensions. As private companies are getting out of China due to the encroachment of the CCP, their weakening economy, and increasing geopolitical risks, Japan seems like the most obvious choice to move to. The combination of cheaper Japanese products and supply chains moving away from China increases the long-term demand for Japanese products.

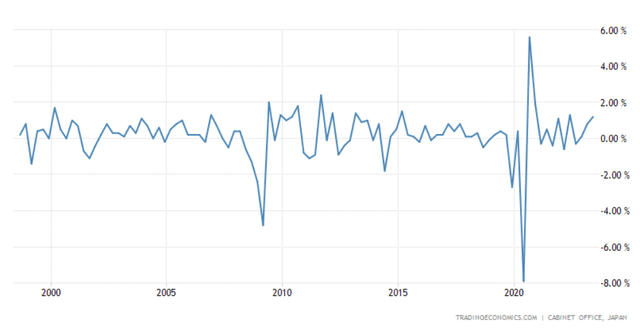

This has directly shown up in real GDP growth figures:

Trading Economics

Source

As can be seen, real GDP is growing close to 2%. If it gets above 2% then it would be the first time there in over a decade.

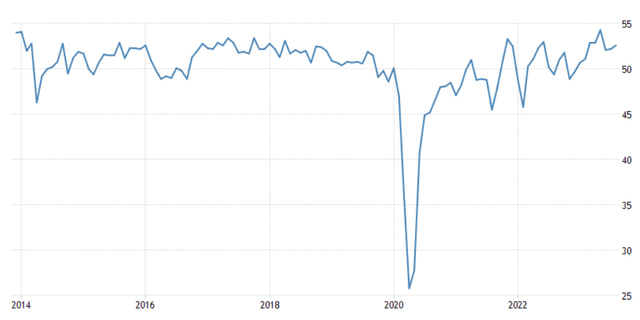

PMI figures which are often seen as a leading indicator of GDP have been shown to be very positive:

Trading Economics

Source

The recent May PMI came in at its highest in over a decade. Because of this, there’s good reason to believe that this could be the beginning of higher trend growth in GDP.

This growth story in the economy is being combined with pressure on the private sector to increase capital efficiency.

The Tokyo Stock Exchange gave a directive to all companies trading below book value that they must come up with a capital allocation plan to get their market capitalization above their book value. This is in an effort to increase capital efficiency and raise the ROE of all companies on the Tokyo Stock Exchange.

While this directive isn’t binding it does act as a warning to Japanese companies that they must become capital-efficient to attract foreign capital.

Since then companies have used this as an opportunity to increase CAPEX and take advantage of low a P/B ratio by repurchasing stock. This is all in an effort to increase ROE and thus trade at a higher P/B ratio.

What’s happened in Japan over the last year is that it went from a value investment to a growth investment. Before many would buy Japanese equities simply because they were cheap not because they felt there were any growth prospects, but now many are willing to pay higher valuations for Japanese companies because they see them as long-term compounders.

Compounder stocks is a term used to describe companies that will grow their earnings at a high rate over long periods of time and due to their capital efficiency will need to reinvest very little capital to do so. If the Japanese economy expands at a faster rate due to the previously mentioned reasons and companies increase their ROE because of the directive from the Tokyo Stock Exchange, then that is a recipe for rapid earnings growth, which is why I believe that investors are starting to see Japan as a growth story, not just a value play.

Demographics

As I mentioned at the beginning I’m of two minds on Japan; while I laid out the bullish side of things above there are still some major structural issues that will prevent secular growth from taking place.

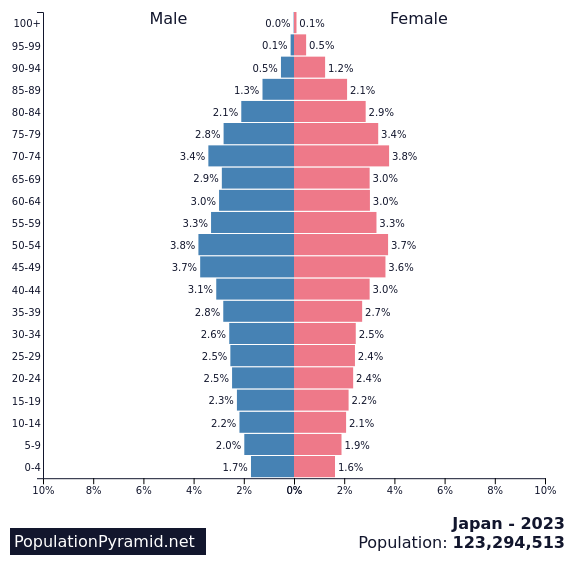

The biggest issue Japan will have to tackle is the ageing population.

Population Pyramid

Source

Above is the population pyramid of Japan as of the present. As of 2023, a third of the population is over the age of 65. With increasing longevity and low birth rates the mean populous will continue to get older.

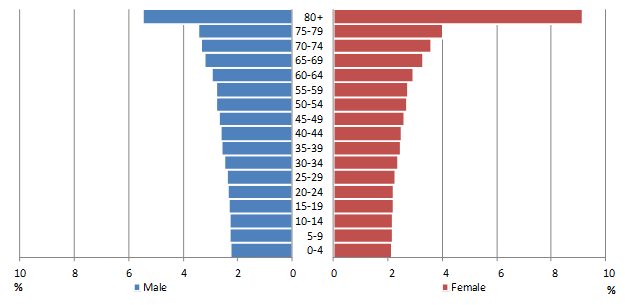

For visualization, if Japan’s birth rate were back to replacement levels in 2011, then this is the UN projected population pyramid for 2050:

PAPP IUSSP

Source

Of course, the birth rate wasn’t back to replacement levels in 2011, which is when the UN made this population pyramid estimate, so the real figures would look even worse.

At this rate in just 30 years, the average person in Japan would likely be 65+.

With a shrinking taxpayer base and increased spending on senior welfare, Japan will have to raise taxes on productive residents and local companies while likely its large budget deficits.

The demographic issue is made worse by the fact that there are no immediate solutions to it. It’s a train wreck in slow motion that can’t be stopped. The only feasible, but also politically inexpedient solution is to have a more open immigration policy, which is unlikely and comes with its own challenges.

Monetary Policy

Another major structural issue in Japan is its loose monetary policy.

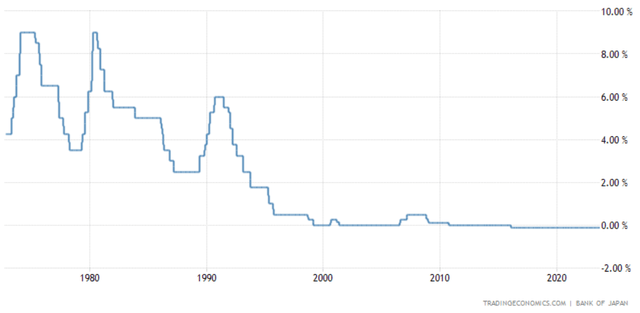

The loose monetary policy started in the 1990s when the economy went into a major downturn and the BOJ looked to stimulate the economy with lower rates:

Trading Economics

Source

Suffice it to say the low-interest rate policy didn’t work. The expectation from the BOJ was that lower rates would encourage more borrowing causing a credit boom, but that didn’t happen as investors were largely risk-off at the time due to the previous unwinding of one of the largest bubbles ever.

Japanese firms instead choose to invest overseas which offers higher returns with lower risk.

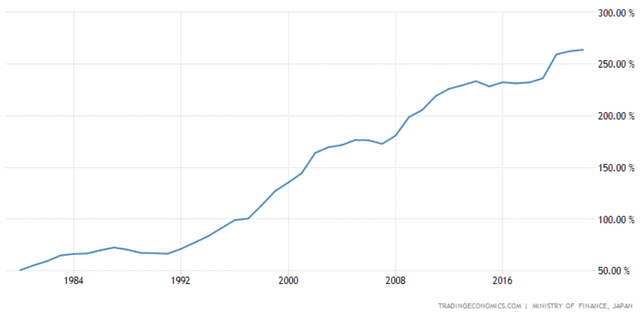

The only entity that heavily borrowed in the hopes of creating growth was the Japanese government. Due to a combination of stagnant GDP and increasing debt, Japan’s debt to GDP is now at 264%.

Debt to GDP (Trading Economics)

Source

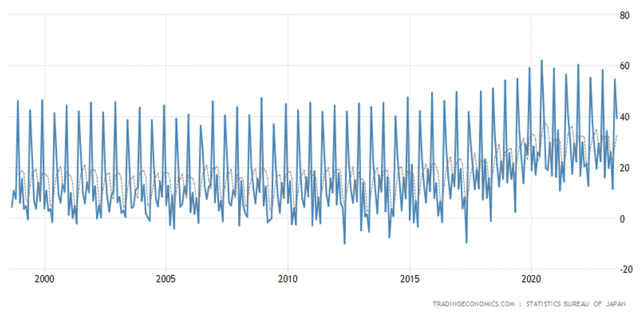

Unlike other countries such as the US, Japan is a creditor nation since its people have a very high savings rate and are essentially financing the government’s large debt by receiving no interest in their savings:

Japan Workers’ Households Ratio of Net Savings and Insurance (Trading Economics)

Source

This has caused a crowding-out effect. The Japanese would save a large percentage of their income, often in the form of government debt. The capital they saved could have instead been used to invest elsewhere where it would be more productive and cause a higher velocity of money, but instead, it is being saved in government bonds. The spending the government does wouldn’t do anything to boost long-term productivity or the velocity of the broad money supply. This causes deflation even as the number of currency units goes up.

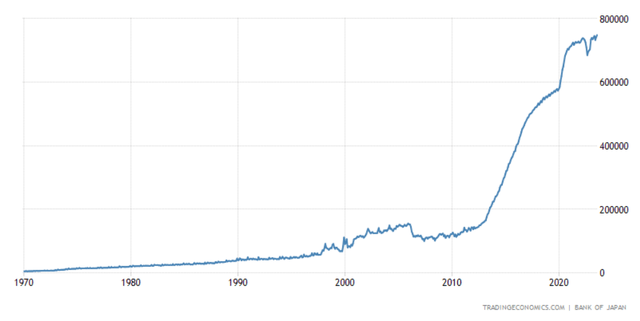

In more recent years though the focus of the central bank has been on what was originally coined as Abenomics. Essentially the focus would be on increasing base money at a faster rate and having more fiscal spending. This led to a large expansion in the balance sheet of the BOJ:

BOJ Balance Sheet (Trading Economics)

Source

The issue with just expanding the balance sheet is that it doesn’t cause a boost in the economy, instead, it just causes asset prices to go higher.

But more recently things have changed due to external impacts, primarily from the US, UK, and EU. Previously all these central banks had zero or negative rates, but over the last two years, all of them have aggressively hiked rates. Also, due to the increased risk of a recession many currencies have been seen as a potential safe haven like the dollar. This has caused the yen to weaken and import inflation from overseas.

Below is the USDJPY currency cross:

TradingView

As can be seen in a period of just two years(2021-2023) the dollar gained over 50% against the yen. This has led to both positive and negative impacts. The main positive is that Japanese exports are up due to the cheap currency and foreign investors are attracted to investments in the country due to how cheap they are in dollar terms. The biggest downside is increased inflation.

So far it seems that the BOJ believes that the upside outweighs the downside, but in my opinion, that is likely to change over the next few years.

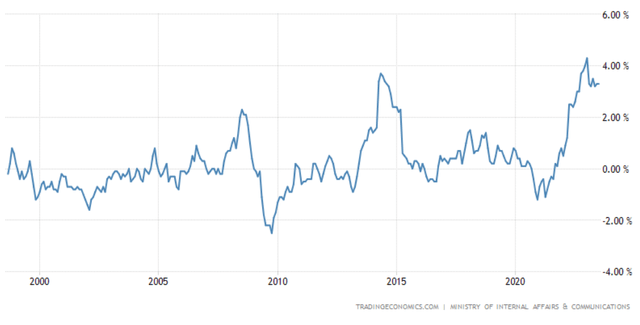

Current year-over-year inflation rate:

Inflation (Trading Economics)

Source

The current YoY inflation rate is close to 4%. This is the highest inflation since the year 1990. If the Fed continues to hike causing a stronger dollar relative to the yen then Japan could import even more inflation, leading to an inflation issue similar to what we’ve seen in the western developing world over the last three years. This brings in the risk of major rate hikes for the first time in many decades, which will likely cause asset prices to reprice to more appropriate equity risk premiums.

There is also a major difference between Japan and the US in terms of what the citizens of their respective countries want and benefit from. Americans have a lot of debt, ranging from student loans to credit cards to mortgages, and Americans are also younger with few assets. Because of this the average American benefits when there is inflation and fiscal stimulus due to debt being worth less in real terms and fiscal stimulus providing more disposable income.

On the other hand, the Japanese are older, have more savings, and have little debt. For them, inflation is a major negative as their savings which are in yen go down in value and assets get more expensive to buy; moreover, because they don’t have as much debt as their Western counterparts they don’t benefit from the inflating away of debt.

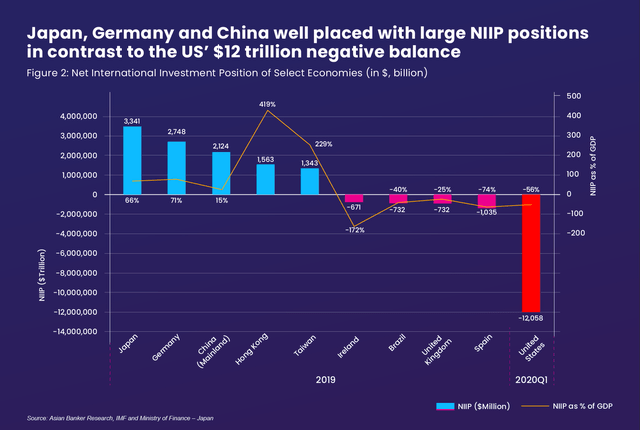

To add to that Japan is also the world’s largest creditor nation due to it having the largest net international investment position:

The Asian Banker

Source

Being the world’s largest creditor nation, Japan would be a long-term net beneficiary of higher rates, and because its private sector isn’t as leveraged as the US’s private sector it can handle higher rates.

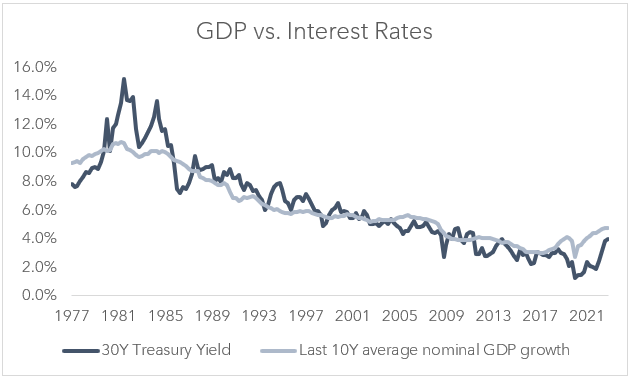

Beyond that, in the long run, interest rates and growth are correlated. For example below is the US 30-year yield relative to 10-year average GDP growth:

Fallacy Alarm

Source

As can be seen, the long end of the curve is correlated with growth. For Japan to eventually see sustainable secular growth in its GDP it will need to let the long end of the curve free from yield curve control to a far higher yield.

My view is that the risk of normalization of rates in Japan to a far higher level and the impact it has on the Japanese government’s interest payments isn’t being taken into account by equity investors.

Currency Risk

Japanese investments are stuck between a rock and a hard place when it comes to returns measured in dollars.

This is because most of the recent growth in Japan has been due to a weak yen. A weak yen and higher inflation provide a boost to the economy so the BOJ is likely to continue to keep the current policy going, but for dollar-based investors like myself and most of you reading this creates currency devaluation on our returns; and if the yen strengthened then it would likely reduce growth, so neither scenario is good.

For this reason, I don’t like plain vanilla ETFs like the MSCI Japan ETF(NYSEARCA:EWJ) which just buys a board basket of Japanese equities. There are some currency-hedged ETFs like the WisdomTree Japan Hedged Equity ETF(DXJ) which could work to capture the upside without the downside currency risk.

My preference though would be to set up a long-short portfolio where companies that are export-based are bought while those that are consumer discretionary or receiving revenue from domestic sources are shorted. This has a built-in currency hedge as when the yen weakens there is more demand for Japanese exports and less spending from the domestic market. Also, I would have a value tilt towards companies trading at a low book P/B as those stocks would most benefit from the moves being made by the Tokyo Stock Exchange.

Key Takeaways

- Lowest valuations in the developed world

- Companies are becoming more capital-efficient due to pressure from the Tokyo Stock Exchange and foreign investors

- High trend growth is likely to continue

- Major demographic issues

- Monetary policy is currently dovish making for a weak yen

- Due to Japan being the world’s largest creditor nation along with a populous that heavily saves, rates have a major risk of normalizing higher

- Rather than buying a board equity ETF like EWJ investors should focus on individual equities that are export-oriented which hedges a weak yen

- Investors should focus on investing in companies trading well below their book value

Read the full article here