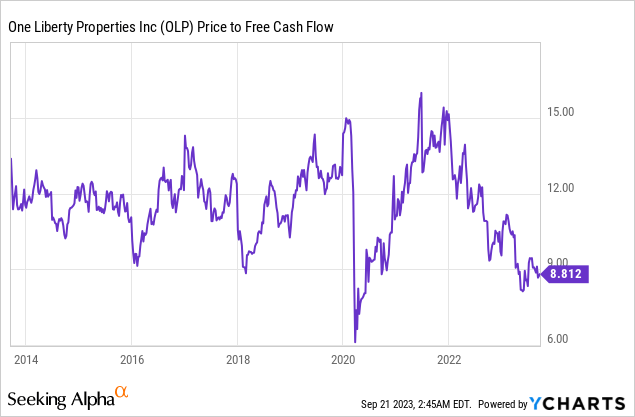

One Liberty Properties (NYSE:OLP) last declared a quarterly cash dividend of $0.45 per share, in line with its prior payment and for a 9.2% annualized forward yield. The industrial properties heavy REIT has dipped by 19% over the last year to trade at a 9.32x price to trailing 12-month funds from operations, its lowest level in years as the Fed funds rate currently sits at a 22-year high of 5.25% to 5.50% and broader concerns about the longer-term health of the US economy weigh down on the ticker. The only other time OLP was this cheap was amidst the pandemic flash crash in early 2020 with the REIT trading hands at an 8.8x price to free cash flow multiple.

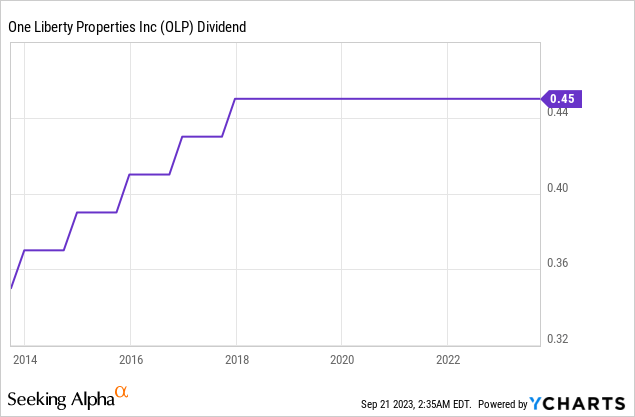

Ultimately, the income is the prize and to decide whether to make an investment in the ticker I set out to answer two fundamental points around the safety of the current dividend yield and whether I’m buying at a reasonable price. The stock has ticked the latter point with the current pullback being one of the most material in its history as the market prepares for the Fed’s higher for longer scenario that will keep the cost of capital for REITs elevated for far longer than most REIT investors would have liked. OLP has kept the current quarterly distributions stable with shareholders receiving their 45 cents per share every quarter since 2018. I like the stability, especially against the heavier pre-pandemic retail orientation of the REIT. I’d have liked to see more growth but the current yield and discount to its historical trading multiple both provide compelling mitigating factors.

The Shift To Industrial

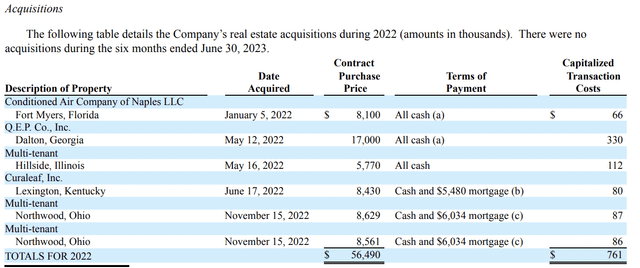

Great Neck, New York-based One Liberty Properties is an internally managed REIT with 120 properties spread across 11,310,416 square feet as of the end of its last reported fiscal 2023 second quarter. The REIT recorded second-quarter revenue of $22.41 million, a 4.4% increase over its year-ago period but a miss by $600,000 on consensus estimates. The growth in rental income comes against a wider evolution of OLP’s portfolio towards an industrial one with recent acquisitions and disposals focused on pushing forward this paradigm.

OLP most recently closed on a $13.4 million acquisition of a 177,040 square feet industrial distribution center in South Carolina. The property currently provides a gross yield of 5.85% as it comes with an aggregate annual base rent of roughly $784,000 from its two tenants. Whilst this is set to increase by 3% annually, there is a weighted average remaining lease term of 1.6 years, which management flagged as an opportunity to raise the leases to market rents in the near term.

One Liberty Properties Fiscal 2023 Second Quarter Form 10-Q

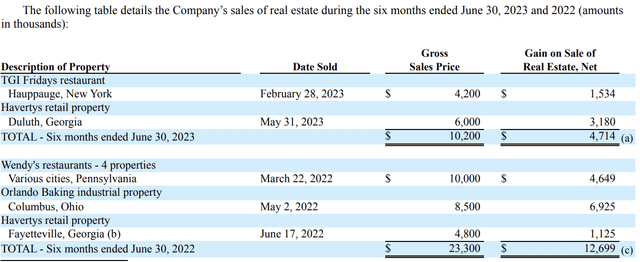

The $415 million market cap REIT spent $56.49 million on industrial property through 2023 against $23.3 million in gross property sales for the last six months. To be clear, retail does not face the same underlying headwinds as other REIT sectors like office, but the recent collapse of its tenants like Regal Cinemas (OTCPK:CNNWQ) and Bed Bath & Beyond (OTCPK:BBBYQ) highlights that the sector is not free from its own unique headwinds from legacy debt acquired during the pandemic and the partial shift of consumer spending towards more hybrid models that include e-commerce playing a stronger role. Industrial properties now account for 53 of its portfolio total and around 8,269,709 square feet.

One Liberty Properties Fiscal 2023 Second Quarter Form 10-Q

The Safety Of The Dividend

OLP reported FFO of $9.6 million, around $0.45 per share. This was down from $14.7 million, $0.69 per share, in the year-ago quarter on the back of the prior period benefitting from a large litigation settlement. Critically, adjusted FFO was $10.8 million, around $0.50 per share, and up around one cent from its year-ago comp’s AFFO of $10.4 million. It’s important to note that all of OLP’s leases are net leases which places the burden of taxes, insurance, and maintenance and repairs on the tenants.

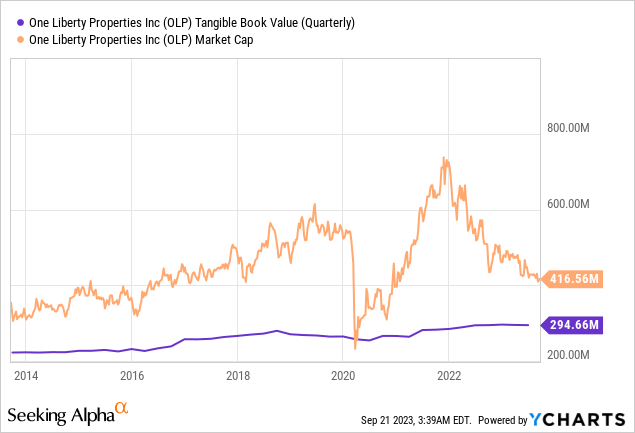

Hence, the current dividend is 111% covered by AFFO. This comes with the REIT’s premium on its tangible book value of $294 million per share, close to its shortest distance since early 2014. The relative weakness of the commons has been noticed by management, who instituted a $7.5 million stock buyback program last year, which still has around $6 million remaining as of the end of the second quarter. The company does have $82.76 million in principal payments on debt due over 2024 and 2025 which can be addressed by asset sales and its $100 million line of credit. However, this line of credit comes with an interest rate of 30-day SOFR plus an applicable margin of 175 basis points. Against the prospect of refinancing debt at ever higher interest expense, the pullback makes sense but I’m comfortable taking a position here.

Read the full article here