September 21st ended up being a really interesting day for shareholders of W. P. Carey (NYSE:WPC), a REIT that owns a diversified portfolio of real estate assets. Shares of the company closed down roughly 8% after management announced that the company will be ridding itself of its entire office portfolio. Some of the assets will be spun off, while the rest will be sold. This took investors by surprise and, what’s most interesting, is that the timeline for this all to take place is incredibly short. Obviously, the market’s reaction to the development was negative. I can understand why that is. After all, in one very important respect, the transactions very likely will make the company more expensive than it was previously. But in another respect, there is some benefit.

A look at the transactions

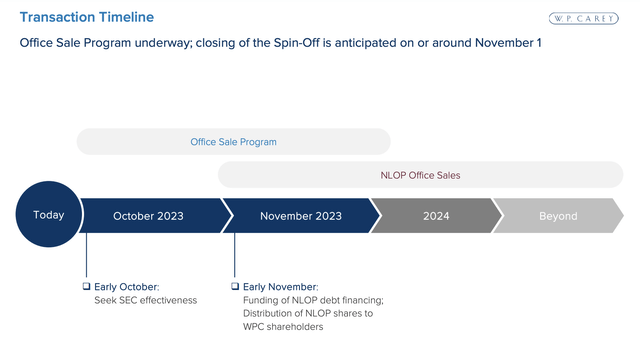

According to the press release issued by W. P. Carey, the company has decided to implement a strategic plan aimed at allowing it to exit the office real estate space. This will actually be done in two different ways. One chunk of assets will be spun off into a separate publicly traded company, with management expecting that deal to close November 1st of this year. And the rest of the assets will be sold off, with a target date for completion of January of next year.

W. P. Carey

If this comes as a surprise, I understand. But there is some very real rationale behind this maneuver. As I have written about previously, the office real estate space is facing some real troubles at this time. Earlier this year, occupancy rates across the nation were estimated to be around 50%. Even though many companies have decided to reverse course following their decisions during the pandemic to allow more people to work remote, there’s still a real threat to office property owners that occupancy rates will remain low and, as a result, that property values will tank. Management clearly sees this threat as being very real and, despite having high occupancy rates for its office assets, has made the decision to reduce risk for shareholders while simultaneously using some of the proceeds to reduce overall leverage for the enterprise.

W. P. Carey

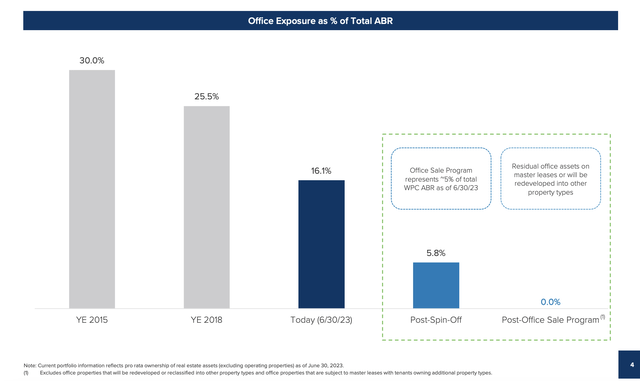

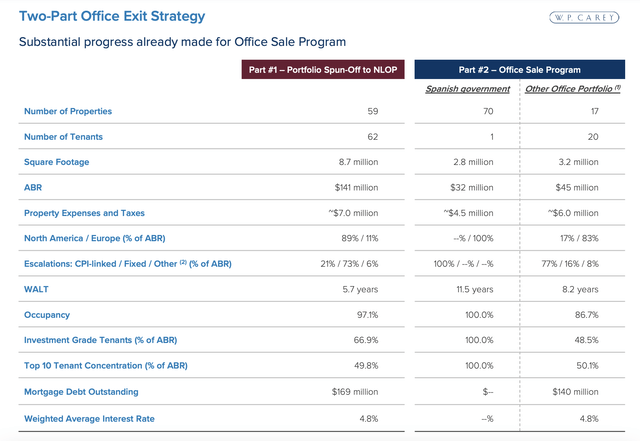

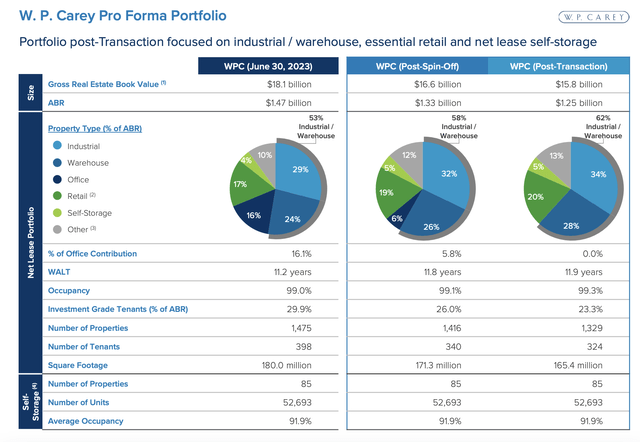

Although this announcement is abrupt, the company has been working for years to decrease its office exposure. Back in 2015, for instance, 30% of its annualized base rent, or ABR, came from office assets. Today, that number is 16.1%. After these transactions are completed, it will drop to 0%. It might be easiest to start off by describing the sale of certain assets and then move on to the more complicated spinoff. The sale side of the equation actually includes the most in terms of property count. The firm is selling off 87 properties, with 70 of those currently being leased out to the Spanish government. The other 17 are occupied by a combined 20 tenants. Collectively, these assets have six million square feet of space and generate $77 million of ABR. As far as office assets go, these seem to be quite appealing. Those that are leased out to the Spanish government have a 100% occupancy rate and 11.5-year weighted average lease term remaining. The other 17 properties included in this portfolio have an 86.7% occupancy rate and a more modest 8.2 years remaining on their leases.

W. P. Carey

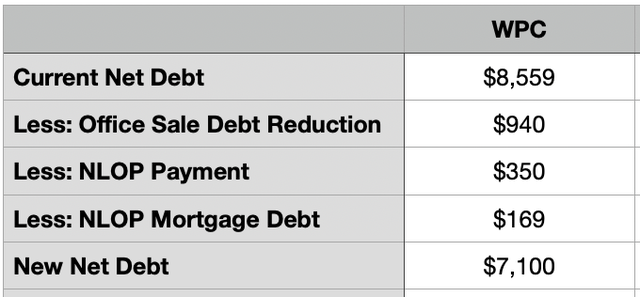

Obviously, since the firm is going through the sale process, nothing has been set in stone in terms of what price investors should receive. But management did reveal that they expect proceeds of around $800 million. In addition to this, around $140 million of mortgage debt outstanding should be transferred from W. P. Carey to the buyers of those assets. So this should give us total proceeds, without transactions costs or taxes, of $940 million if management is correct.

The other transaction involves the spinoff of certain office assets. Management is calling the company Net Lease Office Properties, or NLOP for short. This will consist of only 59 properties that are occupied by a combined 62 tenants. Although the property count is lower, square footage is higher at 8.7 million square feet. In addition to this, ABR is substantially higher at $141 million. Investors should consider these to be higher quality assets, as evidenced by the current occupancy rate stands at 97.1%. However, the weighted average lease term is considerably lower at 5.7 years. 89% of the ABR associated with these properties comes from North America, with the rest coming from Europe. To put this in perspective, the assets being sold get around 31% of their ABR from North America, with the rest coming from Europe.

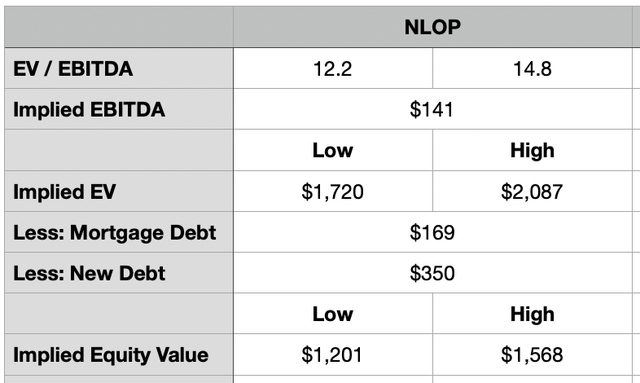

Unfortunately, we don’t have any idea what kind of value should be captured from these assets. This is something the market will decide when the spinoff takes place. But we do have some things to work with. For starters, we know that management will unload $169 million of mortgage debt onto this new publicly traded company. In addition to this, the new enterprise is receiving a $455 million credit facility, from which it will draw $350 million for the purpose of transferring to W. P. Carey.

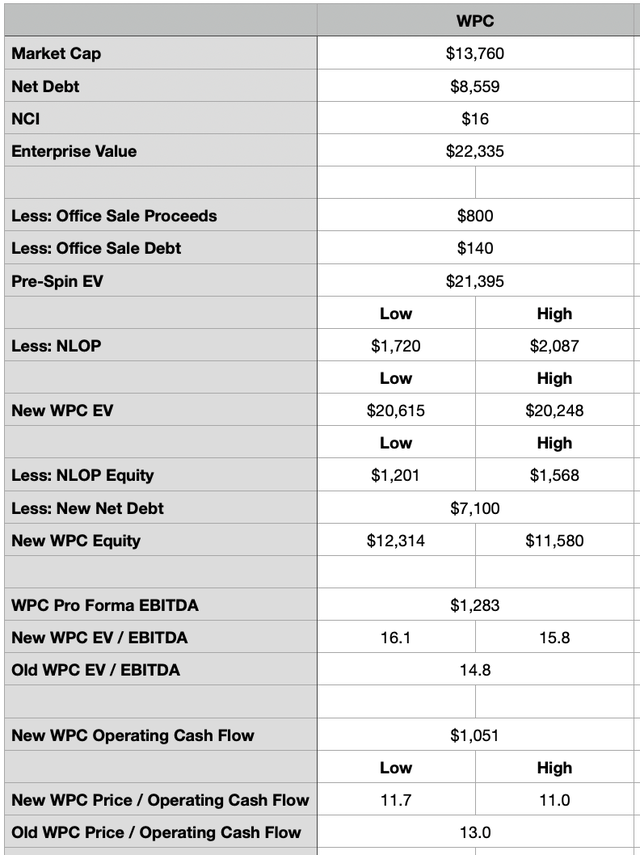

In an attempt to figure out what kind of value might exist for this standalone company, I decided to look at both a conservative scenario and a liberal scenario. But first, we need to get a little creative. While we know the ABR of these assets, we do not know the EBITDA. And the easiest way to value what is going on is by starting with the EV to EBITDA multiple. What I do know is that W. P. Carey generated annualized EBITDA of $1.51 billion during the second quarter of the company’s 2023 fiscal year. If we say that the ratio of EBITDA to ABR is the same across all of W. P. Carey today, then we would get EBITDA for the assets being sold of $79 million. And for the spinoff company, we would get $144 million. This is not the cleanest way to look at the company, mainly because it does have some other minor revenue sources besides the leasing out of its properties. The most notable is the revenue that it generates from certain operating assets. But based on my review of the company, we can’t really split all of these other revenue streams off. So we do create some risk that EBITDA for these office assets is being overstated slightly. For the purpose of conservatism, I have scaled back the EBITDA for each of these portfolios of office properties to match their ABRs.

Author

Following this approach, the assets being sold off are being done so at an EV to EBITDA multiple of 12.2. That will mark the conservative end of the spectrum. Meanwhile, prior to this announcement being made, W. P. Carey was trading at an EV to EBITDA multiple of 14.8. That will mark the liberal end of the spectrum. This would imply an enterprise value for the assets that are being spun off of between $1.72 billion and $2.09 billion. When we strip out the debt, this gets us equity of between $1.20 billion and $1.57 billion.

W. P. Carey

After this transaction is completed, W. P. Carey will generate around $1.25 billion worth of ABR per annum. This maneuver does increase the weighted average lease term of its remaining properties from 11.2 years to 11.9 years, while causing its occupancy rate to inch up from 99% to 99.3%. This on its own is most certainly positive. What’s more, 66% of its ABR will come from North America, with 33% attributable to Europe. At the end of the day, this will also result in around 62% of its ABR coming from industrial properties and warehouses. This compares to the 53% that it generates from those types of assets today. Retail will be the second largest category, accounting for 20% compared to the 17% that the company currently has.

Author

It’s unclear what exactly management will use the cash proceeds it receives for. But if they use it all toward debt reduction, the company will go from having net debt of $8.56 billion to $7.10 billion. If the company prioritizes paying off term loan debt and credit facility debt, and we factor in the mortgage debt that it is freeing itself of, then I estimate it will save around $52 million worth of interest expense annually. This should result in operating cash flow of around $1.05 billion and EBITDA of roughly $1.28 billion. Despite the reduction in net debt, the EV to EBITDA multiple for the company will rise from the 14.8 that we saw immediately before this transaction was announced to between 15.8 and 16.1. However, because of the reduction in interest expense and the equity associated with the spinoff that will be deducted from W. P. Carey, the enterprise should see its price to operating cash flow multiple decline from 13 to between 11 and 11.7.

Author

Takeaway

Based on the data that’s currently available, I can understand why some investors might be concerned about this transaction. On an EV to EBITDA basis, we are looking at the enterprise becoming more expensive than it currently is. But relative to operating cash flow, the opposite is occurring. It’s likely the end cash flow and the aforementioned concerns about the office category of assets that encouraged management to pursue this set of transactions. Frankly, I view this as being marginally positive for the firm. But it’s not quite enough to encourage me to increase my rating on it from a ‘hold’ to a ‘buy’.

Read the full article here