I used to own Mirum Pharmaceuticals (MIRM) but let go after its first approval. I covered it last in May 2022. Mirum has two drugs, maralixibat (LIVMARLI) and volixibat, targeting a set of rare liver diseases involving cholestasis, or the blockage of bile. This causes pruritus and liver damage, and the process is catalyzed by an enzyme, which these two molecules inhibit. The difference between the two – maralixibat is broad spectrum whereas volixibat is selective.

The company’s lead program was maralixibat in Alagille syndrome (ALGS), an ultra-rare disease with a market potential of $300mn. The company did well in its trials, and it was approved in September 2021. I noted how the company had a busy data drop schedule from multiple programs throughout 2022 and 2023; the label expansions would account for a 20x expansion in the target market.

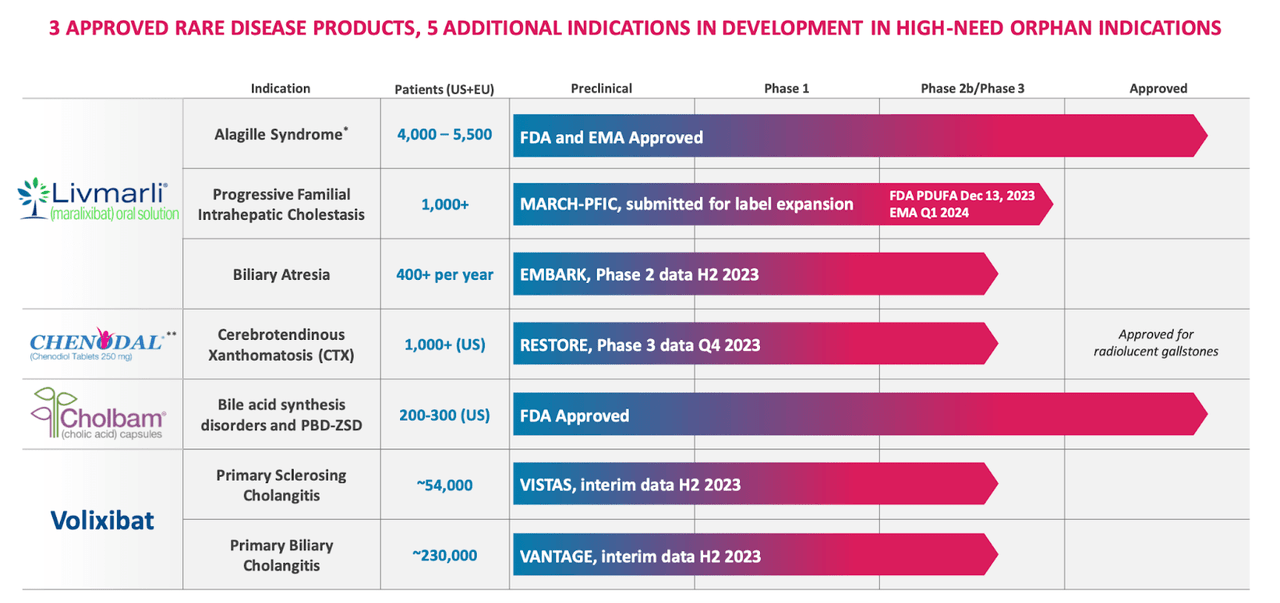

The company’s current pipeline looks like this:

MIRM Pipeline (MIRM website)

That’s a pretty impressive pipeline, although there is a bit of bill padding, in the sense that the main revenue generator here is still LIVMARLI. Its next indication is PFIC, where it produced positive phase 3 data.

PFIC is a rare, progressive disease characterized by bile acid buildup which causes pruritus and liver damage, where 80% of patients need a liver transplant to survive by the time they are 18.

In phase 3 data in a broad spectrum of patients with PFIC, i.e. All-PFIC Patients (PFIC1, PFIC2, PFIC3, PFIC4, PFIC6), maralixibat shows strong positive data. In the primary endpoint of proportion of pruritus score assessments ≤ 1 point, 62% of maralixibat patients showed an improvement versus just 28% placebo (p<0.0001) patients. Serum bile acid improvements also showed a strong positive correlation with transplant-free survival, which is the ultimate functional measure of improvement for PFIC patients. The safety profile was moderate and comparable to placebo. Overall, this was a successful trial. PDUFA is on December 13, 2023.

Other programs in various stages of development. Chenodal has a phase 3 trial running in CTX, where it has seen positive data in earlier trials. The company acquired chenodal and cholbam from Travere Therapeutics in July this year for $210 million upfront and $235 million in potential milestones., which, along with its existing liver disease programs, makes Mirum a proper liver disease franchise. These two medicines are prescribed by the same people that prescribe LIVMARLI, so there is that marketing synergy.

Besides these, Maralixibat will post data from a phase 2b trial in Biliary Atresia in H2 2023. Vorolixibat has phase 2b studies running in two types of Adult Cholestasis and will produce interim analyses from both in H2. Earlier, in a strategic acquisition, Mirum acquired Satiogen, which held rights to both its liver molecules. This reduced their royalty obligations considerably.

In June, the FDA expanded Ipsen’s Bylvay drug’s label to ALGS; however, it is approved for patients 12 months or older. Since ALGS has an onset in children below 12 months in many cases, the impact may not be much. Even so, given the small market size of ALGS, the new approval took MIRM stock down.

Financials

MIRM has a market cap of $1.2bn and a cash balance of $330mn. The company had $37.5 million total revenue, including net product sales for LIVMARLI of $32.5 million, for second quarter 2023. The company recently closed an upsized offering of $316.3 million aggregate principal amount of 4.00% convertible senior notes due 2029. R&D expenses were $22mn and G&A expenses were $32mn. At that rate, and taking into account their revenue, the company has a runway of 5-6 quarters at the least.

Most of MIRM stock is held in the hands of institutions. Key holders are Frazier, Eventide, and Biotech Value Fund. Retail holders have very little ownership here. Insiders have a decent mix of buy-and-sell transactions.

Bottomline

MIRM is a key growth stock of the sector, fast emerging as an all-rounder pediatric liver disease specialist. Its approved indications are not heavy hitters, but MIRM’s plan has always been to get its molecules approved in rare indications as proof of concept programs, and then expand them into diseases with larger markets. This is solid strategizing and has worked well for MIRM so far. Therefore, I expect this company to be a solid grower over the years unless a key program fails. Thus, this is a long-term, buy-the-dip and accumulate stock, and while I played it before its first approval, having first purchased it in the early days of the pandemic, I may just get back in again with a small pilot position.

About the TPT service

Thanks for reading. At the Total Pharma Tracker, we offer the following:-

Our Android app and website features a set of tools for DIY investors, including a work-in-progress software where you can enter any ticker and get extensive curated research material.

For investors requiring hands-on support, our in-house experts go through our tools and find the best investible stocks, complete with buy/sell strategies and alerts.

Sign up now for our free trial, request access to our tools, and find out, at no cost to you, what we can do for you.

Read the full article here