The Setup

AerCap Holdings N.V. (NYSE:AER) is an airplane, engine, and helicopter lessor led by CEO Aengus “Gus” Kelly. AerCap underwent a transformative acquisition when it acquired GECAS (GE Capital Aviation Services) in Q4 2021. Several disruptions over the past three years, including Covid and the Russia-Ukraine War, challenged the business as air travel stopped and airplanes leased to Russian airlines could not be seized. While these challenges are relatively behind the company, a significant overhang remains. GE owned 14.5% of AER stock as of 9/21/23, which they will continue to sell down, creating a near-term overhang. Once GE exits its stake, AER is far more compelling. The short-term selling pressure caps near-term upside. GE made intentions known to exit the position, which should happen by Q1 or Q2 of 2024. AerCap’s discount to BV and mid-single-digit earnings valuation is compelling enough to go long in a small starter position, increasing the position size as GE sells the remaining stake.

Business Description

AerCap is the largest aviation leasing company in the world, with a portfolio of 2,323 aircraft, engines, and helicopters owned, 718 managed, and 426 on order as of June 30, 2023. AerCap provides a wide range of assets for lease, including narrow-body and widebody aircraft, regional jets, freighters, engines, and helicopters, focusing on acquiring in-demand flight equipment at attractive prices, funding them efficiently, and hedging interest rates when prudent. In addition to their primary business, they are the world’s largest engine leasing company, with over 900 owned and managed engines.

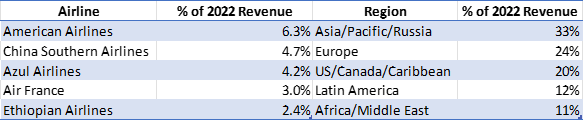

AerCap’s model is a spread business. Borrowing at a cheaper cost than airlines due to the consistent revenue stream and purchasing planes cheaper due to bulk purchases. Where the cost of debt for American Airlines in March 2023 was 7.25% for five-year notes, AerCap was able to issue 5-year debt at 5.75%. The chart below depicts AerCap’s top five customers and the geographic region of its revenue base.

AerCap Revenue Breakdown (AER 10-K)

The lower the credit rating of an airline, the higher the cost of financing, and the more likely they are to lease rather than own. High debt service costs for low credit rating companies impede running a profitable business. Instead, AerCap’s lower cost of financing allows them to act as a middleman, taking a spread above their financing cost and lending it to these riskier customers. Airlines lease a plane rather than own it for a few reasons. The first ties into the above: airlines must have access to capital to purchase a plane. The cost of an airplane can run $100m+ (more or less depending on the body type); some airlines are too small to afford this. Second, a lease does not lock an airline into a long-term commitment. Instead, they can lease a plane for 5-10 years, with the only upfront capital as a security/maintenance deposit and the first few months of rent. The maintenance deposit can be refunded at the end of the lease if the airline returns the plane in good condition. The delta between a deposit and initial rent payments compared to the outright ownership of a plane is substantial, giving the airline greater flexibility. Finally, the airline does not bear the residual value risk when the plane ends its useful life. Technological obsolescence may result in a scrapped airplane.

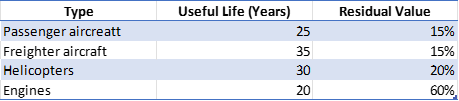

Furthermore, there are risks if the airplane manufacturer unveils new technology, such as greater fuel efficiency, more seating, or a better flying experience. Airlines may become uncompetitive due to a worse flying experience or competition offering better prices. With a lease, instead of the airline bearing this for the life of the plane, typically 25 years, the lessor bears this. The table below depicts the plane/equipment depreciation schedule and the residual value assumed. A $50m aircraft purchase has $7.5m of residual value. The risk of having an outdated plane during the early to middle of life increases for airlines with little knowledge of future demand trends. AerCap, given its broad customer base, foresight into leasing/demand trends, and database of transactions, is far more likely to be the first to know when demand and technology changes will occur.

Aircraft Depreciation Schedule (AER 10-K)

Building on the last point. Gus often discusses the value of the AerCap platform. During the year ended December 31, 2022, the company executed 895 asset transactions (sale, lease, or purchase). In previous years, they completed 349, 179, and 349 from 2019 – 2021. AerCap has an unmatched database regarding what airplanes are in demand, narrow body vs. wide body, Airbus or Boeing, is unparalleled. The most significant risk for a lessor is purchasing an out-of-demand airplane that generates minimal lease revenue and is likely out of demand when the lease renewal occurs or at the end of life, having no residual value. With more data than anyone else, the informational advantage allows them to lease planes at the best risk-adjusted rates, sell planes at the highest price, and purchase the most in-demand aircraft.

Thesis

While the above paints a positive picture for AerCap’s business, the selling pressure stemming from the GE selldown has resulted in AER’s stock declining 2% since the 15-month lockup ended on February 1, 2023, compared to the S&P 500, up 6%. A 20% drawdown coincided with GE’s first sale announcement when they filed to sell 23m shares for $58.50, $1.50 below the stock price. The most recent sale announcement occurred on September 11, selling ~47m shares at $59.00, $2.79 below the current trading price. AerCap repurchased 15.3m, lowering the shares coming to market. In seven months, the discount GE is willing to take on the shares almost doubled in seven months. GE wants the cash and not AER stock. Below, I will walk through my valuation, which makes AerCap look attractive; until this selling pressure subsides, I struggle to see how the valuation gap fully closes.

I recommend building a position as GE continues selling and reaches 3% or less of an owner. AerCap’s history of repurchasing shares should accelerate the value realization. My experience with several types of investments, where typically Private Equity or a significant shareholder sells down, is more important than business results. If results are good, the sell-down continues and could accelerate. Poor results cause further selling pressure, and a significant share sell-down results in a one-two combination of selling pressure.

Unit Economics

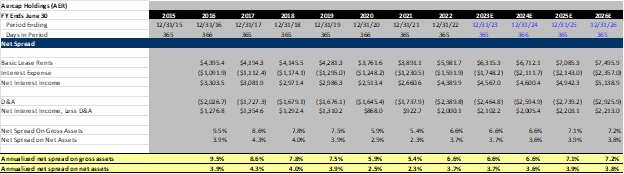

AerCap’s spread model is to issue low-cost debt, purchase aircraft at a sticker price (bulk purchase) discount, and charge lease rents at a spread over borrowing costs while factoring in the credit rating of the end customer. Its business model is similar to a bank. Borrow at low rates and lend at higher rates, adjust spreads or security deposit (for a bank down payment) for credit risk. In AerCap’s case, understanding the annualized net spread on assets gives us an idea of the margin they receive. Calculated by taking basic lease rents, subtracting interest and depreciation, and dividing by property and equipment. The table below depicts the history of this. My estimates for 2024-2026 are based upon the company’s order book, history of asset sales, and debt schedule (discussed more in the balance sheet section below)

Net Spread (AER 10-K)

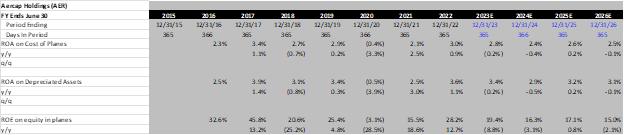

Business performance and, subsequently, the stock is similar to how a bank’s business performs. The higher return on assets (ROA) in AerCap’s case, higher return on aircraft, the better business performs. Taking it further, like a bank, AerCap uses leverage. At the end of Q2, they had net debt of $45.1B and flight equipment of $55.6B. The company’s debt/equity ratio stood at 2.5x, below their target of 2.7x. The use of leverage significantly enhances the return on equity of the company. Like a bank, where ROA’s range from 1-4%, leverage elevates the return on equity to shareholders to 8-12% on average. AerCap follows a similar playbook, with an ROA ranging from (0.5%) to 3.9% since 2015 and an ROE ranging from (3.1%) to 45.8%. (Please note this calculation is done as PP&E – debt = equity in planes).

Another calculation I run to understand how management prices leases is looking at the ROA on the cost of planes. AerCap has consistently generated a 2.1% – 3% Return on cost (excluding 2020), which is good, in my opinion.

AerCap ROA/ROE (AER 10-K)

Lease rents generate 80%+ of revenue, the remaining coming from maintenance revenue (supplemental maintenance rent based on aircraft utilization during the lease term or end-of-life-compensation based on the aircraft’s condition), gain on sale when AerCap sells an aircraft for more than its carrying value, and other income generated from claims, interest, management fees, and other miscellaneous income.

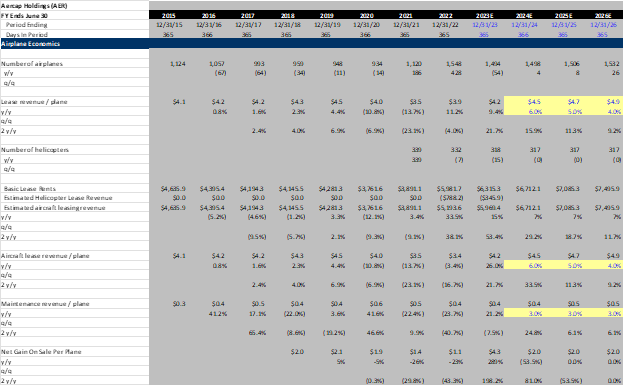

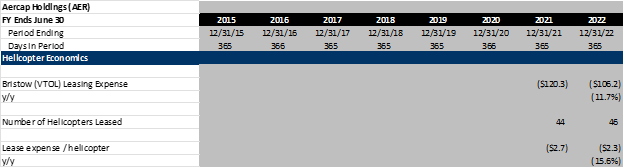

The company’s revenue per plane shows how lease rates trended. 98.2% of AerCap’s rents are fixed, and the remainder are floating rate tied to interest rates. When AER acquired GECAS, they acquired a portfolio of 300+ helicopters and an engine leasing business owning 450+ engines. One of AerCap’s customers is Bristow. Using Bristow’s leasing costs and the number of helicopters leased to calculate the leasing cost per helicopter, then applying this figure to AerCap’s helicopter business to estimate the helicopter segment revenue. I was unable to find a comp for the engine leasing business. Since 85% of AerCap’s assets are aircraft, I believe including the engine leasing revenue but not the number of engines is enough to show how leasing revenue per plane has trended.

Airplane Unit Economics (AER 10-K, VTOL 10-K)

VTOL Lease Expense (VTOL 10-K)

As shown in the spreadsheet above, in the line Aircraft lease revenue/plane, revenue per plane has not recovered to pre-pandemic levels. As lease modifications roll off and leases signed during 0% rates, leasing trends should regain and surpass pre-pandemic levels in the next 2-3 years.

Since AerCap’s cost of financing is increasing, they must pass on these higher costs to customers. Listening to Gus at the Deutsche Bank Aircraft Finance and Leasing Conference, he stated that new lease rates have moved in lockstep with interest rates. I estimate lease revenue/plane return to 2019 levels in 2024 and increase mid-single digits in subsequent years. The increase in rental income will partly be offset by higher financing costs (discussed in the balance sheet section).

AerCap has been a net seller of aircraft because they have consistently been able to sell their planes at a premium to carrying value while the stock has typically traded at or below book value. AerCap can sell planes at a premium and buy the stock at a discount. Selling a plane for a 10% premium to carrying value and purchasing the stock back at a 10% discount is a 20% spread of value creation (assuming the aircraft sale and carrying value are indicative of the remaining book).

In 2018-2019, AerCap sold ~10% of their fleet each year. During the pandemic, this figure was cut in half to ~5%, recovering in 2022 to 13%. Through Q2 23, AerCap sold 39 aircraft/engines (3.3% of fleet) at unsustainably high prices and margins. As shown in the chart below, in Q2, AerCap sold assets at almost 2x the carrying value. Historically, 1.1x-1.2x has been the norm. During the Q2 call, Aengus stated, “On the sales side, we continue to see strong and broad-based demand for our assets, closing $818 million of transactions in the quarter. This resulted in our highest-ever quarterly gain on sale of $166 million, representing a 25% margin. Encouragingly, this was not confined to aircraft assets. We also saw strong gains in our engine and helicopter sales with record volumes in each category. This further confirms the benefits of the asset diversification AerCap now enjoys.” They acknowledge these margin levels are unsustainable, so I have them returning to historical levels.

The main reasons AerCap can sell planes at a premium are twofold. First, the cost of new build aircraft has increased substantially over the past several years. Aircraft are depreciated over a 25-year useful life. Therefore, if AerCap never refurbished or reinvested into the aircraft, the value would decline 4% per year. Over the past few years, inflation ran north of this figure, so while the planes lost 4% in value each year, the cost to replace them increased at a higher rate. Inflation running at 8% and planes losing 4% of value results in a net 4% increase in resale value. Exacerbating this problem is the uncertainty around Boeing and Airbus deliveries, which puts airlines in a situation where they are unsure what their fleet size will be in a year. Paying the premium to have certainty of delivery is worth it for them, giving AerCap bargaining power.

AerCap gain on sale (AER 10-K)

Valuation

I used two valuations to develop a fair value of AerCap: a P/B and a P/E. Significant asset writedowns during 2020 resulted in a loss. Going forward, I believe AerCap’s ROE will be ~15%, which would typically warrant a P/B greater than 1x and a mid to high double-digit earnings multiple; however, time and again, like a bank goes through a recession and has increased write-offs, every decade, an unexpected event seems to occur, causing AerCap writedown assets. With this the case, a 1x P/B and 10x P/E seems reasonable. Additionally, given the leverage profile of the business, the potential for a catastrophic event is always present.

AerCap Capitalization Table (AER 10-K)

AerCap historical valuation (AER 10-K, Analyst Estimates, Dominick D’Angelo Estimates)

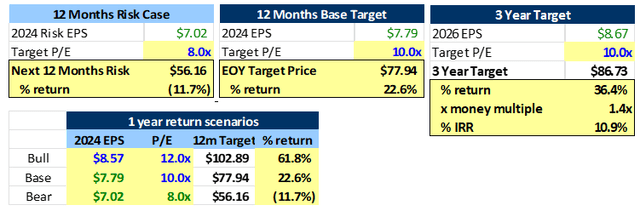

Using the P/E first and based on my analysis and estimates, my one-year price target is ~$78 with a downside of ~$56 for a 2/1 risk reward. If gain sale margins remain robust and leasing rates accelerate, I believe there could be upside to estimates and the multiple. My bull case is that the company generates ~$8.57 in EPS and, given the strong trends, trades at 12x earnings for a 62% return. With a ~5:1 upside/downside, the valuation is compelling.

AerCap P/E Valuation (Dominick D’Angelo estimates)

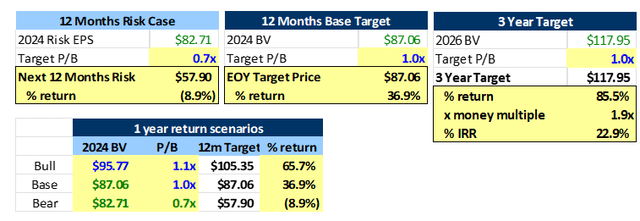

Utilizing a P/B methodology tells a similar story.

AerCap P/B Valuation (Dominick D’Angelo estimates)

Under either valuation methodology, the risk/reward is compelling. My average 12-month downside case is ~$57, base case ~$82, and upside ~$104. With a $63 stock, the risk-reward skews positive. The downside scenario would likely take several factors, including softening demand, lower leasing revenues, lower gain on sale margins, and financing costs accelerating to the upside. The bull case entails accelerating lease rates, sustained gain on sale margins, and net spread expansion.

Historically, acquisitions in the space were above book value, lending further credence to the above valuation. Fly Leasing is the sole acquisition I could find completed below book value. However, this was due to Fly’s stressed balance sheet during COVID-19.

Lessor Transaction Comps (Public Filings/Google)

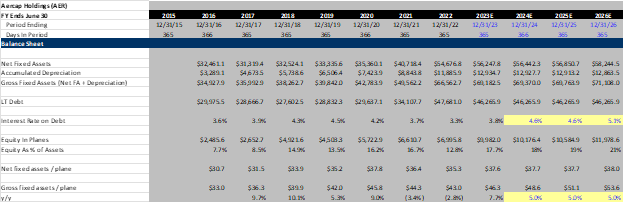

Balance Sheet

AerCap, like many financials, runs a levered balance sheet. The most important items on AER’s balance sheet are Net Fixed Assets, which are the carrying value of aircraft assets (cost – accumulated depreciation), Long-Term debt, and book equity. Before the GECAS acquisition, AerCap’s assets remained relatively stable due to the continued selling of older aircraft and the subsequent purchase of new aircraft. Debt was also relatively stable at ~$29B. As the chart below shows, AerCap’s equity in planes (Asset Value – Debt) increased since 2016. While this hurts the ROE, as the leverage declines (leverage magnifies returns), financial stability, flexibility, and downside protection increase. Previously, a 10% decline in Aircraft values wiped out equity holders. While the probability of such an event is minimal, black swan events like COVID-19 and 9/11 underscore these left-tail events. At the end of 2023, I estimate AerCap will have an equity cushion of ~18%.

While the business economics deteriorate with this higher equity (i.e., lower ROE), the catastrophic risk of the business substantially declines. A trade-off of lower returns but increased safety is one I agree with. Consider what could cause aircraft values to decline by 18%: government mandates a specific fuel efficiency, or all planes must be electric, causing AerCap’s planes to become obsolete. A global depression causes air travel to decline, leading to airline bankruptcy and lease defaults. AerCap’s inability to lease planes could cause the value of the planes to decline. Several other events are possible, but considering what would happen to the airline industry under these situations, no airline can completely transform its fleet overnight. Boeing and Airbus have limited production capacity. At some point, one can be too pessimistic.

AER Balance Sheet Data (AER 10-K)

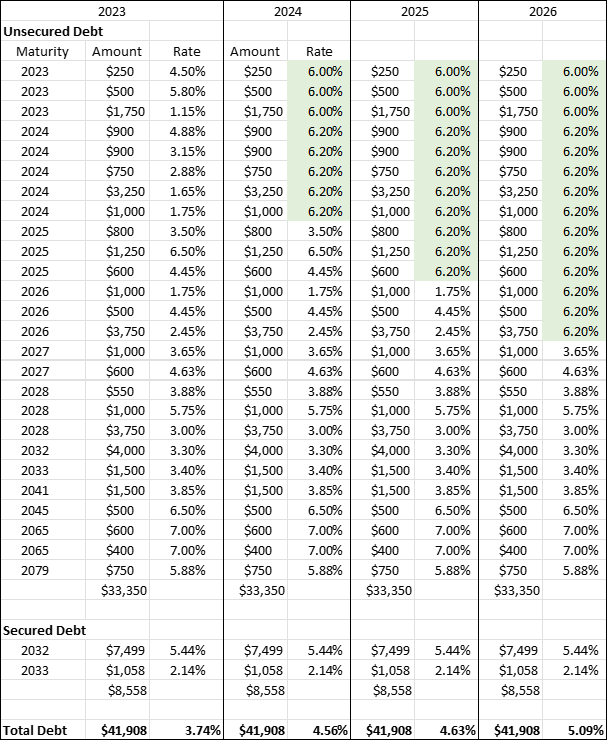

In 2023, AerCap had three bonds mature with interest rates of 4.5%, 5.8% and 1.15%. Today, the company’s cost of medium-term debt is ~6-6.5%, as discussed in the subsequent paragraph. The chart shows the company’s maturity profile and changes to its weighted average interest rate as bonds come due in the next several years. I assume the company issues medium-term debt at 6.2% (which could be low depending on where interest rates go). In 2024, the company’s average rate goes to 4.56%. In 2025 4.63%, and in 2026 5.09%. Given the low base of 3.74% in 2023, the 135 bps rate increase is a 36% increase in interest expense. Should rates continue to move higher, financing costs will further increase.

AER Maturity Schedule (AER Fixed Income Services)

AerCap recently issued 6.100% senior notes due in 2027 at 99.540% and $850M at 6.150% in 2030 at 99.371%. The debt issuance was one of the few times I questioned management’s motive. Typically, when a company issues shorter duration debt, they pay lower interest costs for it due to the upward-sloping yield curve, less uncertainty of a credit event, and lower interest rate risk (the risk that rates rise and the investor loses out by not being able to invest in the higher-yielding debt). In this case, AerCap issued 2027 2030 debt at roughly the same interest rate, likely due to the inverted yield curve. In this scenario, companies needing to refinance debt should go far out on the yield curve because the market charges them less than if they went shorter. Why AerCap would issue 2027 bonds for the same price as 2030 is puzzling, rather than issuing all the bonds in 2030.

Most financial companies run a laddered bond portfolio, issuing bonds at different durations to not have one year with substantially more maturities due than another. Again, shorter bonds generally have lower interest rates than longer. In AerCap’s case, they forced themselves to refinance debt in 2027. One can envision debt markets being closed then, yet AerCap still needs to access the markets by paying a higher rate. AerCap could have run the laddered portfolio with these bonds, even if both had 2030 maturities, by forcing or mentally noting that the plan is to refinance a portion of the debt in 2027. If debt markets are closed in 2027, it gives them a few additional years for markets to normalize. Optionality is often underappreciated.

Management

Aengus has been CEO of AerCap for over 12 years. He grew up in the aviation leasing industry (he’s only 49). I’d recommend listening to him talk. He’s honest, straightforward, and transparent. As a previous shareholder of AER, AerCap was never a company that kept me up. I trust Aengus will make the correct decisions.

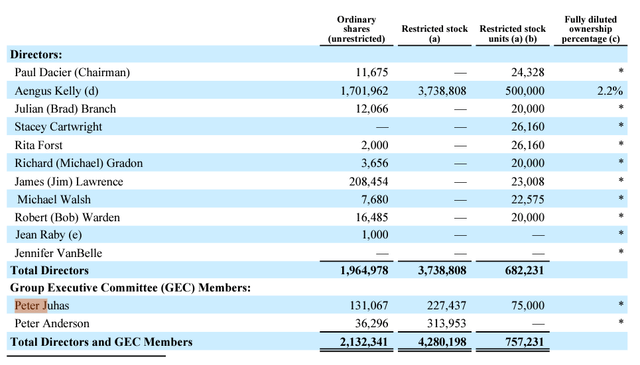

AerCap’s policy on executive ownership is that executive members must own shares valued at a minimum of 5x their annual base salary; for the CEO, the minimum is 10x. Below details management’s ownership stake. The lack of unrestricted stock ownership is concerning. Most board members own little stock and have most of their equity ownership granted through RSU’s.

AerCap insider ownership (AER 10-K)

Management’s equity compensation package is based on long-term growth, value creation, and EPS growth. I have no issue with these performance metrics because the company should become more valuable over time through BV appreciation and increasing EPS.

Risks

Demand for aircraft depends upon the demand for air travel. The main risk with owning a lessor is that air travel demand falls, resulting in less demand for their aircraft. One of the main risks management discusses is the residual value, the remaining value of the aircraft at the end of a lease. Lower demand for aircraft would result in AerCap impairing the asset. Impairments lower the book value and, therefore, the company’s fair value.

Along these lines, I’ve had the opportunity to meet Aengus and hear him speak at several conferences. He is never shy about sharing his opinion of Airplane manufacturers. Boeing and Airbus care little about the airplane’s value once they sell it to a lessor or airline. Aengus stated several times that the financial results will be poor if a company buys what Boeing and Airbus want to sell them. Instead, given AerCap’s database, they know what the most in-demand aircraft will likely be at any time, which is typically different from what the manufacturer wants to sell. This makes sense. For example, if narrow-body planes are in high demand, Boeing is likely already at max production capacity; they cannot increase production if they want to, so they have no reason to push sales for them. On the other hand, wide bodies are likely in less demand. With the excess production capacity, Boeing is out trying to sell these planes to lessors. Similarly, purchasing planes with few potential customers could be problematic. If the original lessee does not re-lease the plane, the potential to lease it to a new customer is challenging due to the lack of potential suitors.

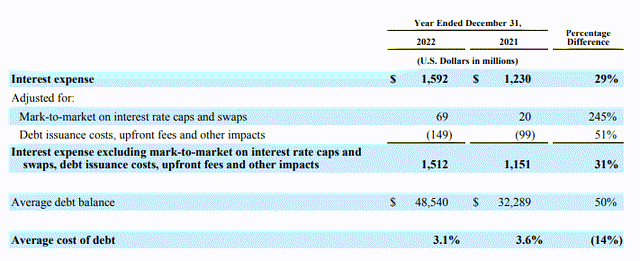

The chart below shows that AerCap’s average cost of debt in 2022 was 3.1% (different from above due to floating rate caps and swaps). Given the dramatic rise in interest rates over the past year, we know that AerCap’s debt cost will increase.

AerCap average cost of debt (AER 10-K)

In AerCap’s 20-F, they state, “As our leases are primarily for multiple years with fixed lease rates for the duration of the lease, we generally cannot increase the lease rates with respect to a particular aircraft until the expiration of the lease, even if the market is able to bear the increased lease rates. As a result, there will be a lag in our ability to adjust and pass on the costs of increasing interest rates.” If AerCap is unable to increase lease rents at a rate similar to or greater than their cost of financing increase, the company’s net spread will contract, leading to a decline in profitability.

Finally, should GE accelerate the selldown of AER shares, it could increase pressure on shares in the short term.

Q2 Results

AerCap reported strong results in Q2, headlined by a $500m repurchase authorization, book value increasing 14% y/y, and full-year adj. EPS guidance increasing to $7.50-$8.00 excluding gain on sale from $7.00 – $7.50 ($8.50 – $9.00 including gain on sale) due to strong demand trends and robust gain on sale margins. The company recorded its highest-ever gain on sale in a quarter of $166m, stating sales were strong in all segments. They have $809m of assets held for sale and are on track to sell $2.5B of assets for the year. During the quarter, they repurchased $300m worth of shares.

Subsequent to quarter end, on September 5, 2023, AerCap received cash insurance settlement proceeds of $645m from insurance claims due to the 17 aircraft and five spare engines on lease to a Russian carrier. Unsurprisingly, with the company’s proceeds, they increased the buyback authorization by $650m two days later. As of 9/7, AerCap had $1.3B remaining under its repurchase authorization, roughly 10% of today’s market cap.

Summary & Forward-Looking Items to Monitor

AerCap is cheap; however, the GE share sell-down is likely capping the upside in the short term. The best game plan is having a starter position and sizing it up as GE sells down, balancing today’s attractive price with the near-term headwinds presented. AerCap’s management team is very experienced, demand trends remain strong, and the business generates mid to high teens return on equity, which supports a higher valuation than today’s discount to BV.

Going forward, monitor the following metrics:

- Net lease spreads

- Lease revenue/plane

- Gain on sale margin

- GE ownership stake and AER buyback rate

Read the full article here