Investment Thesis

We see a good investment opportunity in Pinterest (NYSE:PINS): the company has healthy financials and a bright long-term outlook as well as a near-term trigger: the release of key figures on the Amazon (AMZN) partnership could be an important point for investors to reassess future results. Rating is BUY

ARPU is boosted by ad-spending recovery, partnership with Amazon will likely accelerate growth rates in FY2024

Previously we initiated our coverage of PINS with a HOLD rating, as stock based compensation had a strong dilutive effect on shareholder value. However, we have seen some positive signs that led us to update the rating:

- Faster-than-expected recovery in the digital advertising market.

- Amazon partnership, which will be accretive to the company’s FY2024-2025 financials.

- Moderation in research & development spending.

- $500 mln share repurchase authorization, which will offset more than 80% of FY23 dilution.

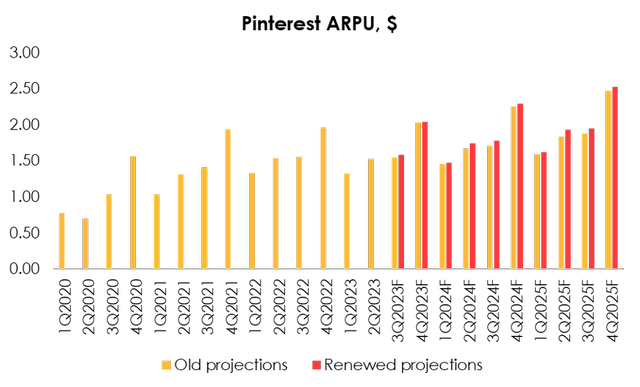

In the first quarter the average number of monthly active users reached 465 mln (+7.4% y/y). The company saw some recovery in average revenue per user as the metric reached $1.53 (-0.8% y/y). Pinterest continues to develop digital marketing, using AI-powered models for targeting and recommendations, which strengthens user engagement and drives customer demand.

We believe that the advertising market has begun a steady recovery (as evidenced by reports from major industry players such as Alphabet – see management’s discussion on YouTube’s performance) and will gain momentum in the second half of the year. Pinterest management itself has noted that there are signs of a recovery in the marketing activity, which has led us to reduce the expected impact of declining budgets from smaller clients on Pinterest’s ARPU.

Invest Heroes

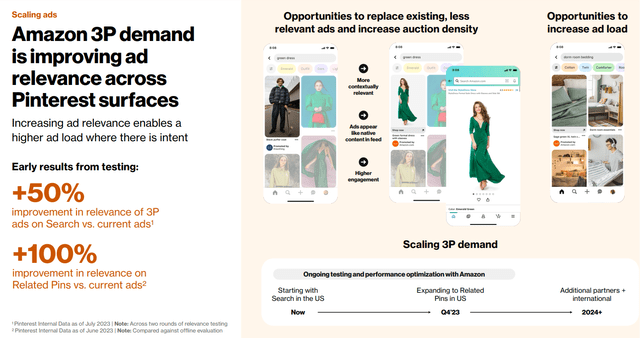

In April, Pinterest announced a partnership with Amazon, and is currently in the process of technical preparations and traffic analysis. Management has made preliminary positive comments about the deal, but the full effect of the synergy is not expected to be felt until 2024, after the platforms are fully integrated, according to management guidance.

At its Investor Day Pinterest presented early numbers from its partnership with Amazon. According to the company, the new deal increases the ad-load of the service and the quality of ad relevance, compared to standard pins. We believe the new feature will drive ARPU, which is why we increased our ARPU relative-to-market multiple from 1.13x to 1.35x in FY2024.

Pinterest

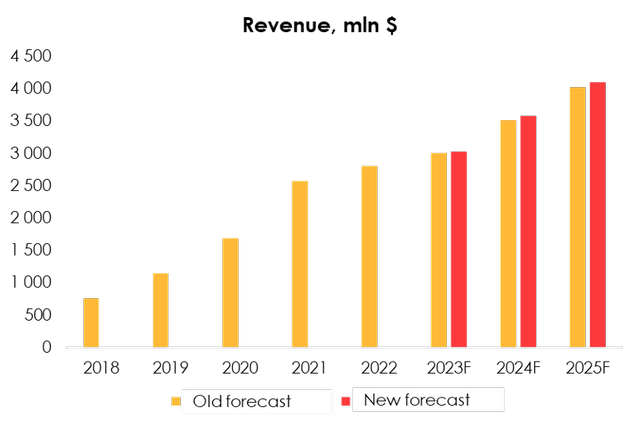

We are forecasting the revenue of $3,022 mln (+7.8% y/y) in 2023 and of $3,579 mln (+18.5% y/y) in 2024 amid a faster recovery of the advertising market and the estimated effect from the Amazon deal.

Invest Heroes

PINS is likely to achieve breakeven without dilution

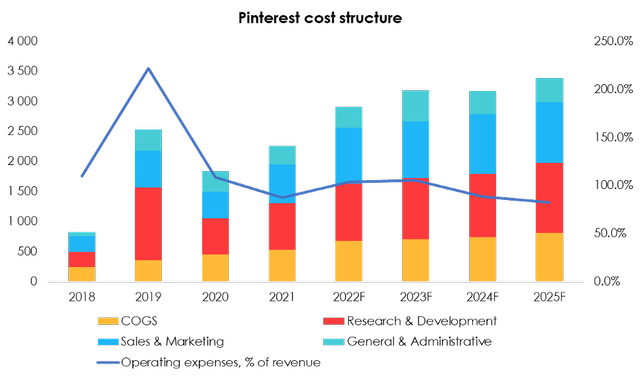

There’s still a lot of uncertainty around operating expenses, as Pinterest’s spending is largely driven by Research & Development. In 2022, the company has ran into problems as its marketing and research budgets increased significantly, while revenue growth was moderate. However, ARPU is accelerating again and the main cycle of R&D investments seems to be over (after the launch of Shopping API, short video editor, seller analytics tools, etc).

Invest Heroes

In Q2 Pinterest’s profitability also showed a positive trend, as its operating costs totaled $612 mln (+4.9% y/y). Most of the impact came from the cost reduction in R&D costs to $269 mln (+15.4% y/y). This is also a sign why we believe that the main cycle of investment in the functionality of the service is over and the company will only improve its margins going forward.

With costs declining at a faster pace, we forecast R&D spending of $1,019 mln (+7.4% y/y) in 2023 and of $1,050 mln in 2024 (+3% y/y).

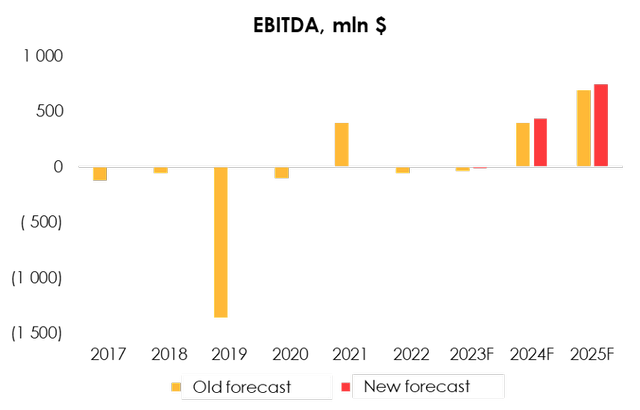

Therefore, we set the EBITDA forecast at ($8) mln for 2023 and at $438 mln for 2024.

Invest Heroes

The current dilutive effect will be partly mitigated by the buyback program. We expect total stock-based compensation to be ~590 mln in FY2023, while repurchases will be $500 mln.

Risks section

In general, Pinterest business is subject to the following risk factors:

- Advertising market recession and declining ARPU’s, as it happened in FY2022. We have issued this assumption as a base case scenario in our previous related articles: (e.g. Alphabet: Deepening into Market Recession). However, this is unlikely to be detrimental to PINS in the near term, as signs of advertiser spending acceleration have been observed.

- Competition. Advertising is a very competitive market and there are a lot of players, and Amazon is also entering the industry. We believe that Pinterest is well-positioned in this regard due to: 1) organic integration of value-added products into a service, that remains shareware for most of the users; 2) collaboration policy; 3) relatively niche product & subsector; 4) loyal audience.

- Inability of monetizing new features in international markets or stagnation of international ARPU’s. This is our most important and most practical point.

Valuation

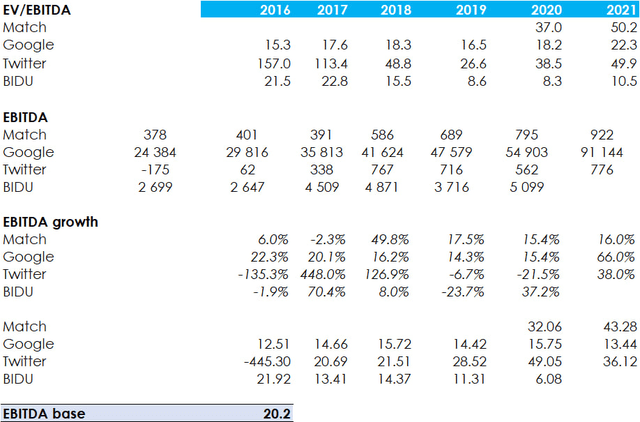

For valuation purposes, we use the historical peer multiples adjusted for EBITDA growth: Multiple/(1+[EBITDA growth rate]). Then we adjust the selection in order to remove data anomalies. Our average industry multiple is calculated to be 20.2x. This is multiplied by the average PINS EBITDA growth rate, which conceptually implies that financial performance will improve significantly in the future, resulting in a higher relative valuation.

SeekingAlpha

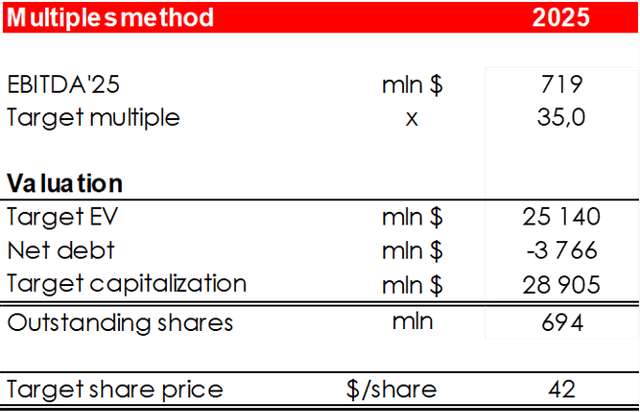

We’re evaluating Pinterest stock’s fair price based on a discount rate at 13% per annum 2025 EV/EBITDA multiple. The target price of the shares is $35. The price below is depicted without 13% discount.

Invest Heroes

Conclusion

Pinterest looks like a good choice for long-term investors looking for serious returns. Organic revenue growth will be supported by both a recovery in advertising spending and Pinterest’s exclusive features (the company is already on its way to becoming an online marketplace). The Amazon deal is likely to be a serious support for PINS and the shares could potentially jump on its Investors Day when Pinterest will disclose key numbers.

To manage your positions we recommend to follow Pinterest and industry peers (Alphabet, Meta, Snap) earnings releases and industry research (Dentsu, eMarketer, McKinsey).

Read the full article here