My Thesis

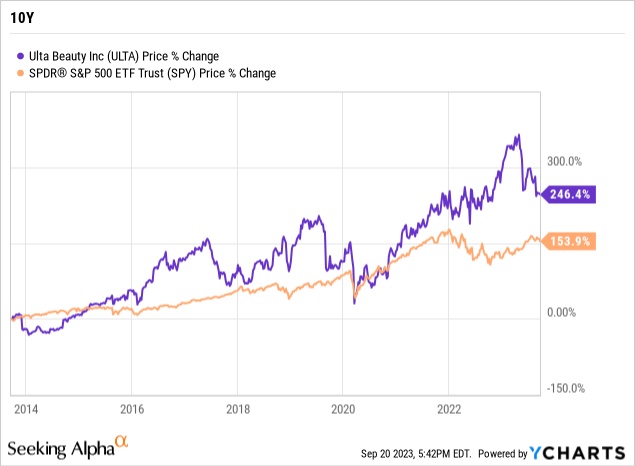

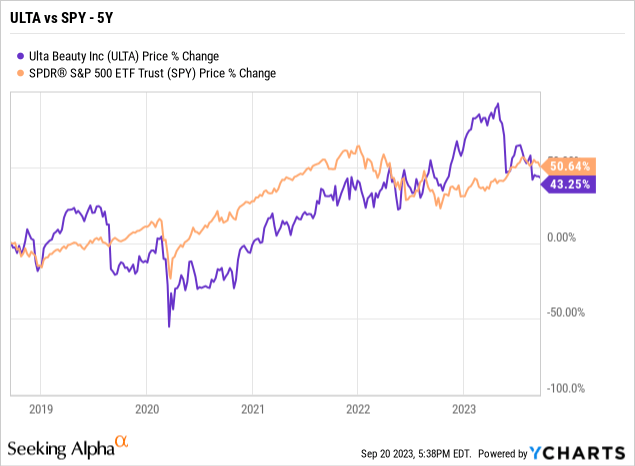

Over the past five years, Ulta’s (NASDAQ:ULTA) stock has encountered a challenging period despite its resilient financials, consistently underperforming the S&P 500 index. The reasons behind this trend remain unclear. However, I believe that this downward trend is unlikely to continue, and there is a strong possibility that the stock will revert to its historical pattern of outperformance observed over the past decade.

Ulta is a high-quality compounder, renowned for delivering significant growth in both its top and bottom lines, complemented by outstanding returns on capital. Its straightforward business model further enhances its appeal. Given its current price, Ulta may offer an enticing buying opportunity. When quality aligns with favorable pricing, it often beckons investors to take action.

The Business and its Moat

In my assessment, Ulta stands out as one of the most attractive brands for private investors to consider owning. This appeal is rooted in its straightforwardness, which facilitates more accessible analysis and predictability. As a private investor who has drawn significant inspiration from investment luminaries such as Terry Smith and Peter Lynch, I firmly believe that Ulta aligns with the standards set by both of these legendary investors.

From Smith’s perspective, Ulta represents a high-quality business characterized by predictability, consistently delivering impressive returns on capital, and demonstrating a robust history of brand loyalty, even during challenging periods.

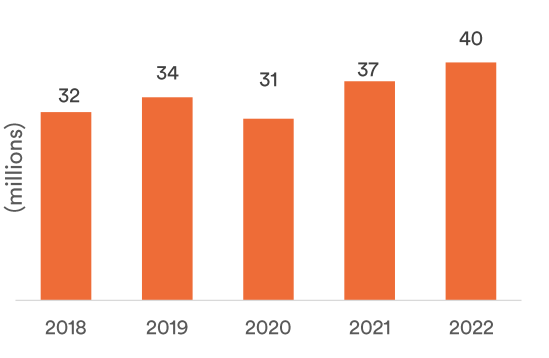

From a Lynch standpoint, Ulta’s growth over the past few years has been visibly evident, with the company opening 281 new stores between 2018 and 2022. This expansion is one of the three key avenues through which Ulta achieves growth, with the other two aspects set to be discussed in greater detail later. Furthermore, Ulta boasts a strong customer base, with “beauty enthusiasts” accounting for 83% of their sales. These beauty enthusiasts primarily comprise Ultamate members, who account for approximately 95% of Ulta’s sales. Notably, Ulta boasts a significant and continually growing membership base, which reached 40 million as of 2022 (see chart).

Ultamate members (Ulta IR)

Beyond its retail operations, Ulta also encompasses a services business, offering services such as haircuts, among others. Customers availing these services tend to exhibit higher spending patterns, typically three times the annual spending of a regular customer. Moreover, they visit Ulta stores approximately five times more frequently in a year than the average customer. Additionally, there is a 50% likelihood that they will make a product purchase on the day of their service appointment.

Furthermore, in addition to its 1,350 standalone stores, Ulta operates within 420 Target (TGT) locations—a noteworthy collaboration that appears to be successful, given the ongoing expansion of these co-located stores. These in-store locations offer a similar shopping experience to that of Ulta’s standalone stores, conveniently housed within Target.

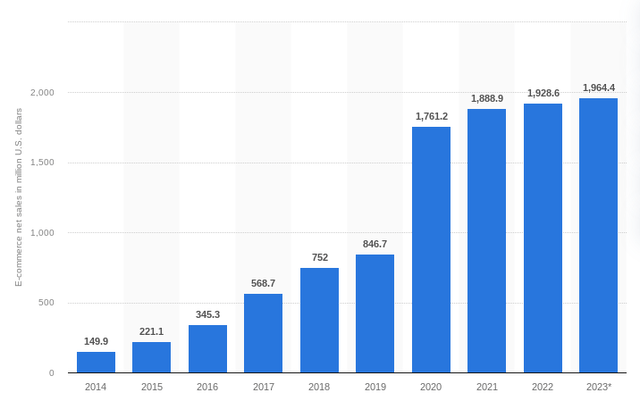

Ulta also operates an e-commerce division, contributing to the seamless omnichannel integration between its physical and online presence. E-commerce currently accounts for approximately 22% of Ulta’s total sales. However, it’s worth noting that growth in this segment has somewhat plateaued since the initial surge during the COVID-19 pandemic. It would be prudent to see management take proactive measures to enhance the performance of this segment (refer to the chart).

E-commerce net sales of ulta.com from 2014 to 2023 (Statista)

The Brand

Ulta emerged as the most favored ‘beauty destination’ for 42% of the surveyed female teenagers. The survey further revealed that 39% of female teenagers are participants in beauty loyalty programs, with Ulta’s ULTAmate Rewards program constituting 62% of the total membership. It is noteworthy that beauty loyalty program memberships at Ulta showed a marginal decrease compared to the spring 2022 survey.

It is imperative to analyze the distinguishing characteristics that set Ulta apart. Unlike Sephora (OTCPK:LVMHF), which primarily offers luxury products, Ulta boasts a portfolio of 600 brands catering to a broader customer base while also maintaining a luxury department. Ulta is renowned for its exceptional guest experience and extensive product selection. For beauty enthusiasts, it is akin to a haven.

Ulta effectively engages customers through influencer collaborations, leveraging its substantial Instagram following of 7 million, which holds significant sway among teenagers. In an industry marked by rapid changes and the necessity to stay relevant, Ulta has demonstrated adeptness in this regard. The company has managed to achieve sustained growth since the 1990s, a period marked by profound shifts, including the surge in e-commerce.

Moving forward, Ulta will need to continue identifying and promoting trending brands like e.l.f. (ELF) to maintain its competitive edge. However, amidst the intense competition within the retail sector, what truly sets Ulta apart is its unwavering focus on the beauty market. Unlike mammoth competitors such as Walmart (WMT) and Amazon (AMZN), customers seek the specialized experience that Ulta provides when shopping for beauty products.

Quantitative Analysis

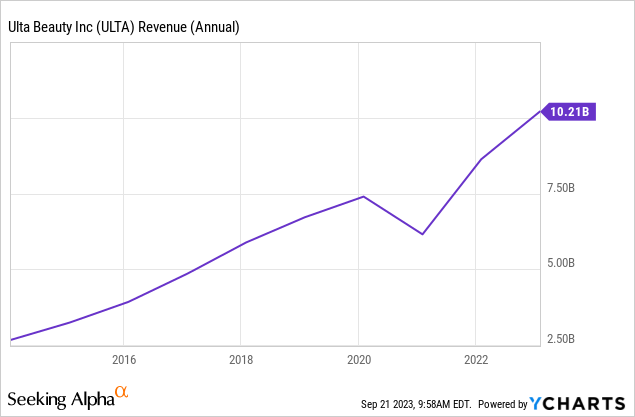

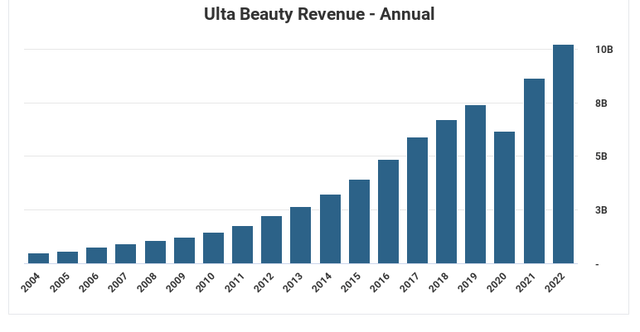

Ulta has effectively managed to achieve remarkable growth in its top line. Over the past decade, Ulta has maintained an impressive average annual growth rate (CAGR) of 15%, a commendable feat. Nevertheless, the outlook for such robust growth in the future is less certain. Analysts project a more moderate growth rate of 7% for the next three years, a figure that aligns with the firm’s maturing stage. This point holds particular significance in the context of valuation analysis, which we will delve into later.

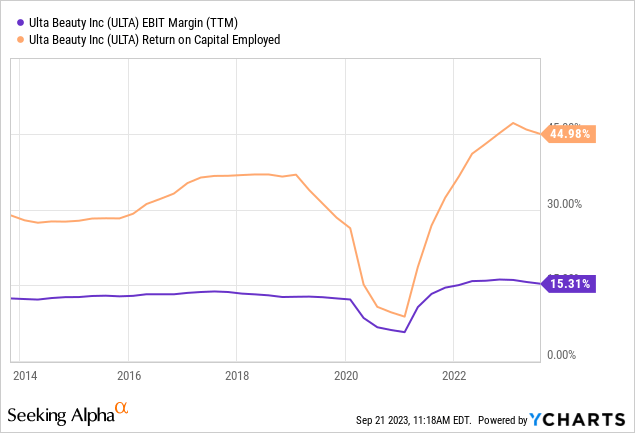

From an EBIT perspective, the company has exhibited robust growth with an 18% compound annual growth rate (CAGR), showcasing operating leverage, which has resulted in margin expansion and heightened efficiency. The EBIT margin achieved by Ulta is noteworthy, especially within the context of the retail industry, where margins typically do not exceed 10%.

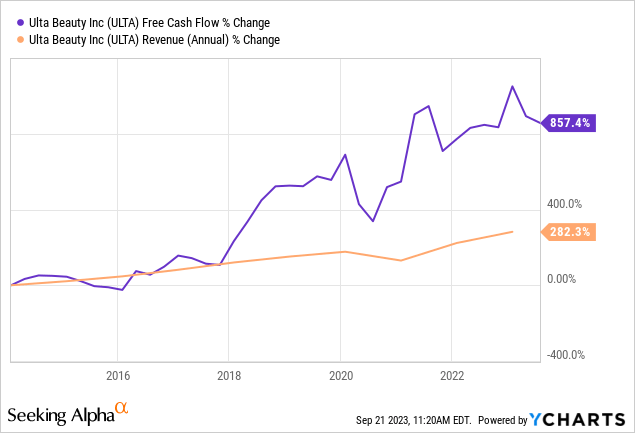

The growth in free cash flow has been exceptional, averaging a 54% CAGR over the past decade. However, it is essential to acknowledge that over the long term, FCF growth tends to align with revenue growth, given the inherent limitations to efficiency. The FCF margin, currently standing at 8%, is commendable for a retailer.

These margin expansion and top-line growth achievements have significantly contributed to Ulta’s returns on capital, figures that hold paramount importance in my perspective. Ulta has accomplished an impressive 46% return on capital employed (ROCE) and a commendable 31% return on invested capital (ROIC). These ratios are critical factors in the context of long-term compounding.

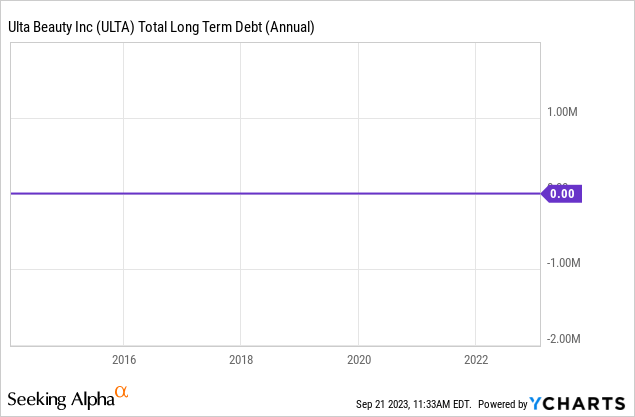

Ulta maintains a robust balance sheet, boasting $388.6 million in cash reserves and, notably, zero debt—a commendable financial position. However, in recent years, the company could have leveraged the low-interest-rate environment, as many other firms have done, to secure debt and employ it for growth-enhancing investments, potentially amplifying returns on capital. In the current high-interest-rate environment, such a move might not be advisable. Nevertheless, the absence of debt on Ulta’s balance sheet remains a positive aspect for the time being.

Ulta, while not paying dividends, has been actively engaged in share buybacks. This strategy has significantly contributed to the impressive growth in earnings per share (EPS), achieving a remarkable 23% CAGR over the past decade. It is important to note that share buybacks can sometimes be executed at inopportune times, with management making purchases when shares are overvalued. Nevertheless, in many cases, I view buybacks as a more favorable option compared to pursuing M&A’s, a strategy often pursued by many companies.

Additional Traits

Ulta operates within the beauty industry, a sector known for its resilience even in challenging economic times. As evidenced by the slowdown experienced this year, Ulta has managed to maintain its top-line performance. While free cash flow saw a decrease, this was primarily attributed to an increase in capital expenditures (capex), which is expected to drive growth in 2024 and beyond.

This unique trait of resilience was also observed during the financial crisis of 2008, as the company sustained its top-line growth without significant disruption. The beauty industry’s enduring appeal lies in its fundamental nature; it is safe to assume that most women continue to prioritize self-care, even during difficult economic periods.

Ulta Beauty Revenue (Stock Analysis)

Ulta’s management team consists of 10 members, with 7 of them being women—an aspect that I consider critical, given that 80% of the company’s customers are women. Understanding the customer base is crucial, and having women in key leadership roles can be advantageous in this regard.

Dave Kimbell, who assumed the role of CEO in 2021, has been with the company since 2014. Assessing his performance will require time. However, during his two years in the position, Ulta has continued on its profitable trajectory. It is noteworthy that he is currently directing investments in capex, with the anticipation of yielding results in the coming years. This strategic approach is generally viewed positively, although it should be monitored, especially if the free cash flow experiences an extended period of decline, potentially affecting Ulta’s returns on capital.

Exploring Risks

I hold a favorable view of Ulta primarily because of its simplicity and predictability, which, in turn, facilitates a better assessment of risks. Nevertheless, it is important to acknowledge that risks do exist. These risks include a heavy reliance on the U.S. market, which may necessitate expansion beyond U.S. borders in the future, requiring an examination of consumer preferences in new markets.

Operating within the retail sector, albeit as a niche retailer, exposes Ulta to intense competition. Competitors such as LVMH’s Sephora, as well as giants like Amazon and Walmart, pose formidable challenges. Another risk associated with the company’s focus on the U.S. market is vulnerability to a severe recession. While Ulta’s performance may outshine that of others during such downturns, the absence of international revenue streams remains a concern.

However, the central risk that warrants thorough discussion pertains to Ulta’s valuation. This aspect will be explored in greater detail, as it represents a critical juncture where the company’s attractiveness could either prove to be a gem or potentially a trap.

You could, in fact, continue to identify more risks, and I encourage you to do so.

Finally, Valuation

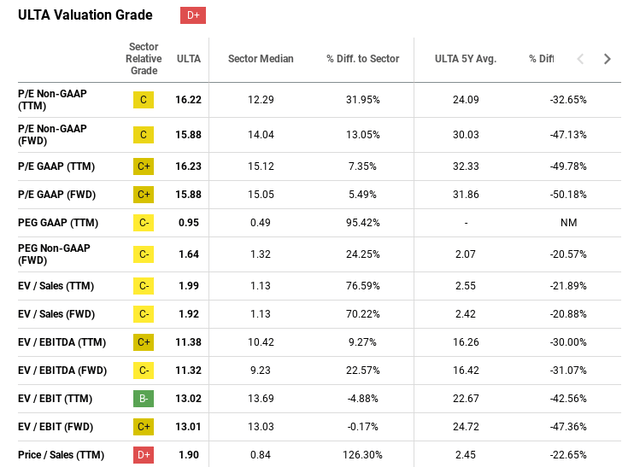

Ulta has garnered the interest of value investors, primarily due to its appeal relative to its historical performance. The company’s current valuation trades below its historical multiples, and in some cases, significantly so. This presents the potential for multiple expansion, a scenario that value investors find compelling.

However, it is essential to recognize that the past five years have been characterized by a low-interest-rate environment, and the prospects for lower multiples, partly due to Quantitative Tightening (QT), present a more intricate situation. While acknowledging this complexity, I perceive Ulta as a favorable choice, particularly in anticipation of challenging economic conditions.

Multiples (Seeking Alpha)

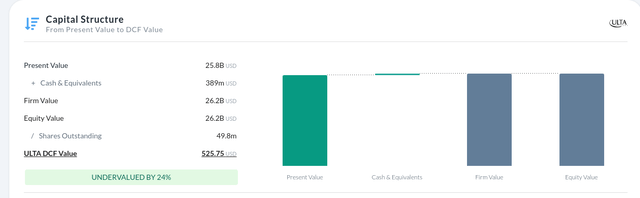

From a discounted cash flow perspective, the situation may appear less compelling, primarily due to the lower anticipated growth in the near future. I have employed relatively realistic inputs, albeit not overly conservative. The growth rate is set at 7%, aligning with Wall Street analysts’ forecasts. While historical growth rates were higher, the current economic environment necessitates a more cautious outlook. The terminal growth rate is standing at 2%, with an EBIT margin of 15% (a somewhat optimistic assumption, based on last year’s figures). The tax rate is projected at 24%, and the model spans over a 5-year horizon. The discount rate, calculated using the WACC method, stands at 8.2%.

Based on these inputs, the intrinsic value price is estimated at $525, which represents a 24% margin of safety. This figure may be perceived as compelling by some investors, while others may exercise caution.

DCF (Alpha Spread)

Conclusion

I am an investor with a significantly long-term horizon, and as such, I view Ulta as an attractive opportunity. I understand, however, why some investors may remain skeptical given the company’s underperformance over the past five years.

In my assessment, Ulta stands as a superior company, particularly within the realm of retailers, and I envision a promising future ahead. The current valuation appears reasonable, and the company boasts a wide moat. I do not discern major reasons to expect continued underperformance, but, as we all know, the stock market is a realm of possibilities.

I would appreciate hearing your thoughts on this matter.

Read the full article here