Honda (NYSE:HMC) has major factories in the US, but Japanese automakers all around are big exporters of physical vehicles manufactured in Japan that make it over the sea to American markets, where Japanese players have serious market share. Honda has around 6-7% market share in the US, but we think that in addition to the already beneficial developments in the Yen, which remains much weaker than we expected it to be a year ago by this time, the UAW strikes further put the Japanese cars ahead of local automakers as car purchases are still supposed to catch up to pre-COVID levels. We are overweight Japanese auto including a low PE and TSE-supported Honda.

UAW Strikes and Honda Breakdown

The UAW strikes are a trending issue, as they should be. They remind other industries as well that there’s a meaningful economic impact from having to commit to double-digit wage increases that will be an earnings headwind for years.

The bargaining position of automakers has become more difficult due to the arrival of President Joe Biden who shared words of support at the picket line, explicitly backing the strike and their objective for 40% wage increases not-so-gradually over the next couple of years. The situation mirrors the strikes and wage negotiations that happened with railway workers. These fixed cost increases are a big problem for businesses that are now facing a disinflationary and cooling environment, and in the US automotive also continued competition that weakens pricing power to get ahead of these wage increases if they go through, which they are quite likely too.

There’s a big cost for the stoppages in production especially as demand broadly for automotive has yet to recover fully to pre-COVID levels, with the aftermath of the semiconductor shortages still taking their toll on the dynamics of the market. Taking advantage of the rebound is going to be an important factor in getting a full recovery, or at least to maintain market share with the risk of the pie shrinking as the leverage-based demand risks shrinking as rates come up.

The Japanese are excellently positioned to take share in the US from local US manufacturers. As we covered in Mazda (OTCPK:MZDAY), the weak Yen already has been an excellent reason for US consumers to choose Japanese cars over US cars, and for investors in Japanese automotive the FX effects create real value by promoting volumes of Japanese vehicles earning dollars abroad, while being able to keep paying expenses in Yen. While Honda has large factories in the US as well, so large that they actually export cars from the US at times, they also ship a lot of cars from Japan for the US market across the seas in RoRo ships. The whole Japanese automotive industry does this and benefit from this FX wedge, including Honda, which actually sells substantially more cars by value in the US than Japan or China, and is possibly the company with the highest proportion of sales coming from the US. The weakening Yuan on Chinese economic woes, where Japan acquires some parts for its cars as well, also contributes to a more pronounced price wedge when selling in the US.

The UAW strikes compromise the competitiveness of local automotive to get meaningful inventory into dealerships, while foreign carmakers, with Japan being one of the bigger ones with share in the US, able to put their products in front of customers who had been deferring car purchases these last couple of years.

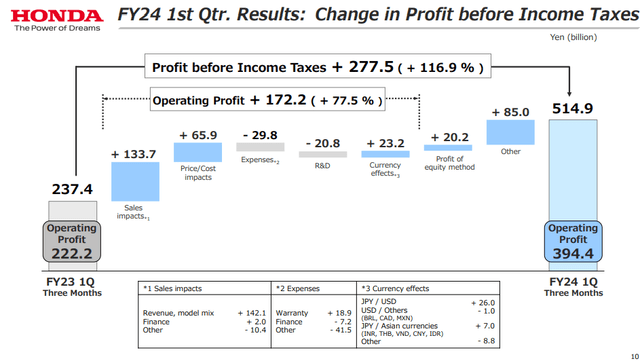

Choosing Honda

Honda is nice for several reasons. First, are the reasons outlined above which appear immediately in their result highlights, noting the sales and price/cost impacts in growing operating profits. Honda benefits more than most in this regard due to US and dollar exposure.

Profit Waterfall (Q1 2024 Pres)

The second reason we’re overweight Japanese automotive, with Honda being one of the most high profile picks, is because of the TSE requiring companies with P/Bs below 1x on the Prime Market on the TSE to report how they plan on bringing P/Bs up. Invariably, Japanese companies with low P/B are overcapitalized and have been accumulating too much cash due to insufficient payout ratios, for some reason pegged across industries at around 30%, even in the most mature industries. The loose credit environment in Japan, the cause of the weak Yen as rates remain negative in real terms there, make the overcapitalization even more extreme. Many companies haven’t made their plan public yet, but this is a requirement and all Prime Market companies including Honda will have received a memorandum about their P/Bs from the TSE, with the potential that a P/B clause may become part of ongoing listing requirements in the future.

To reduce P/Bs, the simplest solutions always are to increase shareholder payouts in the form of higher payout ratios and buybacks. A higher terminal dividend translates the high earnings yield from the low <10x PE multiple into a real cash yield for investors.

With the addition of the UAW strikes being a commercial opportunity for Japanese automakers, and a higher-for-longer rate environment being a support to the FX wedge provided by an enduringly weak Yen, we’d call Honda a buy with earnings growth as a catalyst and downside protection on potential changes in shareholder payouts.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here