Investment thesis

Mueller Industries (NYSE:MLI) is a high-quality traditional manufacturing business. I think so because the company delivered a massive profitability improvement over the past decade despite revenue growing at a modest pace. The company currently faces strong headwinds due to the decelerating pace of the broader economy’s growth, but profitability metrics are still strong and resilient. Moreover, the company’s balance sheet is a fortress and is strong enough to weather even long-lasting storms. Last but not least, the stock is very attractively valued and offers solid dividend growth. All in all, I assign the stock a “Buy” rating.

Company information

Mueller Industries, Inc. is a manufacturer of copper, brass, aluminum, and plastic products. The range of products manufactured includes copper tubes and fittings, steel nipples, aluminum and brass forgings, valves, and pressure vessels.

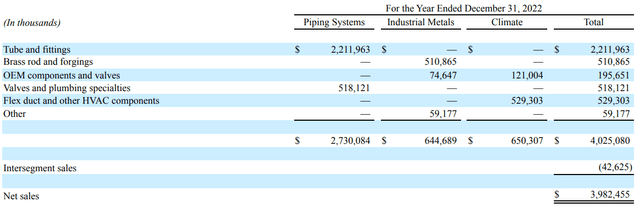

The company’s fiscal year ends on December 31. MLI’s business segments are Piping Systems, Industrial Metals, and Climate. According to the latest 10-K report, the Piping Systems segment contributes almost 70% of the company’s total sales.

MLI’s latest 10-K report

Financials

The company’s performance has been strong over the past decade. Although revenue growth was relatively modest, with a 7% CAGR, the company could expand its profitability metrics substantially. The operating margin widened from 6% to above 20% over the decade, which is impressive. As a result, the free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] reached stellar levels of 15% in the latest fiscal year.

Author’s calculations

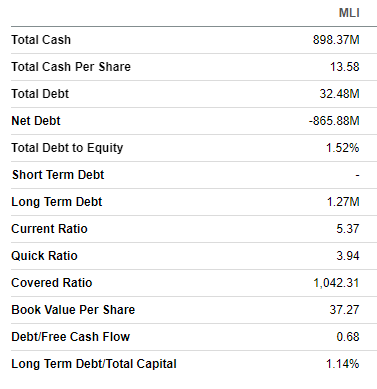

Consistently positive FCF margin enabled the company to build a fortress balance sheet with almost no leverage. MLI is in a substantial net cash position of $866 million, and the current liquidity metrics are in excellent shape. I like how the company balances driving growth, sustaining a healthy balance sheet, and keeping shareholders happy. The company has 18 consecutive years of dividend payouts and consistently conducts stock buybacks, which is a strong bullish sign for investors. Although the forward dividend yield does not look very attractive at 1.6%, the dividend growth rate was impressive over the last five years with a staggering 23.5% CAGR.

Seeking Alpha

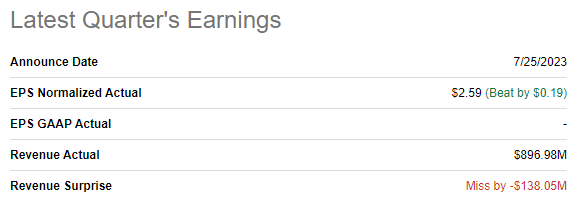

The current harsh macro environment of high interest rates and inflation weighs on the company’s financial performance. Increasing commodity prices also do not add optimism for manufacturing companies in the near term. MLI’s latest quarterly earnings were released on July 25, when the company missed consensus revenue estimates by a wide margin. Despite weakness in revenue, MLI topped consensus non-GAAP EPS expectations.

Seeking Alpha

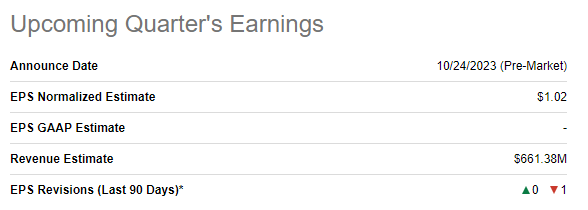

The challenging environment will continue pressing on the company’s financial performance soon. The upcoming quarter’s revenue is expected by consensus at $661 million, indicating a 30% YoY drop. The adjusted EPS is expected to shrink notably due to the top-line weakness, from $2.74 to $1.02.

Seeking Alpha

While some investors might consider the short-term dynamic in quarterly revenue as a catastrophe, I have an optimistic view. First, despite a massive revenue drop in the latest quarter, profitability metrics were still resilient. The operating margin shrank by over two percentage points, but is still above 20%. The company’s FCF is still positive, which is also a good sign. Second, MLI’s solid balance sheet enables the company to weather even a long-lasting storm. For long-term investors, it is essential to understand the nature of headwinds. In this case, challenges are temporary because they are caused mainly due to the macro environment, which is shifting between different stages of the economic cycle.

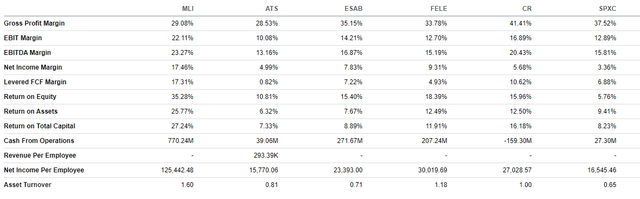

Any economic downturn will ultimately switch to the recovery and growth phases. Therefore, it is important to invest in high-quality businesses with wide profitability margins and strong balance sheets. And MLI is one of these businesses. Looking at the peer analysis of profitability metrics, we can see that Mueller Industrials is positioned well compared to the competition. To me as a potential investor, the bottom line and the FCF are the most crucial metrics, and MLI outperforms its peers by a wide margin. Stellar returns on capital and equity are also solid bullish signs for me.

Seeking Alpha

To conclude this part, I consider MLI as a fundamentally strong company that is worth investing in if the valuation is attractive.

Valuation

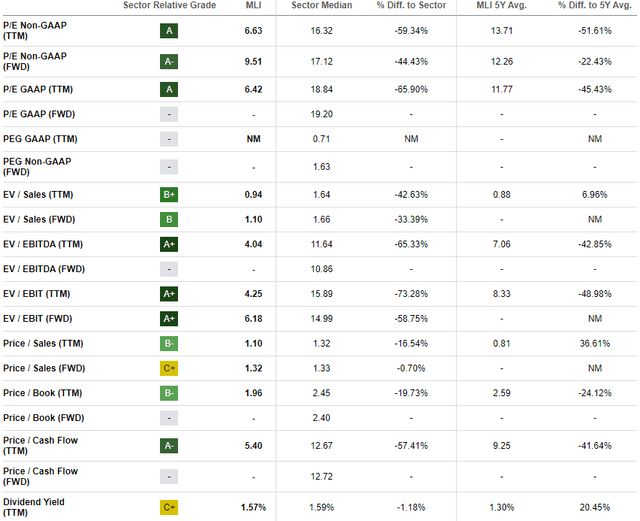

The stock rallied 29% year-to-date, substantially outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent “B+” valuation grade. Indeed, multiples look very attractive compared to the company’s historical averages and the sector median. That said, the stock is attractively valued from the valuation ratios perspective.

Seeking Alpha

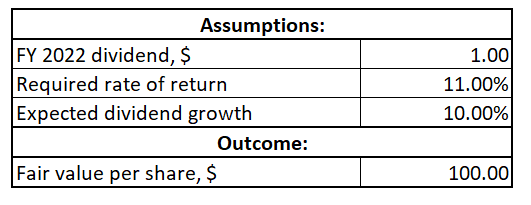

MLI pays its shareholders dividends. Therefore, a dividend discount model [DDM] approach looks like a sound choice to proceed with. I use an 11% WACC for discounting. Consensus dividend estimates are unavailable for MLI, so I use the latest available full-year dividend of 2022 as the current dividend. The company has a stellar dividend growth track record, so I think implementing a 10% CAGR would be conservative enough.

Author’s calculations

According to my calculations, the stock’s fair price is $100. This indicates a 32% upside potential, which is very attractive to me.

Risks to consider

Mueller Industries is substantially exposed to volatility in raw materials prices, especially copper, as a manufacturing company. Any adverse fluctuations in copper prices can undermine the company’s cost structure and profitability. The company is also susceptible to shifts in economic cycles. A slowdown in the macro environment will likely lead to reduced demand for MLI’s products, adversely affecting the company’s earnings.

Mueller Industries operates multiple manufacturing plants and facilities. Any disruptions in operations due to equipment failure or accidents might lead to downtime. This will ultimately adversely affect the company’s financial performance. The company’s operations also might be disrupted by its complex supply chain, which is vulnerable to geopolitical issues or natural disasters.

Bottom line

To conclude, the stock is a “Buy”. Despite substantial challenges the company faces in the current tough environment, its profitability metrics demonstrate solid resilience. Given the company’s consistently positive FCF margin and strong balance sheet, I think that the impressive dividend growth is safe even amid the current uncertain environment. If we put the current temporary headwinds aside, MLI is well-positioned compared to competitors since the company demonstrates stellar profitability metrics, which are higher than peers’ by a notable margin. Moreover, the valuation looks very attractive with more than a 30% upside potential.

Read the full article here