Introduction

The dividend yield for WhiteHorse Finance (NASDAQ:WHF) right now is very high at over 11%. This comes from the fact that the company aims to maximize the shareholder returns as it operates as a closed-end management business. The payout ratio is at 81% and the dividend has climbed quite a little over the years, but with 11% you are getting a fantastic return.

The share price seems to be in an uptrend right now as it bounced from the lows of $11.2 back in May when the financials sector saw a significant amount of volatility following the collapse of two significant regional banks. Besides this, WHF is trading below the NAV price of $14 which further illustrates why the price is so fair right now and deserves a buy rating in my opinion. Over the long term the high dividend yield is going to result in a significant market-beating return I think.

Company Structure

WHF is a business development company with a unique focus on originating senior secured loans in the lower middle market and growth capital industries. This non-diversified, closed-end management company specializes in providing financing to a range of sectors, including broad-line retail, office services, and supplies, building products, health care services, and health care supplies. By investing in these areas, WHF aims to support the growth and expansion of businesses in various industries while generating returns for its investors.

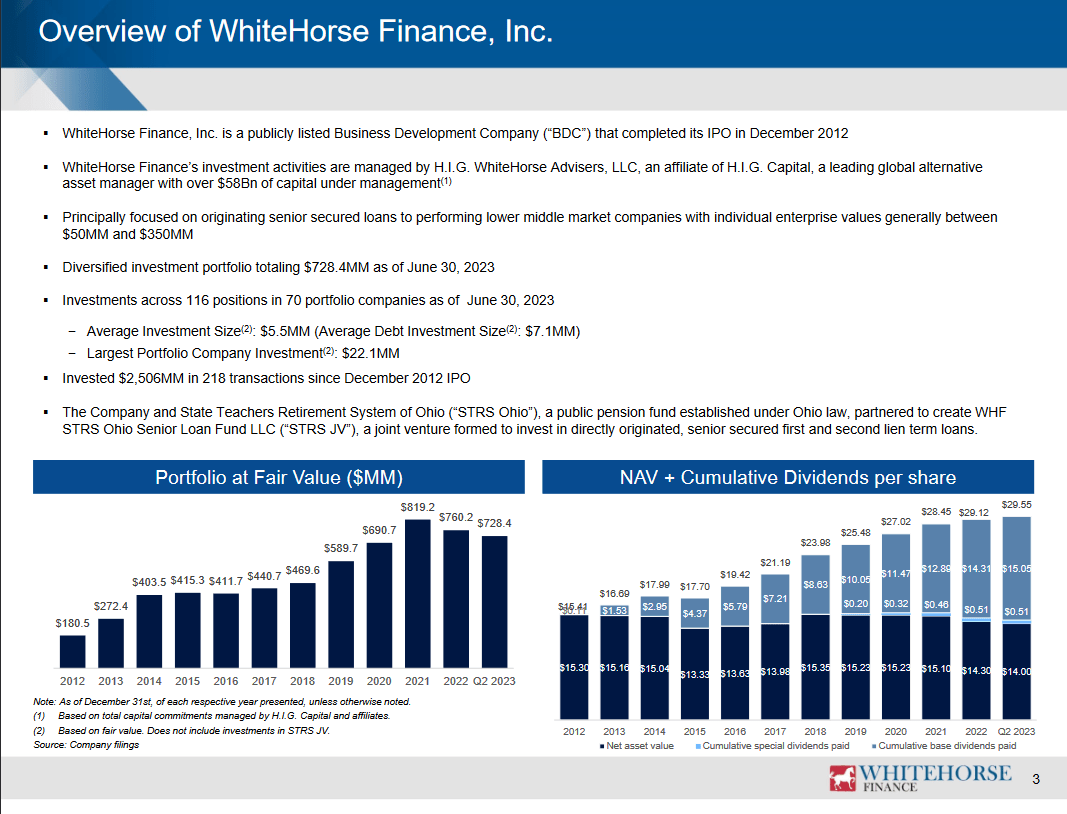

Company Overview (Investor Presentation)

Over the years the portfolio value of WHF has been steadily climbing and is several times higher than a decade ago. This has resulted in an asset growth of 8.28% annually in the last 10 years. If this is something that can be kept up I think that WHF looks quite undervalued right now even.

The company aims to generate a significant return based on its investments and then be able to pass that on to shareholders and therefore yield them a significant return as well. Since the IPO of the company, they have invested just over $2.5 billion in capital and have landed at an all-in yield of 13.4% which I find very impressive.

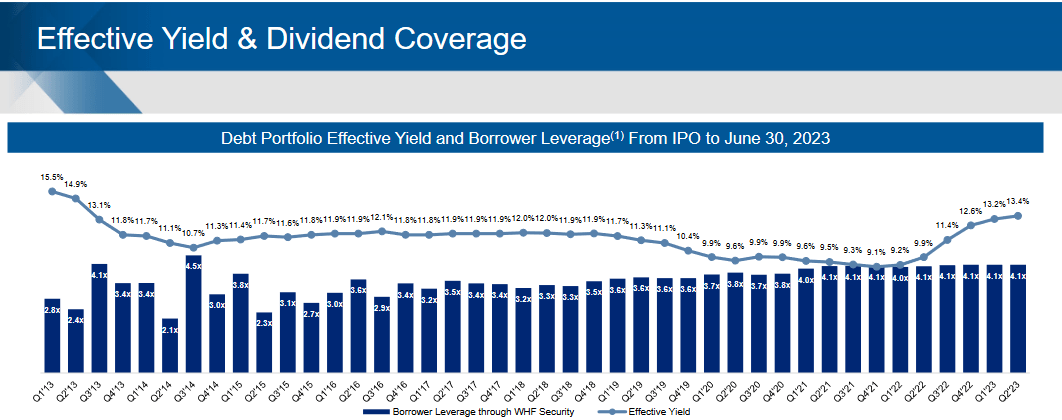

Company Yield (Investor Presentation)

Looking closer at the dividend yield of the company I think that WHF has done a great job here. The dividend yield has increased over the last couple of quarters as a result of higher borrower leverage. The leverage right now is at 4.1x but has sat quite stable at this level over the last few years. I think that WHF is in a position where it can afford to take on more leverage to drive stronger returns. I would prefer the verge ratio below 5 which still gives it plenty of safety to move around without making me worried.

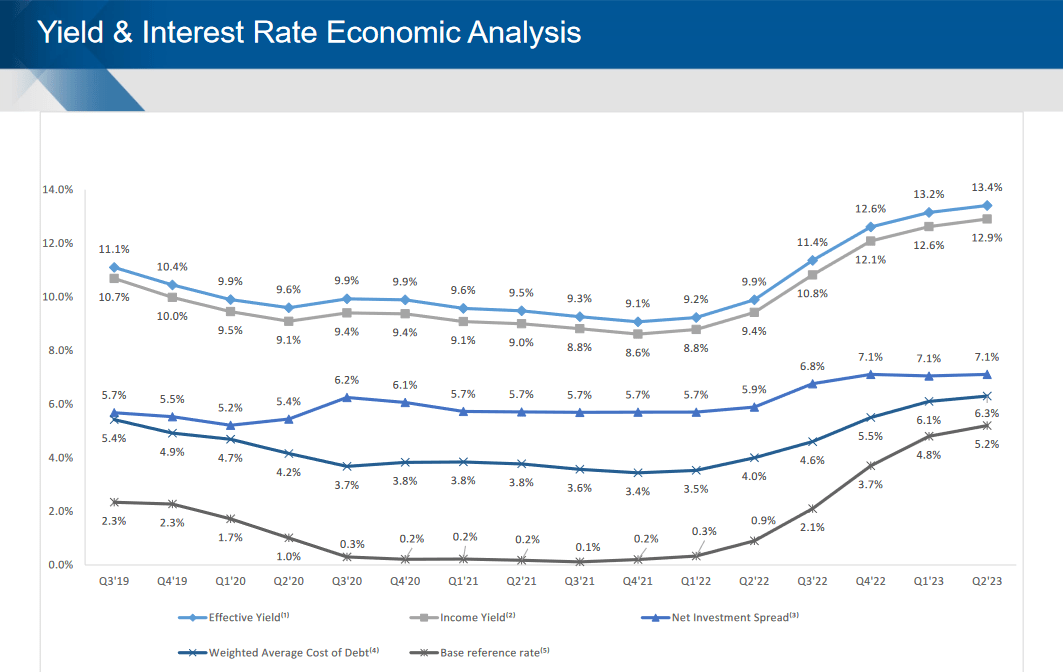

Yield And Interest (Investor Presentation)

Looking at the effective yield for WHF it follows quite well the base reference yield over the past several years. What I think is further impressive is the stable net investment spread the company has had over this time as well, as it hasn’t reached a point where I think it’s showcasing signs of weakness. If it dips significantly I would assume that the share price will do the same.

Earnings Transcript

Going off the last earnings call the company had on August 8, the CEO of WHF Stuart Aronson had some very interesting points and comments to share.

This morning I’m pleased to report strong performance for the second quarter of 2023, Q2 GAAP net investment income and core NII was $10.6 million, $45.06 per share, which more than covered our quarterly base dividend of $0.37 per share. While our core NII declined by $0.005 per share compared with Q1, Q2 core NII increased by 34.5% increase over – year-over-year”.

Seeing this strong growth in the NII of the business makes me very confident that the high dividend yield can be maintained from here on out. The core NII may have shown some decrease it still exhibited a significant double-digit YoY growth rate that I think has sent the share price up for the company. Going into the next couple of quarters I think that this is a key point to be watching in my opinion. If WHF can raise the NII even more then I see it likely that the share price accumulates quickly in value.

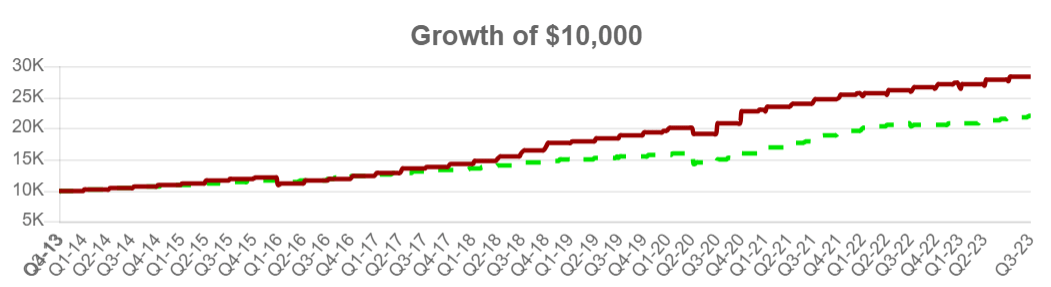

Company NAV (CEFData)

Looking above we can see that the NAV price of WHF has significantly managed to outgrow peers in the industry and this further underscores why I believe that WHF could be such a strong long-term addition. The price is under the NAV which is $14 per share.

Risk Associated

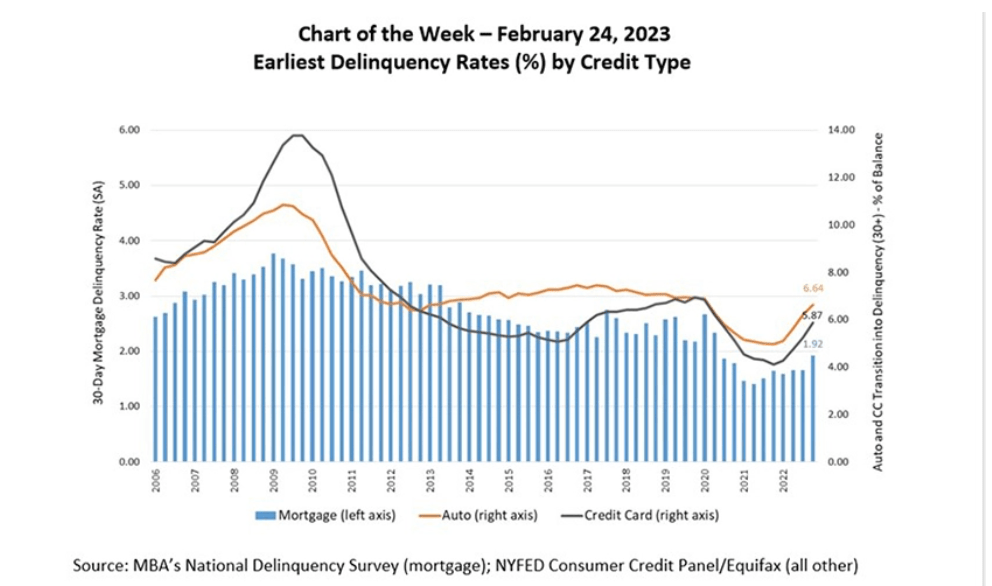

Given WHF’s involvement in providing loans, it’s essential to consider the impact of higher interest rates on the company. When interest rates rise, there is a potential risk that delinquency rates could start to increase as individuals and businesses face higher borrowing costs. If this trend becomes evident in one of the company’s earnings reports, it might put downward pressure on the share price as investors become more concerned about the heightened risks associated with the WHF loan portfolio.

Delinquency Rates (MBA)

In some remarks, it could be argued that WHF is overvalued right now as well. When looking at the p/s for example it sits at 2.8 on an FWD basis which exhibits a premium to the sector median of 27%. If there is a valuation metric to say that WHF is overvalued based on it would be this.

Besides this, I think there is a risk of prolonged interest rates that could mitigate some of the earnings potential of the company seeing as they are an asset and investment company and driving earnings from these sources is the reason for their high dividend yield right now. If they are forced to cut it I think the price would plummet as much of the appeal of WHF is the dividend yield.

Investor Takeaway

The appeal of WHF comes from the significant dividend yield it currently has and can provide investors with a very strong ROI over the long term. As seen in the picture above, the NAV of WHF has been climbing steadily over the years and exhibits why WHF is a sound addition. The earnings multiple sits below the rest of the sector and the last quarter presented a strong growth in the NII of the business. This is a trend I think can continue and underlines the buy thesis I have for WHF currently.

Read the full article here