My Thesis: Patience

Ferrari (NYSE:RACE) represents my ideal company to own. I am not referring solely to the car, which is the dream of many; rather, I am specifically interested in the company itself. There are only a few firms that have consistently outperformed their competition over such an extended period. In my estimation, aside from its engineering excellence, its true value stems from its robust brand, a topic we will delve into later. Its extensive history, sustained growth, and impressive returns on capital are the key metrics that resonate with me when evaluating a business.

However, and this is a significant point to consider, it’s worth noting that Mr. Market is fully aware of Ferrari’s worth and tends to price it as dearly as its luxury cars. Valuation becomes a nuanced challenge, and my current stance is to hold, I do not recommend selling; typically, I would allow my winners to continue their course. However, I do not currently hold the stock. I believe patience is in order, as we await a more favorable entry point. Opportunities will arise, and we must be prepared to seize them when they do.

Background

Founded in 1939 as Scuderia Ferrari by its legendary founder, Enzo Ferrari, this iconic company embodies the spirit of racing, as symbolized by the RACE ticker. In 1947, Ferrari expanded its horizons by venturing into automobile production, a move aimed at supporting its racing endeavors. This marked the inception of a unique symbiotic relationship between the race track and the commercial sale of vehicles.

Notably, Ferrari adopts a distinctive approach to marketing. Rather than direct advertising expenditure, the company leverages its racing team as a powerful promotional tool. By excelling (though not in recent years) in Formula 1 and various other motorsport competitions, Ferrari cultivated an extensive and passionate fan base. Despite this fervent following, the majority of enthusiasts remain unable to acquire the company’s flagship products. At motorsport events, Ferrari stands out with its iconic red livery and unwavering fan support. These factors contribute significantly to the brand’s global prominence, securing its place among the world’s premier luxury labels.

Strong Brand (Brand Finance)

Ferrari’s prancing horse emblem against a vibrant yellow backdrop has become a universally recognized symbol, propelling the brand into a lucrative merchandising venture that constitutes a substantial portion (almost 10%) of its revenue stream. The value of the Ferrari brand cannot be overstated; the company meticulously safeguards it. Notably, Ferrari has turned down potential buyers, even those with the financial means, in the past. Additionally, the company has taken legal action against customers who allegedly failed to uphold the brand’s prestige. These actions reinforce Ferrari’s position at the pinnacle of the luxury brand hierarchy.

Turning our attention to the business aspect, Ferrari maintains exclusivity and desirability by intentionally limiting vehicle production. This strategy effectively preserves both the price and prestige of their automobiles. Consequently, Ferrari boasts the most generous profit margins in the automotive industry, with a remarkable 24% operating margin and an astonishing 50% gross margin, an exceptional feat for an automaker.

Ferrari distinguishes itself further from the typical cyclicality of the automotive market. Unlike traditional automakers, Ferrari enjoys remarkable stability, including the stock market. This resilience can be attributed to the unique dynamics of the luxury sector, where demand remains relatively unaffected during economic downturns. The affluent demographic, particularly the super-wealthy, experiences less pronounced economic impacts, ensuring sustained demand and stability for Ferrari. In the current business landscape, where many companies are witnessing a deceleration in growth, Ferrari has demonstrated resilience with a commendable 14% uptick in top-line revenue and an impressive 35% growth at the EBIT line. This characteristic renders Ferrari a highly predictable company. Personally, I appreciate predictability, as it enables me to invest in the company at a higher yet still reasonable price without undue concern.

The Business By The Numbers

Ferrari categorizes its revenue into four distinct segments:

1. Cars and spare parts (84%)2. Sponsorship, commercial, and brand (9%)3. Engines (3%)4. Other (2%)

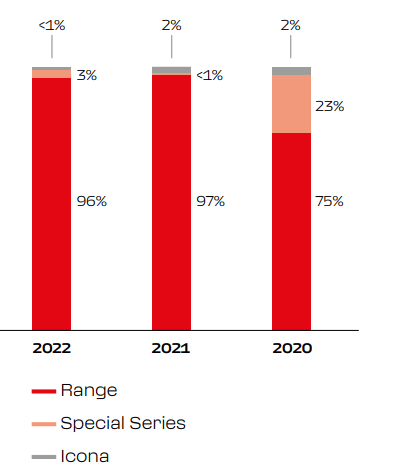

Within the majority share of its business, Ferrari classifies its cars into three primary categories: Range, Special Series, and Icona. In the year 2022, the Range category recorded the highest shipment volume, surpassing the other segments.

Cars Categories (Annual Report)

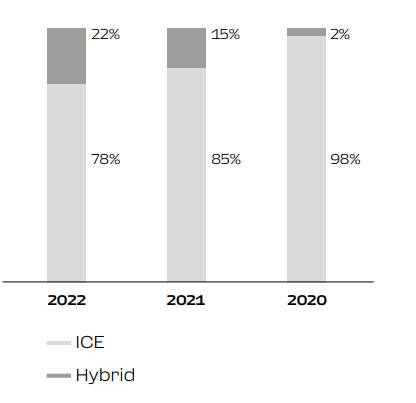

Within the Range segment, it’s noteworthy that hybrid cars are gaining market share. From my perspective, this development is significant as it offers insight into the potential sales of futuristic Electric Vehicles (EVs). It suggests that a portion of customers is inclined towards greener options, while there are likely others who strongly value the appealing engine sound that traditional cars offer:

hybrid growth (annual report)

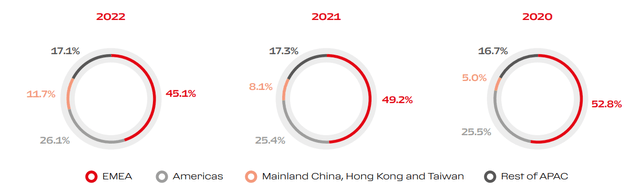

Ferrari also provides a breakdown of its shipment destinations, with notable growth observed in China (Even though, in the short term, the outlook for China may not be ideal)

shipment destinations (annual report)

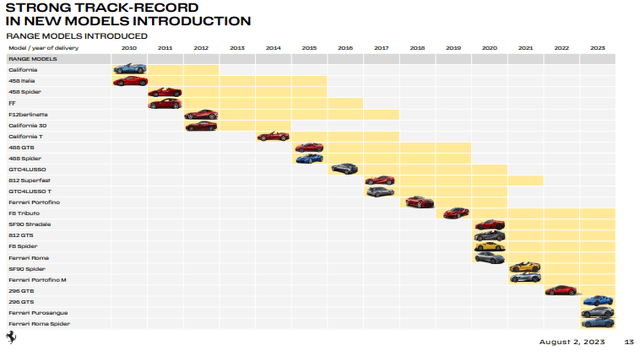

Ferrari’s growth relies on the maintenance of its brand value as well as excelling in innovation. As a testament to this commitment, the company allocates $875.6 million (TTM) towards R&D to foster superior engineering and design.

cars innovation (Q2 presentation)

The combination of brand value and innovation has translated into robust growth for Ferrari, even as a mature brand, with a 10% CAGR over the past 5 years and an impressive 18% CAGR over the past 3 years. As mentioned earlier, Ferrari has expanded its margins successfully by raising prices without adversely impacting demand. The EBIT line has exhibited significant growth, with an 11.7% CAGR over the past 5 years and a remarkable 27% CAGR in the last 3 years. In contrast to other firms, Ferrari is poised to continue growing, even in challenging economic environments, due to the unique characteristics I previously highlighted. If you’ve had the opportunity to peruse my previous articles, you’re likely aware of my keen interest in returns on capital. Ferrari impressively presents a Return on Capital Employed (ROCE) at 22% and a Return on Invested Capital (ROIC) at 19%. In my view, these ratios, coupled with the company’s robust growth, stand as market-beating indicators. Ferrari returns capital to its shareholders through share buybacks and also provides a modest dividend with a yield of 0.7%.

From a solvency perspective, in my opinion, the firm is well-established. Ferrari maintains $1.2 billion in cash and equivalents compared to $2.9 billion in debt. With an interest coverage ratio of 20 and a current ratio of 2.12, which is considered solvent in the short term, Ferrari exhibits strong financial stability. Furthermore, Ferrari boasts an Altman Z-Score of 10, which is undeniably excellent. Additionally, I believe Ferrari is one of the few firms that can be relied upon to continue generating substantial revenue streams.

I Won’t Purchase the Stock at Current Prices

As is consistently emphasized in my articles, the attainment of quality necessitates a corresponding financial commitment. However, this commitment need not be excessively burdensome, for an excessively elevated price can transform an otherwise promising investment in a reputable company into an unfavorable one. Ferrari presently finds itself in a rather precarious situation. I shall commence my analysis with a relative valuation approach, wherein I favor comparisons against the company’s historical averages. Comparing Ferrari to other firms, particularly within this industry, appears to be a daunting task for me.

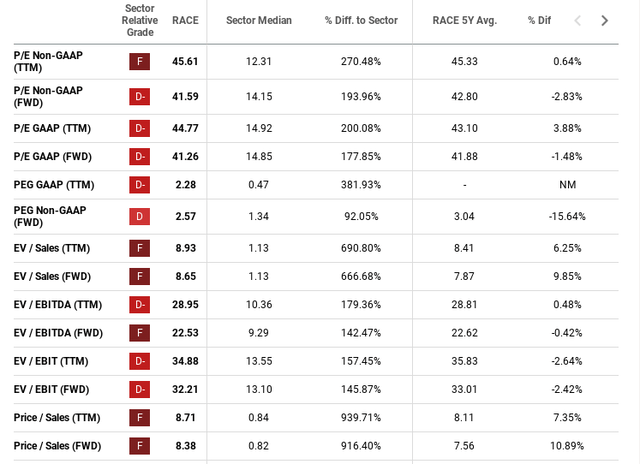

As of now, the valuation of RACE stock appears to be in line with its historical multiples averages. In general, my inclination leans toward acquiring companies when their valuation multiples significantly deviate from their historical averages, this is not due to fundamental underperformance, much like my recent investment in ASML, as detailed in my previous article. Unfortunately, Ferrari’s valuation multiples are significantly distant from the levels I typically consider suitable for investment. From this particular standpoint alone, I would refrain from approaching it, and this is without even factoring in the substantial overvaluation that becomes apparent when examining my DCF calculations.

multiples (Seeking Alpha)

From a discounted cash flow perspective, exercising caution in formulating assumptions is imperative. Nevertheless, in the case of a firm like Ferrari, I can reasonably anticipate a sustained growth rate of approximately 10% (Drawing upon historical growth patterns and analysts’ projections), primarily due to the robust demand and profitability it enjoys. While I cannot assert this with absolute certainty, it is somewhat immaterial given the current pricing dynamics. Optimistic assumptions, even if made, appear insufficient to enhance the stock’s attractiveness.

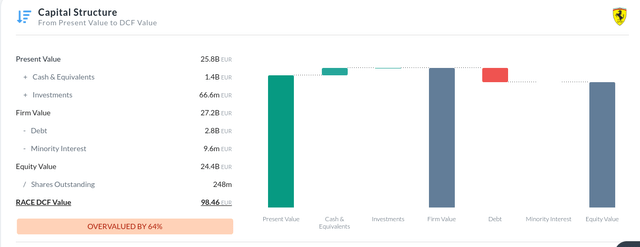

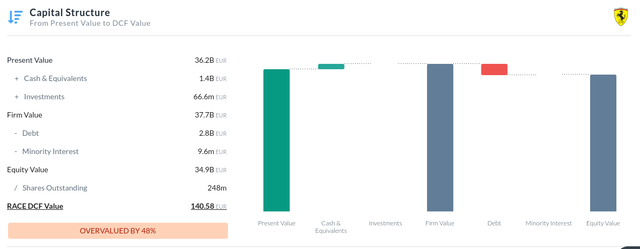

To construct my DCF model, I have employed the historical top-line growth rate of 10%, assumed a 26% EBIT margin, and employed a tax rate of 20% based on the latest financial report. The model spans a 5-year horizon, with a terminal growth rate of 3% and a discount rate of 9% derived from the WACC calculation. The resulting chart indicates a target price of approximately $98, implying an overvaluation of the company by more than 60% (!). It is worth noting that the growth rate for the past three years stood at a commendable 18%, but as a company expands, relying on such growth becomes increasingly challenging, albeit not entirely implausible. Under the 18% growth scenario, the price would be projected at around $140. Nonetheless, even under this more optimistic scenario, the stock does not appear to warrant a purchase based on the DCF model.

DCF result (Alpha Spread) DCF result #2 (Alpha Spread)

In the case of Ferrari, I favor the application of relative valuation, as the DCF method may not adequately capture the company’s inherent quality. For instance, earlier this year, the stock was trading below its historical valuation multiples, yet I refrained from purchasing it, and the stock has since appreciated by 50%. In my view, certain companies are seldom conducive to acquisition through the DCF approach.

While I am not a technical analyst myself, I do possess some knowledge in this area and utilize it in an attempt to make purchases at opportune moments. I prefer to buy stocks when their price is near their 200-day average and their RSI is low. However, neither of these indicators is currently met in the case of Ferrari.

technical view (tradingview)

As I contemplate all three valuation approaches that I typically employ in my company research, I discern the qualities of a truly exceptional company. However, its current valuation appears to be unreasonably elevated. If I were holding the stock, I would opt not to sell it, perhaps considering only a partial reduction in my position. Yet, I would not contemplate purchasing it at its present price point. I have experienced unfortunate encounters in the past with high-quality companies for which I developed a deep appreciation, only to acquire them at inflated prices, subsequently encountering the capriciousness of Mr. Market. I endeavor to draw lessons from such experiences and avoid repeating those regrettable mistakes. Over time, I have come to realize that the most valuable tool for investing in the world’s highest-quality companies is patience. Without it, there is a risk of acquiring these exceptional assets at unattractive prices, and I strongly advise against making such a choice.

Risks

Ferrari must embrace innovation and excel in the production of electric vehicles (EVs) as they have with their internal combustion counterparts.

While a severe economic downturn could potentially impact the company, I believe it might not affect Ferrari as severely as it would others.

Subpar performance on the racing track, in my view, has the potential to diminish the brand’s value.

Valuation in the case of Ferrari is indeed a complex matter; it consistently commands a premium, yet it may not always present a viable investment opportunity. At present, in my perspective, it presents an opportunity to inflict distress upon investors.

Conclusion

My dream company is currently beyond my immediate reach.

Its qualitative attributes align precisely with my criteria for an ideal company; however, Mr. Market is acutely aware of its allure. It is intriguing to observe the unfolding dynamics of hybrid integration and the forthcoming electric vehicles (EVs). The confluence of brand prestige, innovation, and engineering excellence has fostered a formidable and unwavering demand, seemingly impervious to disruption for the esteemed Italian establishment.

However, at this moment, I am unable to include it in my portfolio. It must remain on my quality watchlist. As students of history, we must exercise patience and wait for this gem to RACE towards us. It will happen, and I assure you that I will provide updates.

I’d love to hear what you think about this company.

Read the full article here