It’s been nearly 2 months since I announced to the world that I’m still avoiding Norfolk Southern Corporation (NYSE:NSC), and in that time, the shares are down about 13.4% against a loss of about 4.6% for the S&P 500 (SP500). That’s gratifying to some degree, but it’s time to review the name yet again because the shares are now even more cheap than they were last April when I bought the shares. For that reason, it’s time to review the business again. I’m going to review the latest traffic patterns we have available to us, and compare these to the current valuation to see if it makes sense to buy back in or not.

I’m the sort of reader who likes to read the final page of a novel to see how things work out because I don’t like surprises. I assume the same of my readers on this forum. You didn’t come here for me to hit you with an expectation-subverting plot twist at the end of my article. You want to know what I’m thinking upfront. This is why I write a “thesis statement” at the beginning of each of my articles. It gives you more than you normally get from a title and bullet points, but much less than you get from the entire article. As importantly, it lets you know what you’re getting at the outset.

In spite of the fact that traffic continues to decline, I’m going to be buying back into Norfolk Southern this morning. This is because the valuation has become attractive to me once again. I am of the view that stocks should be eschewed when they’re too expensive, and they should be embraced when they’re sufficiently cheap, and, in my view, this stock is now sufficiently cheap to buy. As I wrote earlier, I think the dividend is reasonably well covered, and I think there’s room for growth on that front over the next decade. For that reason, I’m comfortable buying in spite of the fact that the yield is about 200 basis points lower than the 10-year Treasury Note (US10Y).

Traffic Review

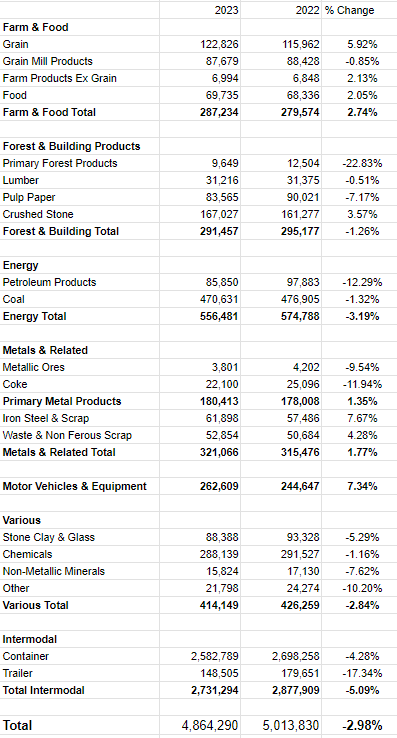

In case you’ve forgotten, I’ll remind you that Norfolk Southern is a railroad, and as a result they make their money hauling stuff. They specialize in hauling bulky, heavy items with low per unit value. We see from the table below that so far this year, the company has hauled about 3% less “stuff” this year than they did last year. Most interestingly to me, “forest and building materials” and “energy” were down, sometimes dramatically from last year. This may offer insights into what’s going on with the broader economy, including construction, and the various energy sectors.

In any event, in order for me to buy back into the name, I’d need to see the valuation reflect this slowdown, lower current price or not.

Norfolk Southern Traffic to Week 35 (Norfolk Southern investor relations)

The Stock

If you read me regularly for some reason, you know that I consider the stock and the business to be two different things. For instance, the business generates revenue by hauling really heavy stuff. The stock, meanwhile, is a slip of virtual paper that gets traded around in the public markets. This stock represents a claim on the future revenues and profitability of the business, and one reason that the stock bounces around so much in price is because people change their minds frequently about that future profitability. In the short term, though, the stock’s price movements are more volatile than most changes in the underlying business.

For instance, if someone bought Norfolk Southern on July 28 (the day after they reported their latest earnings), they’re down about 19% on their investment. If they bought virtually identical shares nearly two months later after Transportation Secretary Buttigieg announced $1.4 billion in funding, they’d be down only about 5.9%. Either way, not enough happened from July 28 to now to account for a near 20% reduction in the value of this stock. So, we may “buy businesses” in an abstract way, but in reality we access the cash flows of that business via the very capricious stock.

In my experience, this volatility is frustrating, but it’s the only source of sustainable profits when it comes to buying and selling stocks. Specifically, I’m of the view that the only way to make money trading stocks is to work out the assumptions that are currently embedded in price, and trade against those assumptions when they are unreasonably optimistic or pessimistic. Paying attention to what’s known by most other investors at the present is relatively useless as current news is already “priced in.”

Additionally, I think it’s worth noting that buying cheap stocks tends to lead to higher returns. In the example above, the person who bought when the shares were cheaper had a “less bad” return. Not only are cheap stocks lower risk because they have far less to drop in price, they also offer greater potential reward, because it’s easier for the companies of these stocks to outperform low expectations.

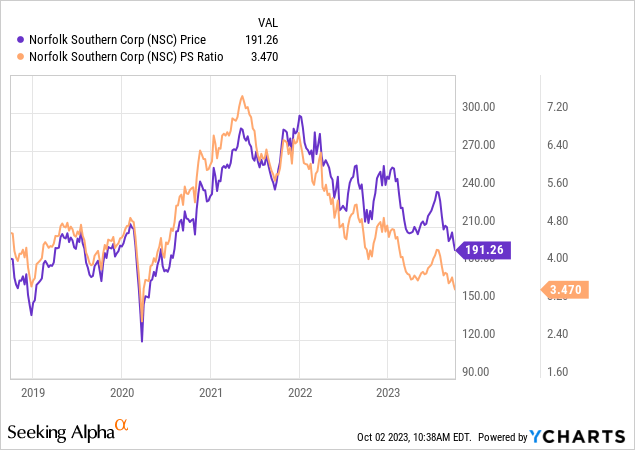

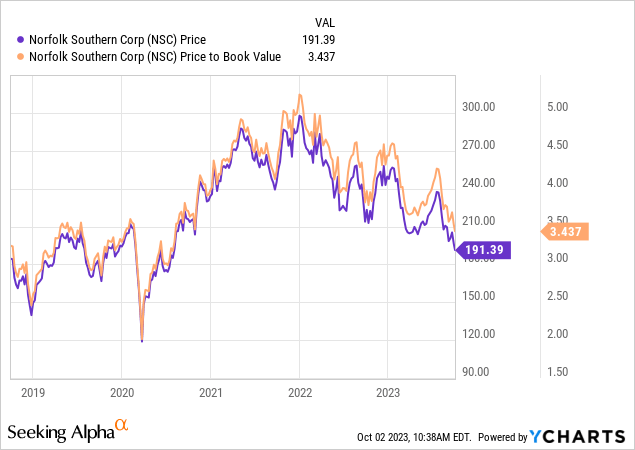

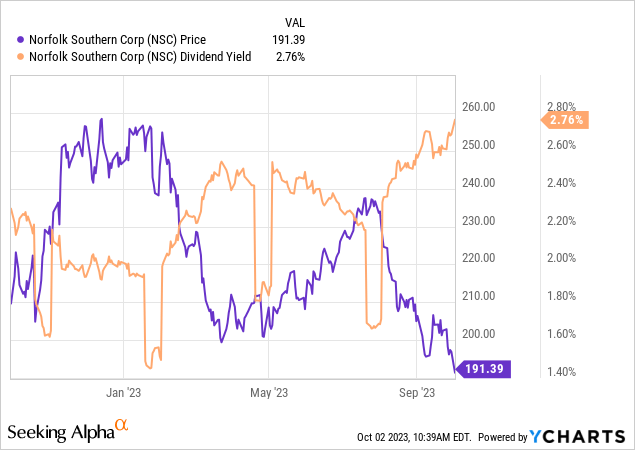

My regulars know that I measure “cheap” in a few ways, ranging from the simple to the more complex. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, and the like. I bought Norfolk Southern in April when the stock was trading at a price-to-sales ratio of about 3.74 times, a price-to-book value of 3.62 times, and sported a dividend yield of 2.5%.

Fast-forward to the present, and things look even more attractive today. The shares are between 5% and 7.2% cheaper than they were when I last bought, and the dividend yield is higher by about 10% higher. I’ll admit that the yield is still nearly 200 basis points below that of the 10-year Treasury Note, but I think there’s some room for dividend growth over the next decade.

You may recall that I wrote that the only way to make money in stocks in my estimation is to spot discrepancies between expectations and subsequent reality. That means, then, that we need to work out what the assumptions are currently. Again, I want to buy when the crowd’s expectations are too dour and sell when the crowd becomes too rosy. Additionally, I want to try to quantify these expectations as much as possible, and to do that, I turn to the works of Stephen Penman and/or Mauboussin and Rappaport.

The former wrote a great book called “Accounting for Value” and the latter pair recently updated their classic “Expectations Investing.” All of these writers consider the stock price itself to be a great source of information, and the former in particular helps investors with some arithmetic necessary to work out what the market is currently “thinking” about the future of a given business. This involves a bit of high school algebra, where the “g” (growth) variable is isolated in a standard finance formula. Applying this approach to Norfolk Southern at the moment suggests the market is assuming that earnings will grow at a rate of about 4% from current levels. Although this is slightly optimistic, it’s not egregiously so. Given that Norfolk Southern Corporation shares are otherwise inexpensive, I’m comfortable buying back into this business with its wonderful “moat.”

Read the full article here