Thesis

In a time characterized by both technological innovation and economic uncertainty, Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) stands as a pivotal player at the crossroads of opportunity and challenge. This article delves into TSMC’s intricate position in the semiconductor industry, its financial performance amidst market fluctuations, and, notably, the results of an analysis that underscores its substantial upside potential with a DCF model projecting a present fair value of $124.9, signifying a 43.8% upside from the current stock price, and a potential 121.2% future upside over five years.

After a thorough analysis of the short-term prospects, it is evident that while the stock does possess substantial long-term potential, it might encounter a decline in its stock price in the immediate future. This decline can be attributed to the ongoing downturn in consumer electronics demand resulting from the prevailing economic challenges. Given these circumstances, my recommendation is to assign TSMC a “Hold” rating.

Overview

Business

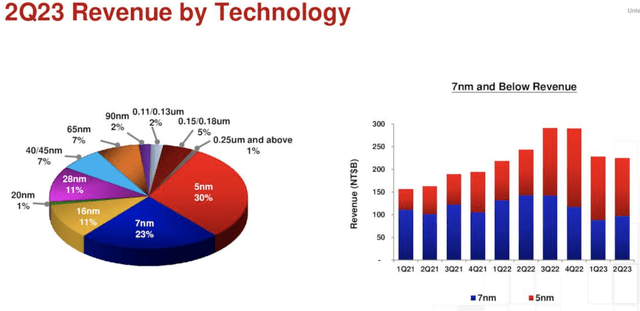

As evident from the graph below, TSMC heavily relies on 7nm and 5nm chips, which collectively account for over 53% of its revenue. Both the 7nm and 5nm technologies find extensive use in consumer electronics. For example, the Apple (AAPL) A12 utilized 7nm technology, while Apple’s A14 employed 5nm technology. The primary distinction between them lies in their processing speed, with 5nm outperforming 7nm. This is due to the fact that the lower the nanometer value, the shorter the distance electrons must travel. Consequently, this leads to enhanced efficiency, reduced heat generation, and faster performance.

However, it is worth noting that investors need not delve into the intricacies of semiconductor technology. Rather, their focus should primarily be on understanding the factors that can impact the demand for these chips, as this knowledge informs the company’s valuation.

Q2 Investors’ Presentation TSMC

What happened in Q2 2023?

When TSMC released its Q2 earnings on July 20, the company experienced a decline in second-quarter revenue and provided a gloomy outlook, which included the postponement of the Arizona plant’s construction from 2024 to 2025.

Furthermore, TSMC currently faces capacity constraints, which are likely to result in reduced operating margins.

What’s up with the plant?

The plant has become a battleground for conflicts involving TSMC, labor unions, and the firms managing the project. TSMC has been accused of disregarding labor safety guidelines and failing to address the concerns raised by the unions.

Additionally, TSMC has asserted that there is an insufficient number of qualified workers in the US, leading them to apply for 500 work permits for Taiwanese professionals. This move has encountered opposition from the unions.

Finally, TSMC has faced accusations of providing inadequate plans. According to construction workers, TSMC has not supplied detailed blueprints but rather basic engineering drawings. Moreover, they have implemented significant changes, which, according to the construction workers, often involve dismantling existing structures to comply with the new guidelines.

The positive aspect of this situation is that it primarily revolves around a coordination issue, which can be resolved without substantial investments. However, the downside is that if this problem persists, the original cost of the plant could escalate.

Running at low-capacity

In Q4 2022, the first signs of trouble emerged, with the most severe impact felt by the 7nm chips, which operated at an 83% utilization rate. Subsequently, in Q1, this rate dropped to below 70%, and in Q2, it dipped below 60%. This predicament is attributed to weakened demand for smartphones and PCs.

N16 chips also suffered a decline, falling below 90% utilization in Q1 and remaining at 75% in Q2. N5 chips are similarly affected, with a utilization rate of approximately 88%. The challenge with utilization rates lies in the fact that operating costs remain fixed while revenue can fluctuate, akin to the dynamics of oil drilling.

Moreover, advanced packaging is essential for new AI chips, and Nvidia (NVDA) is the largest customer in this regard, particularly for their A100 and H100 GPUs.

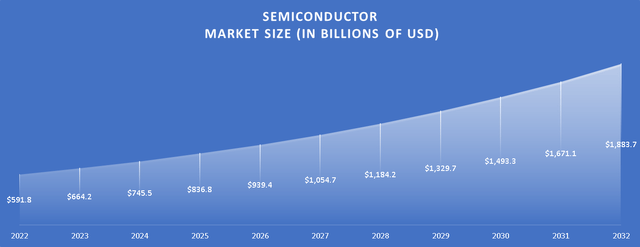

Projections suggest that the semiconductor market is poised to grow at a Compound Annual Growth Rate [CAGR] of 12.28% from 2023 to 2032. As of 2023, the market size stands at approximately $664.2 billion. If these projections materialize, it is estimated that the market will expand to $1.88 trillion by 2032.

Author’s Calculations

Can AI chips move the needle?

To counter the near-term downturn in mobile phones and PCs, the contracts for AI GPUs, expected to grow at a rate of 34.7% between 2023 and 2026, may prove to be the saving grace. Further forecasting beyond this timeframe may not be necessary given the two-year horizon.

For the Nvidia H100, which measures 812 mm² and utilizes a 300 mm wafer ( which has a surface of around 28,274 mm²) with 4nm technology, it can be estimated that one wafer can produce 27 H100 chips. TSMC charges between $18,000 and $20,000 per wafer, translating to an approximate production cost of $703 per H100.

With these estimates in mind, we can project that TSMC could generate $1.09 billion in revenue for 2023, equating to approximately $272.5 million per quarter, from manufacturing H100 chips for Nvidia. This calculation is simplified but serves as a rough estimate. It is based on my expectations, as discussed in my article about Nvidia Corporation, which suggests estimates lower than those put forth by analysts.

However, if I take analyst’s expectations as a base, which basically means that Nvidia will earn about $33.1 billion in data center revenue for FY 2024 (2023), divided by the cost $30,000, it would mean that Nvidia sold 1.7 million GPUs, which means $1.74 billion for TSMC, $306.17 million quarterly.

Now, one might argue that I’ve only considered Nvidia, but what about the other players? Well, it’s important to note that TSMC holds a commanding grip on approximately 90% of the production of these AI chips. Looking ahead to 2023, it’s projected that the revenue generated from AI chips, essential for artificial intelligence applications, will soar to an estimated $53.4 billion. When we divide this figure by the average cost of $20,000 per chip, it equates to a staggering 2.6 million chips sold. When we multiply this number by the estimated revenue of $703 per chip, it translates into a substantial $1.8 billion in revenue for TSMC.

In essence, these figures are substantial enough to potentially offset the anticipated declines in the mobile and PC sectors, in the case they amount to $2.8 billion. However, it’s essential to acknowledge that any further downturn beyond this point could pose significant challenges. Currently, with a year-over-year revenue reduction of 2.9%, equivalent to $2.1 billion, we find ourselves perilously close to breaching that threshold.

Financials

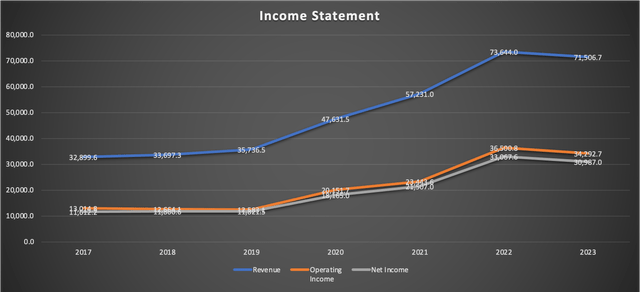

TSMC revenue currently stands at $71.5 billion which represents a YoY decline of 2.9%. This is not that severe and is way better than having a decline of 13-20%.

Author’s Calculations

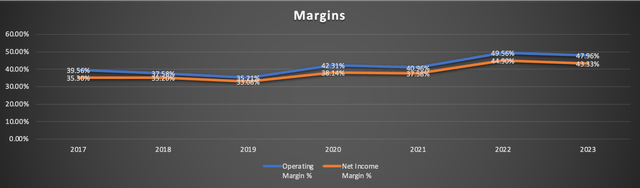

Since Q2, we have observed a slight decrease in margins, primarily attributed to the low utilization situation. Prior to Q2, the operating margin and net income margin stood at 48.32% and 44.15%, respectively. However, as we approach Q3, these margins have moderated to 47.96% and 43.33%.

Author’s Calculations

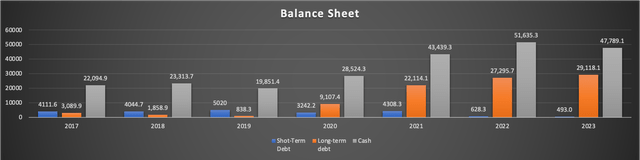

The company’s balance sheet remains robust, boasting substantial cash reserves sufficient to eliminate its entire debt. Nevertheless, there has been an increase in long-term debt of approximately $2 billion from Q1 to Q2 of 2023, while the substantial cash reserves have remained stagnant over the same period.

Author’s Calculations

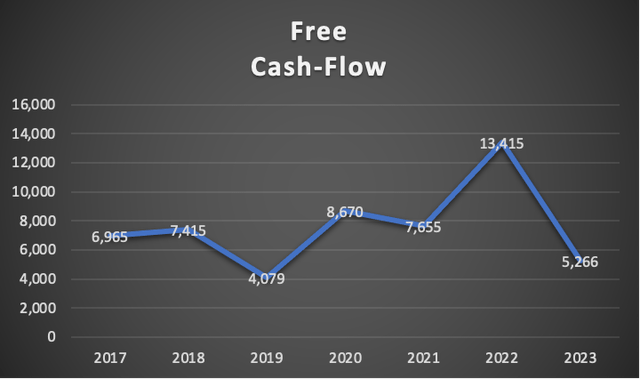

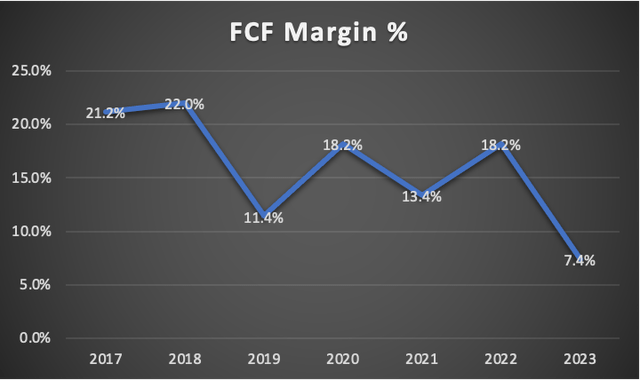

Now, let’s delve into one of the most significantly impacted metrics – free cash flow. Before Q2, it amounted to $11.6 billion, but it has since contracted to $5.2 billion. This reduction in free cash flow translates to a decline in the FCF margin, falling from 15.68% prior to Q2 to the current margin of 7.4%. This represents more than a fifty-percent reduction.

Author’s Calculations Author’s Calculations Author’s Calculations

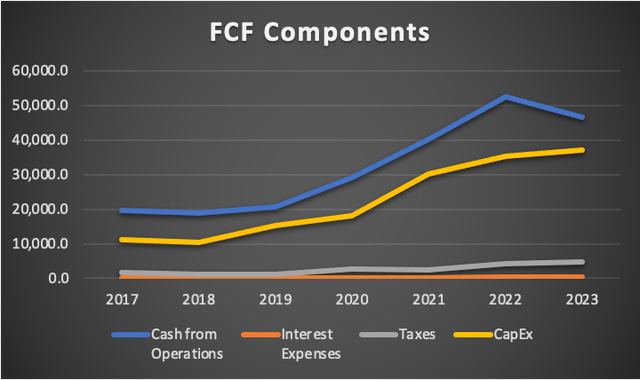

Overall, there haven’t been many substantial changes from Q1 to Q2 2023, apart from the noted margin adjustments. These reductions in margins can be attributed to the worsening utilization rates that TSMC has encountered as the year has progressed.

Valuation

First and foremost, it’s important to acknowledge that any revenue downturn for TSMC should have been anticipated in a market characterized by high interest rates and dwindling savings. As I’ve previously mentioned, over 40% of TSMC’s revenue is closely tied to consumer electronics, such as smartphones and PCs, which can experience significant cyclical fluctuations.

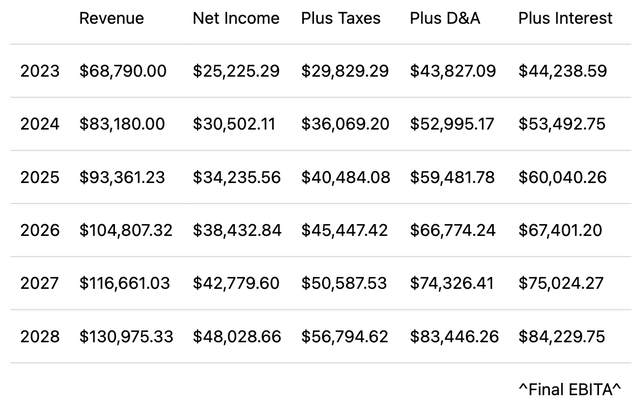

In a previous article, I provided revenue projections for 2023 and 2024 that were considerably lower than the consensus estimates put forth by analysts. The variance amounted to nearly $3 billion for 2023 and a substantial $5 billion for 2024.

Previous Estimates (Author’s Calculations)

| Revenue | Net Income | Plus Taxes | Plus D&A | Plus Interest | |

| 2023 | $65,040.0 | $23,804.64 | $26,908.93 | $39,701.63 | $40,071.55 |

| 2024 | $78,860.0 | $28,862.76 | $32,626.66 | $45,419.36 | $45,789.29 |

| 2025 | $93,361.2 | $34,170.21 | $38,626.24 | $56,989.44 | $57,520.44 |

| 2026 | $104,807.3 | $38,359.48 | $43,361.81 | $63,976.34 | $64,572.45 |

| 2027 | $116,661.0 | $42,697.94 | $48,266.03 | $71,212.07 | $71,875.59 |

| 2028 | $130,975.3 | $47,936.97 | $54,188.27 | $79,949.78 | $80,694.72 |

| ^Final EBITA^ |

| D&A Projection | Interest Projection | |

| 2023 | 12,792.704 | 369.92 |

| 2024 | 12,792.704 | 369.92 |

| 2025 | 18,363.201 | 531.00 |

| 2026 | 20,614.530 | 596.11 |

| 2027 | 22,946.033 | 663.53 |

| 2028 | 25,761.510 | 744.94 |

Author’s Calculations

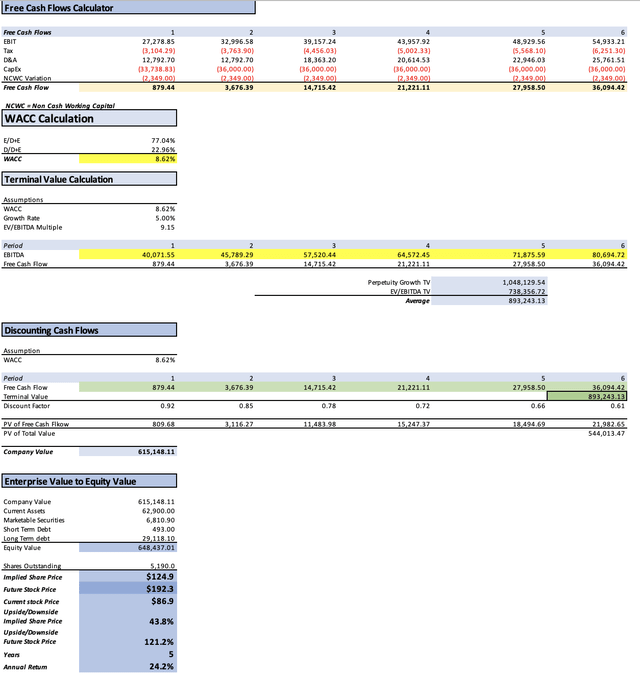

Now, turning to the Discounted Cash Flow [DCF] analysis, it reveals a present fair value of $124.9. This represents an impressive 43.8% upside from the current stock price of $86.90. Additionally, the projected future stock price of $192.3 implies a remarkable upside of 121.2%. Over a five-year period, this suggests an annual return of 24.2%.

It’s worth noting that the present fair price doesn’t fluctuate significantly in this context. The primary factor influencing stock prices here is the growth rate. As demonstrated in this model, and as indicated in my previous analysis, I am assuming a long-term growth rate of 5%. However, if we were to consider a higher growth rate of 7%, the landscape changes dramatically. The present fair value surges to $203.7, and the future value soars to $321.5.

I assign a “hold” rating to TSMC, as previously elaborated, due to the likelihood that AI demand may not suffice to offset the decline in consumer electronics demand. Some may wonder why I’m recommending a “hold” when my DCF analysis suggests significant undervaluation. The reason is that if I had conducted a DCF for just a three-year horizon, the price would appear lower. It’s important to note that many analysts set their price targets within a span of 12 to 18 months, a timeframe where trends are more firmly established, as opposed to projecting over a five-year period.

Risks to Thesis

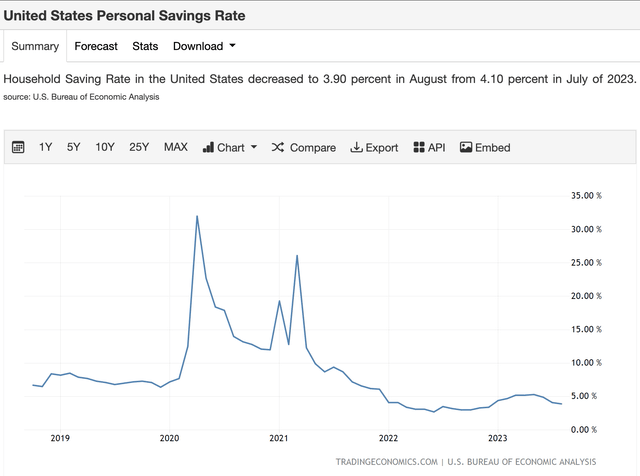

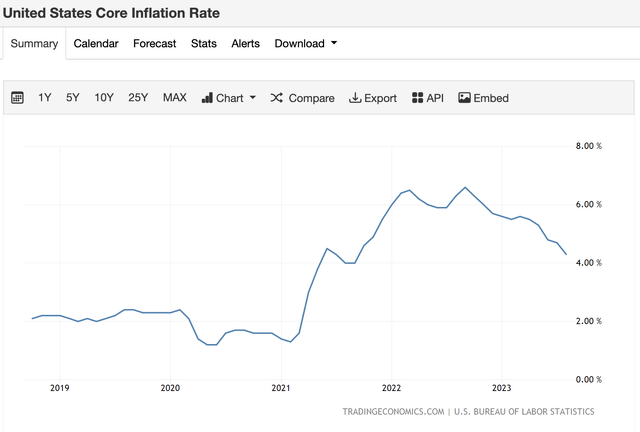

As I’ve mentioned previously, it’s essential to set realistic expectations for TSMC in the short term. Phone sales and PC sales are anticipated to either decline or remain flat, particularly in a period characterized by restrictive monetary policies. It’s unsurprising that people may lack the purchasing power to invest in high-end devices, whether it’s the latest iPhone 15 Pro Max with 1TB of storage or even a $600 laptop. This factor alone should serve as a clear indication that the road ahead may be challenging.

Trading Economics

Trading Economics

Furthermore, I don’t foresee Intel (INTC) or Samsung being able to usurp TSMC’s leading position. As previously discussed in my earlier article, TSMC’s very existence emerged from the need to separate chip production from chip design. Companies like Intel, which were integrated device manufacturers [IMD] involved in both production and design, posed a risk to chip designers as there was a potential for their designs to be pilfered by the IMDs. Additionally, the constant equipment rotation required in IMDs made it more profitable to specialize in chip design rather than both production and design.

Given these factors, TSMC’s unique positioning and expertise in semiconductor manufacturing are likely to help it maintain its competitive edge in the industry. While short-term challenges may persist, the long-term prospects for TSMC appear promising,

While I understand that this article may seem contradictory, please don’t misunderstand me; I have a positive outlook on TSMC’s prospects. However, I believe that in the near term, a more favorable buying opportunity may arise. Nevertheless, there’s nothing wrong with those who prefer to make immediate purchases rather than waiting in my opinion.

Conclusion

In conclusion, TSMC stands at the intersection of technological innovation and economic fluctuations. Its dependence on 7nm and 5nm chip technologies, which power consumer electronics like smartphones and PCs, has made it both a beneficiary and a victim of market dynamics. The intricacies of semiconductor technology aside, investors should focus on the external forces that shape chip demand and, consequently, TSMC’s valuation.

TSMC’s recent financial performance has seen some fluctuations, notably in its margins and free cash flow, largely influenced by lower utilization rates stemming from the global economic climate. The company maintains a strong balance sheet with ample cash reserves. Nevertheless, a DCF analysis suggests substantial upside potential for TSMC’s stock price. The DCF model yields a present fair value of $124.9, signifying a 43.8% upside from the current stock price of $86.90. Furthermore, the projected future stock price of $192.3 implies a large potential upside of 121.2%, translating to an annual return of 24.2% over five years – but near-term challenges loom, particularly due to economic conditions affecting consumer electronics sales.

Nonetheless, I anticipate that TSMC will offer a more favorable entry point in the near term. Consumer electronics demand may further decline as economic conditions worsen, and as savings deplete. It’s also crucial to note that student debt repayments are set to resume, which will exacerbate the financial condition of the American consumer. For these reasons, I have decided to assign a “hold” rating.

Read the full article here