Investment action

Based on my current outlook and analysis of Intuit (NASDAQ:INTU), I recommend a hold rating. While I acknowledge that INTU is a big and stable business that has consistently compounded FCF over the years, I believe it is still under the mercy of near-term macro movements. In particular, the current macro weakness significantly impacts INTU’s primary base of customers—small businesses and consumers. While there are initiatives that would likely drive long-term growth, I think the time to invest is when all these macro issues are behind us.

Basic Information

INTU is a famous brand for anyone who does their own tax, small businesses, and accountants. There are 5 key products that INTU offers to its customers: Turbotax, CreditKarma, Mint, Quickbooks, and Mailchimp. The business has been around for a long time, and through organic and M&As, it has reached a massive size of $14 billion in annual revenue in FY23. INTU is also a cash-generating beast, as it has maintained an FCF margin of 20 to 30+% over the past 10 years and compounded FCF at more than 15% over the past 10 years.

Review

Based on what I learned from reviewing INTU 2023 Investor Day last week, the company’s future looks bleak for the foreseeable future. Management’s long-term revenue growth target of 15 to 20% was restated during the presentation, which was encouraging given that growth has been well below that range in recent quarters. My negative viewpoint is that Intuit, which grew 13% in FY23 and is expected to grow 11% at the midpoint in FY24, would need to significantly speed up its growth rate in order to meet these targets.

Unfortunately, this trend appears to be here to stay for the foreseeable future, and I attribute much of it to the persistently difficult macro environment. I interpreted management’s openness to sharing information about the macroeconomy as a signal that the economy will remain weak in the near future. To my mind, management’s observation that small businesses have 90% less cash on hand this year compared to this time last year indicates that liquidity is becoming an increasingly pressing issue in the macro environment. As a result, spending money on riskier expansion projects or anything else deemed unnecessary will be put off as long as possible. The statistics (mentioned by management) showing a decline of 13 points in small businesses’ credit scores and an increase of 30 percentage points in their average credit card balances corroborate my assessment of the current macro situation. In addition, as student loan payments resume and interest rates remain higher than in recent years, pressure is increasing on consumers’ discretionary income. I’d also point out that the delinquency rates for credit cards and mortgages are both on the rise. Clearly, we are nowhere near the end of this pain.

But this is not the end of the road for INTU. Although I am pessimistic about the near future because of the sluggish macro situation, I think investors were heartened to see management actively pursue incremental growth opportunities. For instance, if well implemented, management’s decision to expand Quickbooks’ reach into the SMB mid-market (10 to 100 employees) should prove to be a significant growth driver. There is no dearth of product features, so I believe the odds of success are high if a solid go-to-market strategy is implemented. INTU is ramping up its efforts to increase its market share in the mid-market by strengthening its marketing strategy and expanding its sales team. If this upmarket shift is successful, INTU will have more experience figuring out how to expand into the market for companies with more than 100 employees (most likely between 100 and 250). The end goal is probably increasing market share in the enterprise sector, but I don’t think that will happen anytime soon. However, the fact that INTU has been able to successfully break into increasingly larger markets gives investors reason to believe they can achieve their ultimate goal of breaking into the enterprise market, which could be a stock valuation re-rating catalyst.

Now, let’s move to the $52 billion mid-market opportunity. We’re building product and go-to-market engines to deliver end-to-end platform of connected scalable solutions with QBO Advanced at its core. There’s so much runway within our base. There are 800,000 mid-market customers already using one of our core QuickBooks queues. And we continue to see meaningful growth in our high-value customer base. INTU 2023 investor day

Valuation

Author’s work

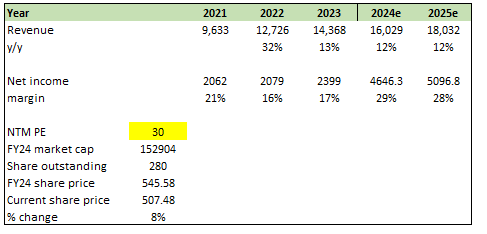

Being conservative, I am assuming that growth rates stays at the current low-teens region, implying that INTU will not be meeting management’s target for high-teens growth. Under this assumption and applying INTU historical average forward PE – which I think is fair as the business is growing in line with historical low-teens rate, my price target is $545, or 8% above where the stock price is today ($507).

Risk and final thoughts

My primary concern is that recent economic and geopolitical events have caused widespread uncertainty and harmed businesses, causing some IT customers to become more picky in their purchasing decisions, delay modernization projects, and cut back on spending. Customers’ IT spending and, by extension, demand for INTU’s products and services, could be negatively impacted if the economic climate continues to deteriorate, especially given the company’s exposure to SMB.

My recommendation for INTU is a hold rating. INTU is a substantial and stable business with a strong track record of generating free cash flow over the years. However, it remains vulnerable to near-term macroeconomic conditions, which have a significant impact on its primary customer base, including small businesses and consumers. While there are promising long-term growth initiatives, I believe it may be prudent to wait until the macroeconomic challenges subside before considering an investment.

Read the full article here