This is my first look at Alector, Inc. (NASDAQ:ALEC) an intriguing clinical stage biotech. Like hundreds of its peers it has no product income, with none in sight for the next few years. What it lacks in product income and breadth of portfolio it is working to make up with productive big pharma collaborations.

During its three year span as a public company Alector has had its highs and lows, trending down

Starting out as an LLC in 2013, Alector restructured as a corporation in 2017. On 02/03/2020 it announced the closing of its underwritten public offering of 9,602,500 shares of its common stock at the public offering price of $25.00 per share. Initial IPO enthusiasm carried its shares up to a closing high of $35.08 on 02/07/2020.

They wobbled up and down for several months until 07/29/2020 when they dropped decisively to a close at $16.31 on disappointing trial data. Before long it closed <$10 on 10/15/2020 after missing quarterly numbers for Q1, Q2, and Q3 2020.

Despite its travails and a lack of positive news, shares regained their heft closing out the year >$15.00. News reports on its Alzheimer’s therapy candidate buoyed the stock in early 2021. It bounced around in the high teens and low $20’s until it stunned the market with its 07/02/2021 GSK (GSK) deal.

That day it hit an intraday high of $43.32 and then closed at $35.21 on a furious trading day with >39 million Alector shares changing hands. The furor was short-lived. By the end of 07/2021 Alector had notched several closing prices of <$25.00. It has since to reach another closing >$30.00.

It has bounced around, trending downward. It last closed above $10.00 on 09/08/2022. As I write on 10/03/2023 it closed at $6.26.

Big pharma deals have played a major role in Alector’s value proposition

General

Alector’s S-1 filed in 01/2019 in connection with its IPO made it clear that collaborations played a key role in Alector’s development plans. It introduced itself as an early clinical-stage biopharmaceutical company with a limited operating history.

Since its formation in 2013 it had focused on developing therapeutics for neurodegenerative diseases. These included frontotemporal dementia [FTD], Alzheimer’s disease [AD], and Parkinson’s disease [PD]. Its sole revenues came from grants and collaborations.

Alector’s AbbVie (ABBV) deal

Alector’s initial stab at a big pharma collaboration took form in October 2017. Alector entered into a Co-Development and Option Agreement with AbbVie (AbbVie Agreement). As stated in Alector’s S-1 the primary goal of the AbbVie Agreement was to co-develop and commercialize therapeutics to treat Alzheimer’s and other neurodegenerative diseases.

The release announcing the deal described the parties’ respective roles as:

AbbVie and Alector have agreed to research a portfolio of antibody targets and AbbVie has an option to global development and commercial rights to two targets. Alector will conduct exploratory research, drug discovery and development for lead programs up to the conclusion of the proof of concept (PoC) studies. Upon exercise of the option, AbbVie will lead development and commercialization activities. Alector and AbbVie will co-fund development and commercialization and will share global profits equally. Alector will receive a $205 million upfront payment and a potential, future equity investment of up to $20 million.

The parties settled on AL002 and AL003, two therapies focused on treatment of AD. In an 07/08/2022 press release Alector announced that after a program review AbbVie was no longer partnering to develop AL003. It noted that the deal continued with respect to AL002, also an experimental treatment targeted at AD with a different mechanism of action.

Alector has but a meager pipeline of clinical assets. AL002 is its second lead asset. As described in slide 7 of its 08/2023 corporate overview slide presentation (the “Presentation”), it expects a phase 2 AL002 data readout in Q4, 2024.

In its 2023 10K (p. 4) it noted that AL002 targets Triggering Receptor Expressed on Myeloid cells 2 (TREM2). I discuss this aspect of the AbbVie deal in more detail below. Later in the 10-K (p. 20) it noted that it expected top-line data from its AL002 longterm extension study in Q4, 2024.

In Alector’s Q2, 2023 10-Q (p.15) it notes that the AbbVie Agreement calls for possible additional payments:

… regulatory milestone payments, an opt-in payment for continued development of AL002, and other future payments from profit sharing or royalties after commercialization of product candidates from such program.

Alector’s GSK deal

As mentioned above Alector’s stock shot up in 07/2021 when it announced its GSK corroboration. The financial elements of the deal were particularly notable They provided Alector $700 million in upfront payments, up to $1.5 billion in potential milestones, profit sharing and royalties.

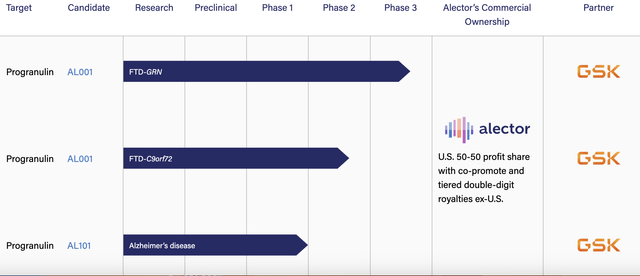

In return Alector provided GSK the right to co-develop progranulin-elevating monoclonal antibodies, AL001 and AL101. It envisions therapies for a range of neurodegenerative diseases, including FTD, PD, and AD. At the time of the deal, Alector had advanced the following:

- AL001 — enrollment in a pivotal Phase 3 trial in people at risk for or with frontotemporal dementia due to a progranulin gene mutation (FTD-GRN);

- AL001 — currently in a Phase 2 study in symptomatic FTD patients with a mutation in the C9orf72 gene;

- AL001 — planned to enter Phase 2 development for amyotrophic lateral sclerosis (ALS) in the second half of 2021;

- AL101 — a Phase 1a clinical trial designed to treat patients with AD and PD.

The following excerpt from Alector’s pipeline entry on its website (accessed 10/01/2023) lists its GSK trials as:

alector.com

It includes no entry for ALS. Alector’s phase 2 trial (NCT05053035) to evaluate AL001 in C9orf72-Associated ALS is shown “TERMINATED” on clinicaltrials.gov.

Alector’s website does include the following general discussion:

Researchers have come to understand that ALS and FTD are part of a broad neurodegenerative continuum…. Decreased progranulin levels are associated with the abnormal accumulation of the TAR DNA-binding protein 43 (TDP-43). Excess aggregation of TDP-43 is thought to lead to neuronal death. We are developing AL001, …, for ALS based on evidence that increasing progranulin levels may be protective, and even reverse, TDP-43 pathology.

Its Presentation slide 5 includes the following catchall, “Undisclosed programs in AD, PD, FTD, ALS, vascular dementia and BBB technologies”. I interpret the sum of this as dropping to ALS to back burner status.

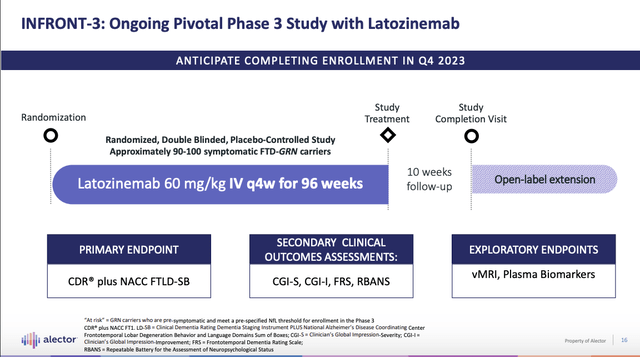

Presentation slide 16 below describes Alector’s lead therapy latozinemab, AL001.

alector.com

Its pivotal Latozinemab INFRONT-3 trial is scheduled to complete its enrollment by the close of Q4, 2023. It will take 96+ weeks to gather the data once the last patient has completed the trial. In response to a question during the Call CMO Romano pegged the data release as:

…we’re going to finish enrollment in the fourth quarter of this year, 96 weeks later, or that would be approximately third quarter of ’25 we will have last patient out and data shortly thereafter.

Data by Q3, 2025 strikes me as optimistic. I submit that Q1, 2026 is more likely. I note that there has already been considerable slippage compared to 05/04/2023 release hypothesizing data in “early 2025 with the potential for a … filing in late 2025 subject to regulatory discussion outcomes”.

Alector’s finances rely on hefty collaboration revenues

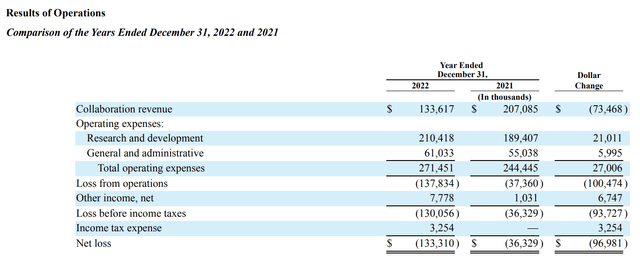

Alector’s comparison of results for the years ended December 31, 2022 and 2021 as set out in its 2023 10-K shows the importance of its collaboration revenues:

seekingalpha.com

The variation in revenues was complicated by recognition of revenues from its GSK and AbbVie deals. The excess in 2021 reflects $173.4 million collaboration revenue recognized from the latozinemab FTD-GRN license provided as part of the GSK deal. This was partially made up in 2022 by recognition of $55.8 million net increase to collaboration revenue under the AbbVie Agreement resulting from the termination of the AL003 program.

It is unclear how this will play out in future years. Alector’s Q2, 2023 10-Q shows collaboration revenues of $72,763 for the first 6 months of 2023 compared to $104,325 for the first 6 months of 2022. During the Call, CFO Grasso guides for total 2023 collaboration revenues of between $90 million and $100 million. The trend seems to point down with guided 2023 collaboration revenues less than half those of 2021.

In terms of expenses Grasso guided for 2023 R&D expenses between $210 million and $220 million; he guided general and administrative expenses to be between $60 million and $65 million. The guidance pegs aggregate expenses to a midpoint of $277.5 million only a slight increase over 2022’s ~$271.5 million.

Alector’s 2023 10-K (p. 24) includes sections titled:

- Strategic Alliance with GSK (p. 24); and

- Strategic Alliance with AbbVie (pps. 24-25).

Each of these includes sections for overview, governance, exclusivity, intellectual property and term and termination. As regards to future collaboration revenues the GSK agreement tantalizes with its $1.5 billion in potential milestones beyond the $500 million received in 2021 and the $200 million received in 2022.

The triggers for the additional GSK milestones and the timing and amount of future recognition of milestones already received are unclear. They could be considerable over the next few years.

The AbbVie deal likewise confounds and entices with hefty potential and uncertain time lines. It provides for $250 million payment if AbbVie exercises its option to Alector’s TREM2 program. It also includes potential for $225 million in milestones “related to the regulatory approval for up to three indications”.

CFO Grasso tallied Alector’s cash at $630 million at close of Q2, 2023. He pegged this as sufficient to take it through 2025. This should take it out to AbbVie’s $250 million TREM2 decision point.

Conclusion

Alector’s current market cap of ~$540 million is hovering right below its cash balance. The market seems to take a dim view of its prospects for turning this cash into profitable revenues.

Its success or failure is heavily dependent on continuing to qualify for milestones under its collaborations. The qualification requirements and timing for future milestones are unknown. We do know that management is guiding for less in 2023 than for its two previous years as stated above.

Expenses are taking significant chunks from its cash resources as time moves on. Management expects its $630 million to pave a cash runway from close of Q2, 2023 through 2025. As 2026 rolls in it will need to ramp up its revenue production.

Whether it will be able to do so is a known unknown which creates a question mark that leads me to stand back. Accordingly I rate Alector a hold.

Read the full article here