Thesis

I am a big fan of family-owned holding companies, as they often have excellent long-term track records because they take a long-term view and stay away from risk, as they manage the money of the entire family. Companies like Investor AB (OTCPK:IVSXF), which has returned 15% a year over the past 35 years, or Tamburi, Exor (OTCPK:EXXRF) and LVMH (OTCPK:LVMHF) have all easily beaten the S&P 500 over the past 10 years or more.

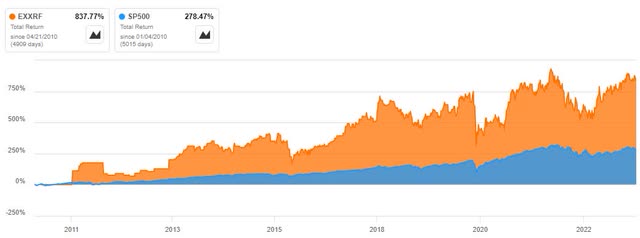

Seeking Alpha Charting Tab

Exor’s performance over this period has been nothing short of phenomenal, demonstrating the capital allocation skills of the family and its management team. The Agnelli family, and John Elkann in particular, have created value for themselves and for shareholders. And their portfolio and asset allocation should enable them to continue this success.

Let me explain in the next few chapters why I think they have a strong case for 15%+ annual returns over the next 10+ years, which should be your time horizon if you plan to invest alongside the Agnellis.

Exor’s Business And Portfolio

Exor Investor Presentation

Exor’s portfolio is divided into private and public investments as well as early stage investments through Exor Ventures. Also Royal Philips (PHG), in which Exor acquired a 15% stake for 4 billion euros, was added to the 3 large public companies Ferrari (RACE), Stellantis (STLA) and CNH Industrial (CNHI).

The portfolio focuses on luxury, technology and healthcare, which management believes are the most interesting sectors for the future. In the luxury sector, they have the No. 1 luxury car brand, Ferrari, which has such a strong brand that it is in a league of its own. And Christian Louboutin, with its red bottoms, is clearly the No. 1 in high-priced high heels. So these are two very strong brands that have a huge competitive advantage. The first all-electric Ferrari, which will debut in 2025, is likely to boost their sales even more. They also own Shang Xia, a Chinese luxury brand that is relatively unknown to most, but is in the most important growth market in the luxury industry. China, and probably India in a few years, will have a huge impact on the sales of luxury brands.

Exor Investor Presentation

In Healthcare, with the Philips acquisition, they have a company that is transitioning to be more of a healthcare company, which fits with Exor’s plan for how they want to deploy capital. To what extent it is a good fit and how it will evolve will only be known in a few years. But in Merieux they have one of the leading companies in clinical diagnostics for infectious diseases and in Lifenet Healthcare they have a company that manages hospitals and outpatient clinics. As the population ages and people live longer, healthcare is likely to be one of the most lucrative sectors in the future. The compound annual growth rate (CAGR) for the digital health market is projected to be 23.7% through 2030. At Exor Ventures, where they have invested approximately $500 million in more than 75 companies, they also focus primarily on healthcare, fintech, and mobility.

Stellantis, the successor to Fiat, the legacy company of the Agnelli family, has a strong portfolio of different brands in the automotive industry and is the third largest player by sales. In FY22, they managed to increase net sales by 18%. However, due to the cyclical nature of the company, I would not invest in it alone. But the high cash flow of Stellantis can and will be used by Exor to fund other projects with a better ROI. To have enough money for better projects, Stellantis with its ~7% dividend yield is a good addition.

Juventus, one of the most iconic clubs in European soccer, is more of a trophy asset, although a sale would likely fetch a lot of money. However, it would probably not match the sales of the Premier League clubs as they have a much stronger television deal.

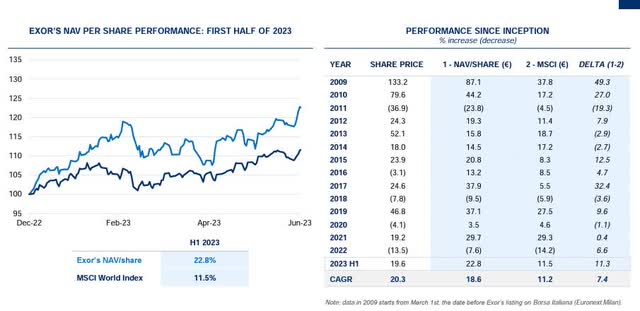

Exor Shareholder Presentation

Since its listing on March 1, 2009, Exor has a nice visualization of its NAV per share compared to the MSCI World. Although it should be noted that the company almost always trades at a discount to its NAV. It should also be noted that the years 2009 and 2010, when they massively outperformed the MSCI in terms of stock CAGR, slightly distorted the long-term CAGR.

Current NAV of Exor

- Stellantis: 14.4% = 14.4% x $57b = ~$8b

- Faurecia: 5.1% = 5.1% x $5.1b = ~$260m

- Ferrari: 24.2% = 24.2% of $53b = ~$12.8b

- CNH: 26.9% = 26.9% of $15b = ~$4b

- Iveco: 27.1% = 27.1% of $2.1B = ~$550m

- Juventus: 63.8% = 63.8% of $800m = ~$500m

- Philips: 15% = 15% of $18.5b = ~$2.7b

Market Cap Exor: $19.3b Public Investments: ~$29b

And the public investment is about 75-80% of Exor, so you get a total NAV of about $35 billion to $37 billion. So the discount to NAV is probably somewhere between 40% and 50%. A little discount for holding companies is normal because of the holding discount, but it’s more like 10% to 20% most of the time. That said, Exor is definitely undervalued.

EXXRF’s Capital Allocation

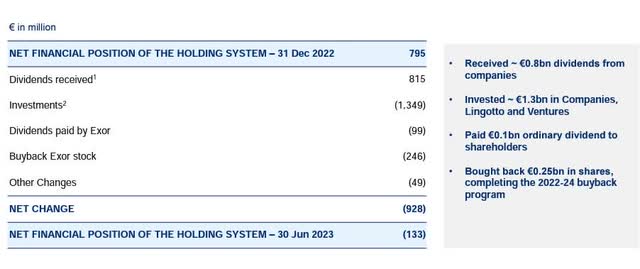

Exor H1 Investor Presentation

Exor’s management believes that share buybacks are more efficient for most shareholders, which is why they have set the annual dividend at €100 million and prefer to use buybacks to return cash to shareholders. Between 2018 and 2020, they bought back €300 million worth of shares, representing about 2.28% of the issued share capital.

This was followed by the €500 million program, which started in 2022 and was completed with the third and final tranche in June 2023. In total, 1.5 million + 3.5 million + 1.9 million = 6.9 million shares were repurchased.

Now they have announced a new program where they want to buy back €1 billion in shares, which is about 12% of the free float and 5% of the market cap. 750 million of this offer is in the form of a tender offer in which Agnelli BV has already agreed to participate for 250 million euros. They made the tender offer because they hoped it would be faster than if they were to make on-market purchases. The tender offer expires on October 12, 2023. If the amount of €750 million is not reached, this will be a vote of confidence in the company by the selected shareholders.

With the shares trading at a massive undervaluation to NAV, this is exactly the right time to buy back shares and should benefit shareholders enormously in the long run. In addition, the €400 million investment in Lingotto and the €60 million investment in Ventures, as well as the €833 million investment in Merieux to support growth, should be good capital spending for the future.

With about €1.5 billion in annual dividends from its companies, cash flow for further investment appears secure. Overall, the company has demonstrated that it understands how to create value for shareholders. The spin-offs of Ferrari or Ivesco, combined with the merger of Fiat and Peugeot, show that they can allocate capital resources efficiently. After all, when you invest in a company like Exor, you are really investing in the capital allocation skills of the management, because that is what drives long-term returns.

Risks

You have to understand that a lot of money came in from the sale of PartnerRe, and normally Exor is dependent on the Stellantis dividend. So if Stellantis, which is a cyclical company, has to cut its dividend, Exor has less to work with.

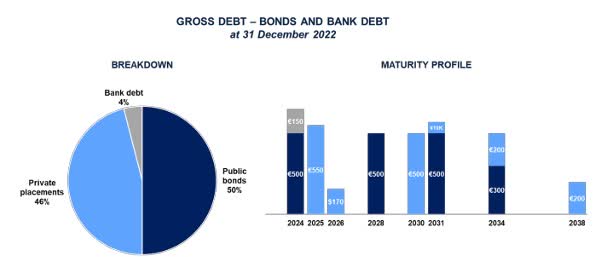

Exor Investor Presentation

However, it should be noted that they also used some of the money from the sale to reduce debt by about €0.6 billion, bringing gross debt down to €4.2 billion. While 95% of that is in bonds with an average maturity of 7 years and only 2.5% average fixed costs. So the cost of capital is not overwhelming.

Conclusion

Given the large discount to NAV, I think it is likely that they can increase the share price by 80% over the next 4 years to close some of this gap. This would correspond to an annual return of 15.8%. Since the companies in the portfolio are likely to continue to grow, this return would probably not be enough to close the gap, so the upside is even greater. And over the next 10 years, from today’s starting point, this company has the potential to grow by as much as 20% per year. So if you are a buy-and-hold investor with a long enough time horizon, this company is probably a better choice than an S&P 500 ETF because of its upside potential and its diversified portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here