Paramount Global (NASDAQ:PARA)(PARAA) is a media and entertainment company that is currently trading at decade lows. Suffering from widespread writer strikes, underperforming cinema releases, pressure in the advertising market and a debt load of over $15.5b, the common shares are down over 40% Y/Y. The price correction could be an overreaction by the market and might turn Paramount into an asymmetric bet, for reasons which we will discuss below.

Why is Paramount down?

Paramount is currently suffering under a mix of different external and internal circumstances:

- Earlier this year, the company announced a significant cut in dividends from $0.24 to just $0.05, causing a major drop in share price.

- The 2023 writer strikes are causing disruptions in the company’s content creation engine and also creating uncertainty regarding future cost structures for new content.

- Recently, Paramount’s movies have had disappointing box office performances. Both the latest Mission: Impossible movie and the latest Transformers movie, which usually are top-performers for the company, underperformed at the box office and barely broke even.

- Pressures in the advertising market are significantly affecting Paramount’s TV Media business, which can be considered the cash cow Paramount is using to fund its other business segments. In their Q2 2023 report, Paramount is quoting a 10% decrease in TV Media advertising revenue Y/Y.

- With a debt load of over $15.5b as per their Q2 2023 report, the company has a big debt load which is especially significant in a high-interest environment. At current rates, the company is posting a net yearly interest expense of around $800m.

- Paramount is significantly investing in their DTC streaming services (mainly Paramount+) costing the company billions so far. The company is mainly using cash generated by its TV Media segment which, as discussed above, is itself struggling with declining revenues.

Paramount’s assets

Paramount currently is posting a book value of around $21b. Excluding goodwill of about $16.5b, there is a book value of about $4.5b. We can look closer at the company’s main assets to see if the real value of the company’s assets is higher than the book value minus goodwill.

Portfolio

Over its 100+ year history, the company has accumulated an impressive portfolio of owned franchises and highly valuable rights. With owned titles like SpongeBob SquarePants, Indiana Jones, Top Gun, Mission: Impossible, and Terminator, just to name a few, it is easy to say that Paramount’s portfolio is easily worth billions.

If all else fails, the company will always have the theoretical opportunity to either sell off some of its portfolio or license it for added revenue without any added costs. The company already seems to be pushing for higher licensing revenues, posting a 17% “Licensing and other revenue” increase in their last quarterly report.

While it is difficult to estimate a fair value for their portfolio, I will assume that the current book value for their programming and other inventory is not higher than the fair value.

Real Estate

As per their last annual report, Paramount owns significant real estate in highly desired locations. The most notable are:

- CBS Broadcast Center in New York – 860,000 sqf

- Cloud Center in Hauppauge, NY – 170,000 sqf

- Paramount Pictures Studio in Los Angeles – 1.86m sqf

The (former) CBS Studio Center in LA was sold for $1.85b in 2021, Paramount Pictures Studio in LA being bigger and more central, should be worth even more.

It is also worth noting that the company is also currently considering selling their New York CBS Broadcast Center which, by estimates, should raise a net price of at least $800m for the company.

I would estimate that currently, their real estate’s fair value is at least $1.5b higher than its book value.

Networks

Paramount owns different, highly successful, TV Media networks, the biggest one being CBS. CBS finished the 22-23 season as the most-watched TV network, marking its 15th straight year of claiming that title. The network also holds the title for most viewed broadcast series, most viewed news series, most viewed comedy and most viewed news program, based on average viewers. CBS being able to consistently produce highly successful owned-titles showcases its ability to keep up with trends and continue to innovate.

Besides CBS, Paramount owns other highly successful networks like Nickelodeon and Showtime, with which they are able to further generate TV Media revenue.

With Nickelodeon for instance being one of the top kids and young adult TV networks, it is also clear that Paramount is able to create successful content in specific niches too. Nickelodeon also shows significant synergies between their TV networks and films.

The last Paw Patrol movie for instance, was able to generate a gross box office of $144.3m worldwide. While the number itself might not appear very impressive, it can be considered a bigger success than some of the larger titles like the last Transformers movie, given the Paw Patrol movie had a budget of less than $30m. Paw Patrol can also be taken as an extreme example of successful IP creation and licensing from the ground up. From 2014 to 2020 the company posted $8b in global retail sales just for Paw Patrol licensed products.

With trends showing that sports live events are increasingly important viewer drivers, it is also worth noting that Paramount’s networks own broadcasting rights to top-sports events for years to come. With sports ad sales continuing to be attractive for networks too, some multi-year contracts with sports franchises like the NFL can be considered fairly future-proof revenue and profit-generating assets for the company’s networks.

We can conclude that the company’s networks continue to be valuable assets going into the future.

Simon & Schuster

In August 2023, Paramount announced the signing of a definitive agreement to sell book publisher Simon & Schuster for $1.62b. While the sale is still subject to some closing conditions, if successful, Paramount hints in their last quarterly filing that the proceeds will support their ability to fund their debt obligations. Simon & Schuster added around $250m to Paramount’s net earnings yearly.

Streaming

Coming to the elephant in the room regarding Paramount, is their streaming or “Direct-To-Consumer” (DTC) segment, which mainly consists of their streaming platform Paramount+.

Being a big cost-driver for the company, the DTC segment has been a negative Adjusted OIBDA driver since its inception. While the company can tout impressive headline-numbers like 40% Y/Y DTC revenue and Paramount+ subscribers in their last quarterly report, growth has been clearly slowing down during the last couple of quarters. In Q2 2023 the company has been only able to grow subscribers by just above 1% Q/Q, compared to a growth of almost 10% Q/Q in Q2 2022.

Amid the so-called “Streaming Wars”, streaming services across the board are encountering increased pressure from competition, as more services are launched. Other streaming providers have been battling with a decline in subscriber numbers, blaming increased competition and reduced consumer spending power. Disney’s streaming service Disney+ for instance, is reporting record subscriber losses.

Keeping in mind suppressed market conditions and high expenses for the DTC segment, we can expect that DTC will add considerable pressure and hurt the company’s bottom line for quarters to come. Even though Paramount is forecasting “significant earnings improvement” for 2024, for our analysis we remain pessimistic on the outlook for the DTC segment.

Future revenues and profits

We can make some cautious assumptions regarding the company’s future revenues and profits, keeping the above statements regarding the company’s assets in mind.

TV Media

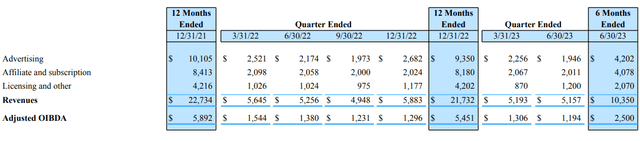

Paramount TV Media results (Paramount 2Q 23 Trending Schedules)

Given the previously mentioned circumstances regarding the networks, we will estimate that the TV Media segment of the company is going to continue adding an average of $19b in revenue and $4.5b Adjusted OIBDA to the company’s result in the coming 2 years. Given this represents a decline of around 5% to current numbers, this can be considered a pessimistic estimate, especially when keeping in mind that 2024 is an election year for the US with record political ad spend forecasts.

Direct-To-Consumer

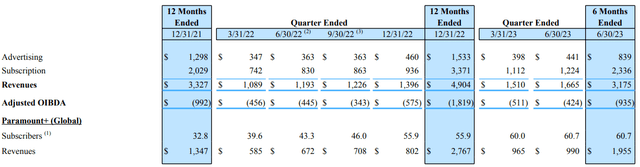

Paramount DTC results (Paramount 2Q 23 Trending Schedules)

Even though Paramount’s DTC products still have pricing headroom and significant growth momentum, we will stick with pessimistic estimates for the DTC impact on Paramount’s numbers. We will estimate that the DTC segment will add an average of $6.5b in revenue and a negative $1.5b Adjusted OIBDA to the company’s results in the coming 2 years. Given this represents almost a total halt in growth and no margin improvements, this can be considered a pessimistic estimate.

Filmed Entertainment

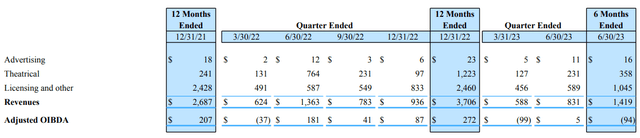

Paramount Filmed Entertainment results (Paramount 2Q 23 Trending Schedules)

The Filmed Entertainment sector is generally very volatile and highly depends on the mix of theatrical releases in any given quarter and year. With some highly-anticipated releases since their last quarterly report and also before the end of 2023, we can expect this segment to perform better than the last couple of quarters. We estimate the Filmed Entertainment segment will add an average of $4b revenue and $0.4b Adjusted OIBDA to the company’s results in the coming 2 years.

Combined

Combining all business segments we can come up with some rough, pessimistic estimates regarding Paramount’s revenue and Adjusted OIBDA over the next 2 years.

Based on the above assumptions, we are giving a pessimistic estimate of $29.5b yearly revenue on average and $3.4b yearly Adjusted OIBDA on average over the next 2 years.

Valuation

While asset sales like the CBS Broadcast Center in New York and Simon & Schuster are poised to significantly reduce the debt load and in turn interest expense in the future, we will continue to make pessimistic assumptions and assume an average debt load of $15.5b and net interest expense of $800m.

Even under the most pessimistic assumptions, Paramount can still cover yearly interest expense with Adjusted OIBDA by over 4 times. With our assumptions in mind, we can expect the risk of bankruptcy to be very low for Paramount in the coming years.

With Class B shares trading at $11.70, at the time of writing, the company has a market cap of under $7.8b, currently trading at a multiple of only ~2.3 to Adjusted OIBDA. Assuming a correction to a multiple of ~3.5 to our pessimistic assumptions, the price for the common shares could increase over 50% to over $17.50+, translating to an EV/Adjusted OIBDA of around 8 at our price target.

While the company’s book value, excluding goodwill, is standing at about $4.5b, based on our previously mentioned estimates on the fair value, we are estimating the fair value of the company’s assets being at least $6b due to valuable real estate. These assets can be considered a great margin of safety for common shares investors.

What to look out for and risks

Amid uncertainties across the board, it is important to closely monitor the results of the following quarters, making sure the company is not underperforming even based on our pessimistic estimates. Major issues in advertising sales in TV-Media, a decline in DTC revenue, or a lack of cost discipline which further decreases the company’s bottom line are some of the things to look out for in the next couple of earnings releases.

While the above cases could make me withdraw my buy-rating to a hold- or sell-rating, any surprise to the upside could shift my buy-rating into a strong-buy-rating. With the biggest uncertainty being Paramount’s DTC shift, a big positive surprise in DTC numbers could greatly improve the outlook for the common shares.

Conclusion

Paramount Global’s shares are down due to a mix of external and internal circumstances. Based on the underlying assets the company owns and the profitable business segments we are arguing that the drop in share prices since the dividend cut is exaggerated, putting both classes of common shares into undervalued territory.

Due to the current volatility across the board, it is important to closely monitor the company’s movements over the next couple of quarters to ensure that the company will not perform even worse than our pessimistic estimates.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here