Introduction from John P. Calamos, Sr., Founder, Chairman and Global Chief Investment Officer

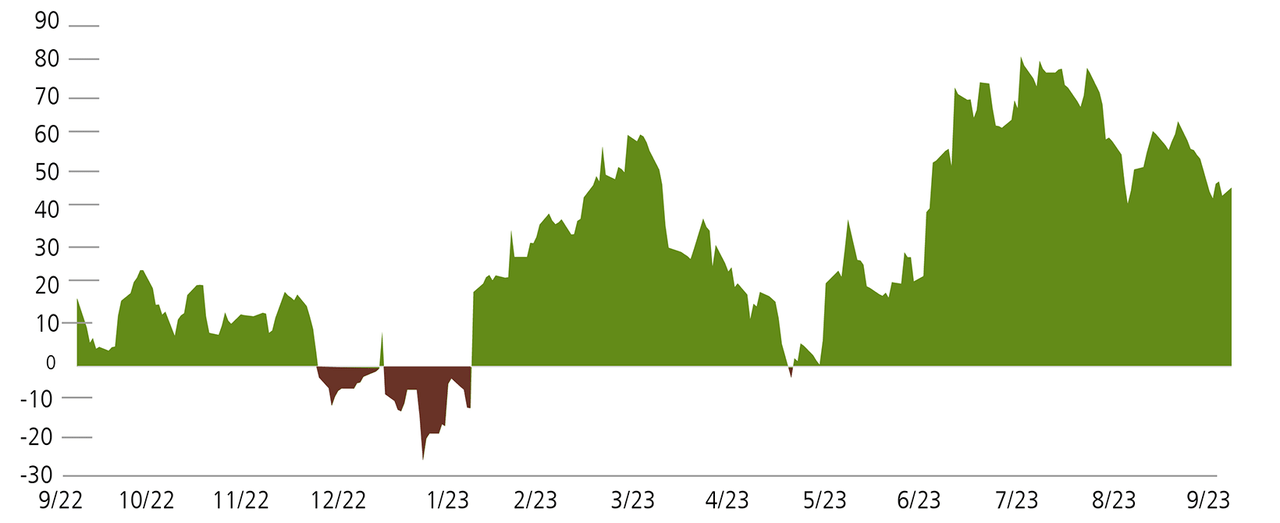

As the third quarter began, markets reflected investors’ upbeat mood, but this positive sentiment fizzled as the quarter wore on. Despite a steady stream of economic data continuing to surprise on the upside (Figure 1), investors became increasingly unsettled as they looked forward. Rising energy prices and rekindled inflation fears led to a ramp up in 10-year Treasury yields and deepened concerns about the sustainability of corporate earnings, the health of the consumer and economic growth overall. And although the Federal Reserve paused its rate tightening in September, the decision provided little comfort to markets as the central bank dashed hopes of imminent rate cuts by reinforcing prior guidance that rates would be higher for longer.

Figure 1. US economic data continued to surprise to the upside

Citigroup US Economic Surprise Index

Past performance is no guarantee of future results. Source: Bloomberg.

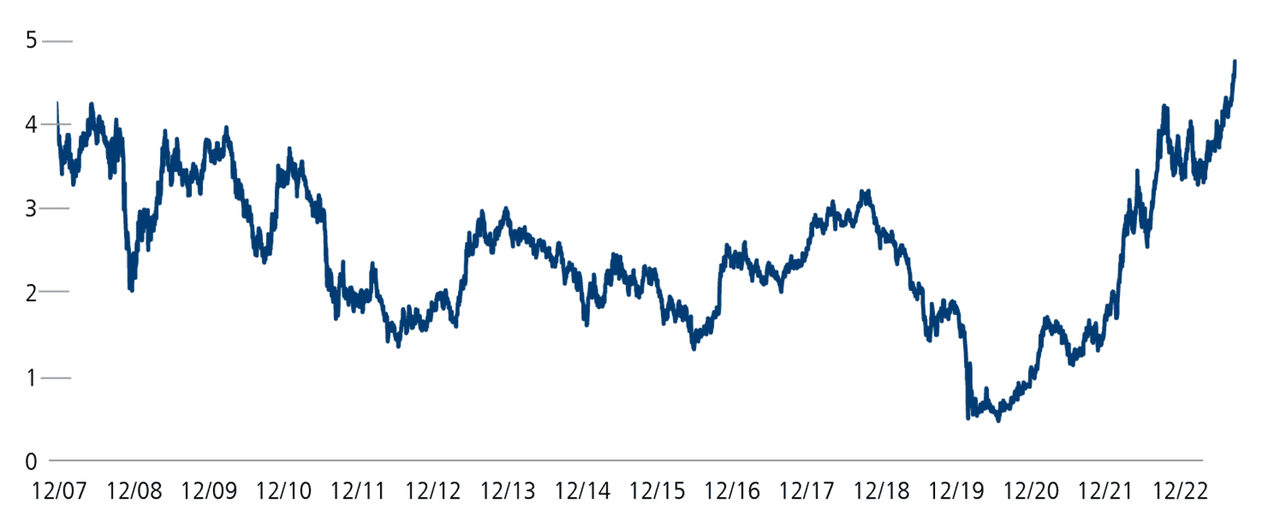

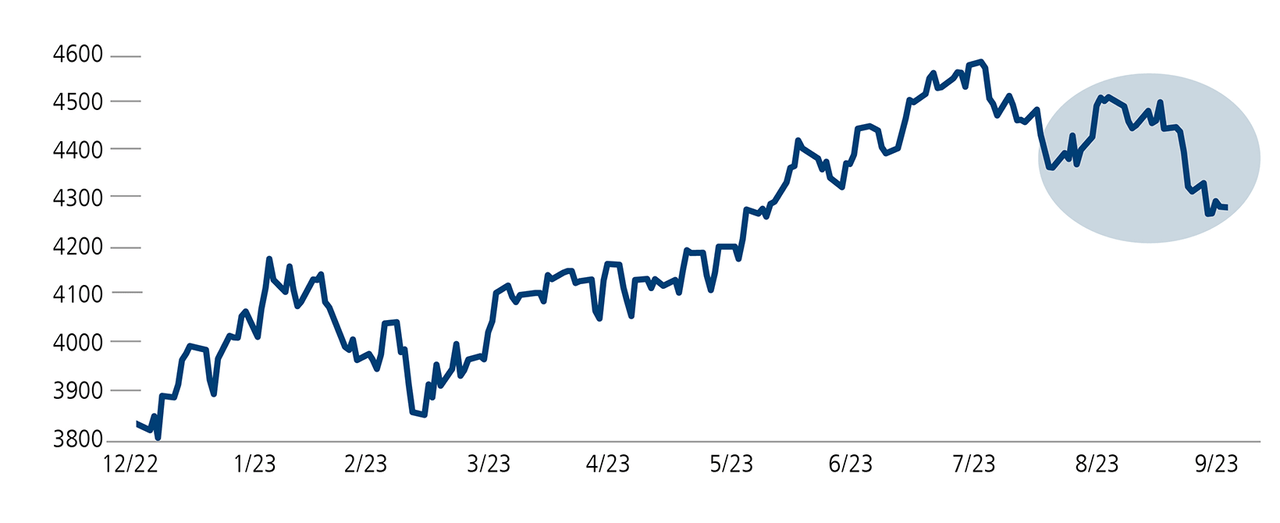

Higher interest rates are problematic for equities for a variety of reasons—higher rates ultimately lead to increased borrowing costs for companies and individual borrowers alike, which may create economic headwinds and crimp overall consumer and business spending. We have seen that equity valuations are also intricately linked to the long end of the yield curve and will, over long periods of time, generally fall as rates rise, and vice versa. Accordingly, as long-term Treasury yields have spiked to levels that we haven’t seen since before the Great Financial Crisis of 2008 (Figure 2), equities have come under renewed pressure (Figure 3).

Figure 2: Long-term yields have spiked to levels not seen in years

10-Year Treasury Yields (%)

Past performance is no guarantee of future results. Source: Bloomberg.

Figure 3. Stocks have fallen as investors digest the impact of a higher interest-rate environment

S&P 500 Index (September 30, 2022-September 30, 2023)

Past performance is no guarantee of future results. Source: Bloomberg.

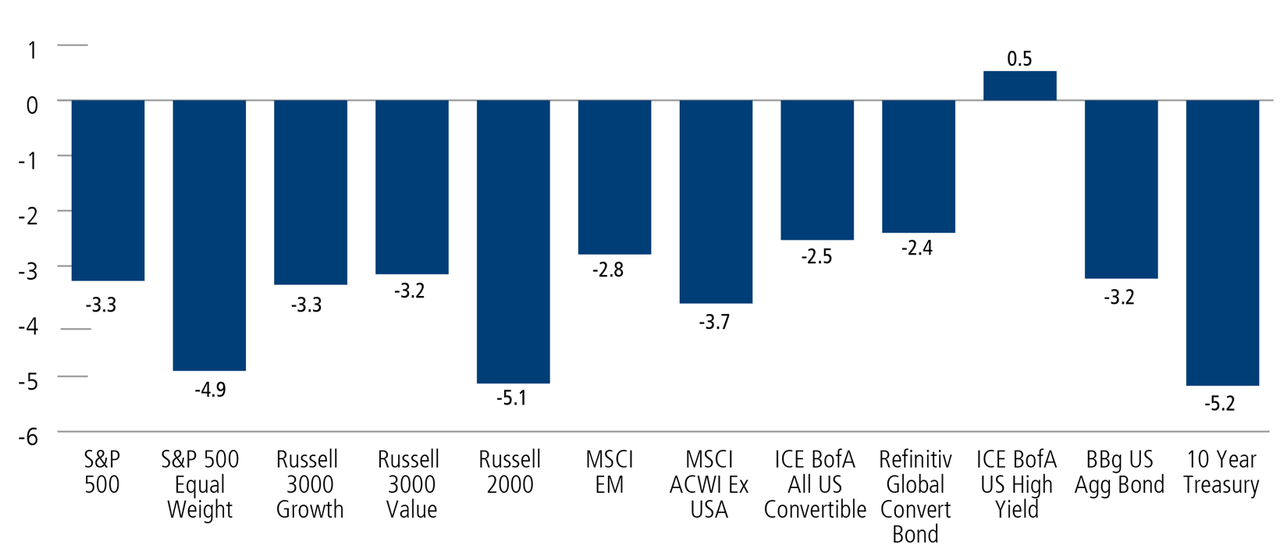

Reflecting this deteriorating sentiment, stocks and traditional bonds ended up in the red for the quarter, and to a remarkably similar degree (Figure 4). The high yield was the only major asset class to inch into positive territory, and small caps fared worse. In recent commentaries, we’ve discussed the wide performance differential between the market-cap weighted S&P 500 Index, which was propelled by the performance of a narrow pool of mega-cap technology-oriented names, and the S&P 500 Equal Weighted Index, which fared much worse. During the third quarter, the gap between the two narrowed and both fell into negative territory as investors worried about the impact of higher rates on growth-oriented companies, including technology.

Figure 4. For the quarter, global asset class performance was consistently lackluster

Total Return %

Past performance is no guarantee of future results. Source: Morningstar. Data as of 9/30/23.

Perspectives on Asset Allocation

When global financial markets decline broadly as they did in the third quarter, investors may be tempted to retreat to the sidelines. However, jumping in and out of the market is a dangerous strategy—investors tend to capture the downturns and miss the upturns. Instead, a far better course is to focus on establishing a well-diversified asset allocation that aligns with your needs and risk tolerance. Your asset allocation should be determined by your holding period—for example, the considerations are different if your holding period is six months or six years, and investors make a mistake just focusing on returns. Rather, we believe investors should seek to be well compensated for the risks they undertake.

In many cases, alternative investments can help investors optimize their asset allocations and provide an additional ballast during volatile markets. Calamos Phineus Long/Short Fund and Calamos Hedged Equity Fund, for example, are designed to complement traditional stock funds. Calamos Market Neutral Income Fund, our flagship alternative, and Calamos Aksia Alternative Credit and Income Fund, our private credit offering, provide ways to enhance a fixed income allocation, including in environments such as these when traditional bonds come under pressure. Finally, many investors may be well served by expanding their portfolios to include active ETFs.

There are Opportunities in Every Environment— Even Challenging Ones

Markets are forward looking, as are our teams. We see many signs pointing to slower growth and increasing risks across sectors. Global manufacturing data is trending down, and rising fuel prices are putting significant pressure on a wide variety of companies and many households. Meanwhile, retailers will likely struggle as the nest eggs that consumers amassed during the pandemic dwindle and student loan repayments start again. Fiscal policy uncertainty, already elevated (as we saw once again with this latest round of debt ceiling negotiations), will no doubt intensify as the US presidential election approaches. Against this backdrop, we expect sideways moving markets, rotation, and short-term volatility to continue.

Nevertheless, there are opportunities in all markets. We continue to see companies innovate and disrupt the status quo, creating entire new ecosystems of opportunity, from AI to biotech. It’s important to not get caught up in the emotion—either to the upside or the downside—because ultimately, we believe fundamentals will win out. Against this backdrop, our teams continue to focus on individual security selection, the identification of key growth themes, rigorous research, and multi-faceted risk management.

As you’ll read in the posts below, our teams are finding a breadth of investment potential across the global markets. They share their outlooks on the economy and markets, where they are finding opportunities, and how they are managing risks for the benefit of our shareholders.

2023: Now For the Harder Part

Calamos Phineus Long/Short Fund (CPLIX)

Michael Grant

- CPLIX reduced its net equity exposures in late July on the assumption that further improvement in inflation would be harder to come by due to the stickiness of labor incomes.

- There will be a time to acknowledge the heightened recession risks, but that is a storyline for 2024. For now, we are at the stage of the cycle where “good news is bad news.”

- We continue to emphasize a mix of select quality GARP opportunities and cyclicals that appear too cheap in the absence of a recession.

In last quarter’s review, we stated that the “Easy Part” of 2023 was behind us, and the third quarter confirmed this belief. Equities succumbed to a bearish mood in recent months, though the correction from the highs of early July has been orderly. The disinflation narrative that led markets higher from October 2022 into July has been suppressed by several less supportive narratives that imply equities could be stuck between a rock and a hard place (aka, the resilient economy).

CPLIX reduced its net equity exposures in late July on the assumption that further improvement in inflation would be harder to come by due to the stickiness of labor incomes. US consumers were never the source of the pandemic surge in prices but are now positioned to demand higher wages. This stubbornly energetic labor force is one reason the Federal Reserve will be slow to temper its restrictive policies and points to a “higher for longer” setting, which is weighing on equities and bonds alike.

This tightening of financial conditions is occurring in the context of an economy that seems well placed to absorb it, for now. The consumer is in good shape, employment markets are firm, corporate profit estimates are moving higher and fiscal policy is unusually pro-cyclical for this stage of the expansion. Higher yields thus appear well justified on the back of a resilient economy and a hawkish Fed. There will be a time to acknowledge the heightened recession risks, but that is a storyline for 2024. For now, markets are hostage to the direction of oil prices and the US 10-year Treasury yield—for better and for worse.

For much of the past 40 years, interest rates would be declining to new lows at this stage of the expansion, providing a liquidity impulse through refinancings and housing demand. Instead, investors are confronted by the gradual drain of liquidity that is apparent in the narrowing gains of almost all financial prices. Nominal economic growth is still healthy, but the persistent contraction of money and credit implies this has an expiry date. The soft-landing thesis will remain suspect in the eyes of investors until something changes here. And the longer the economy remains resilient today, the greater the likelihood of an eventual harder landing.

This higher level of real interest rates speaks to the time value of money and contrasts distinctly with the post-2008 era of “free money.” The important conclusion is that valuation should be imperative to investment selection after a long absence. In other words, it is becoming increasingly difficult to justify a growth-at-any-price mindset. For CPLIX, we have avoided the latter stocks and continue to emphasize a mix of select quality GARP opportunities and cyclicals that appear too cheap in the absence of any near-term recession.

CPLIX Positioning Outlook

| US SECTORS | STRATEGIC | TACTICAL |

|---|---|---|

| Financials | Negative | Negative |

| Consumer Discretionary | Neutral | Positive |

| Health Care | Positive | Selective |

| Technology (Mega Cap) | Positive | Positive |

| Consumer Staples | Negative | Negative |

| Energy | Neutral | Negative |

| Industrials | Neutral | Positive |

| Communication Services | Positive | Selective |

| GLOBAL/REGIONAL | STRATEGIC | TACTICAL |

|---|---|---|

| Europe | Negative | Negative |

| Emerging Markets | Neutral | Selective |

| US Domestic Consumer | Positive | Positive |

| Defensive, Stable Growth | Neutral | Selective |

| Technology Outside of Mega Cap | Selective | Negative |

| Global Trade | Neutral | Negative |

We advise clients to prepare for a different kind of decade ahead and the evidence of this is rolling in fast. Today’s financial cycle is quite different from that underpinned by the era of low and stable inflation. Equity exposures will need to be tactical and able to navigate a rising flurry of cyclical inflections that are different from the experience of many investors.

CMNIX: Continued Strength as Bonds Tumble

Calamos Market Neutral Income Fund (CMNIX)

Eli Pars, CFA

Summary

- During the quarter, rising interest rates delivered a blow to traditional bonds, with the Bloomberg US Aggregate Bond Index declining -3.2%.

- CMNIX posted a gain for the quarter, demonstrating the benefits of not being at the mercy of interest rate moves.

- We see an attractive opportunity set for convertible arbitrage continuing, supported by rising overnight interest rates and increased convertible issuance, while the Fund’s hedged equity component continued to benefit from higher interest rates.

- CMNIX maintains a 40% notional value of net long puts, which we believe will provide ample income opportunities without taking on an undue amount of residual equity risk—consistent with the fund’s investment mandate.

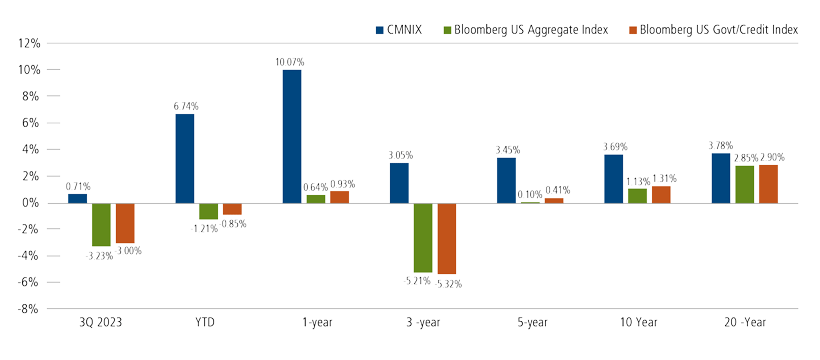

A History of Outperformance Versus Traditional Fixed Income

Calamos Market Neutral Income Fund (CMNIX) is designed to enhance a traditional fixed income allocation. The fund combines two complementary strategies—arbitrage and hedged equity—to pursue absolute returns and income that is not dependent on the level of interest rates. This approach has proven effective over the long term (as seen in Figure 1 below) but also through periods of extreme change in the markets (For more, see our post “Consistency Through Uncharted Waters.”)

Figure 1. CMNIX has outperformed bonds over the short term and long term

Source: Morningstar

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 2.75%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. The fund’s gross expense ratio as of the prospectus dated 3/1/2023 is 0.88% for Class I shares.

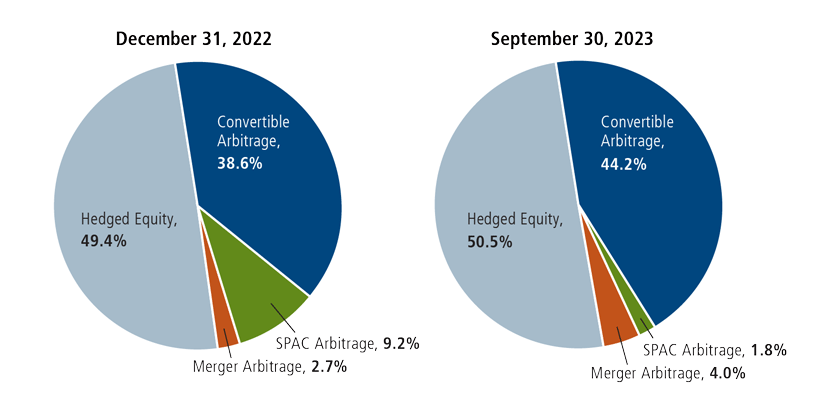

We monitor and manage the fund’s allocation between arbitrage and hedged equity and have maintained a roughly equal balance in recent months based on our view of strong relative opportunities in each.

The Arbitrage Strategy Reflects Our Optimism on Convertible Arbitrage

Within the arbitrage strategy, we have the flexibility to diversify among different sub-strategies, including convertible arbitrage, merger arbitrage and special purpose acquisition company (SPAC) arbitrage. During the third quarter, each of the arbitrage sub-strategies was up.

We continue to like the opportunity in convertible arbitrage most, and the fund’s allocation to convertible arbitrage has grown from 39% at the start of the year to 44% on September 30 (Figure 2). We expect to continue adding to convertible arbitrage, particularly if we see the attractive new convertible issuance that we anticipate.

Figure 2. We have increased CMNIX’s convertible arbitrage allocation in 2023

The portfolio is actively managed. Holdings subject to change daily.

Why We’re Bullish on Convertible Arbitrage

A principal driver for our bullishness in convertible arbitrage is our heightened return expectations for the strategy on the back of the rise in overnight interest rates. Convertible arbitrage returns have historically been correlated with overnight rates. This is because of the rebate the fund receives on its short stock positions, which is directly tied to the fed funds rate. Although returns don’t necessarily go up tick-for-tick with rates, we expect a meaningful tailwind in 2023 and beyond. Conditions for convertible arbitrage generally improve as short-term interest rates move higher. One factor, for example, is that rebates on short stock positions are highly correlated with the level of the fed funds rate. Markets continue to price in that the recent tightening by the Federal Reserve will remain for the near term.

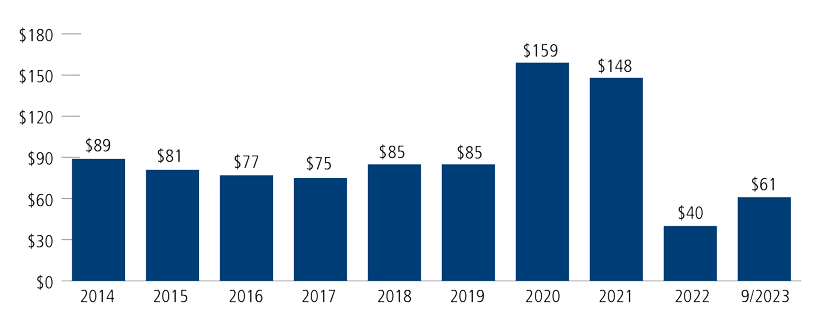

Increased convertible issuance is also favorable. We continue to see the potential for a large uptick in investment-grade issuance. During the third quarter, we saw signs that this trend is taking hold (Figure 3), including a large investment-grade oil company domiciled in Italy. According to Bank of America Global Research, 30% of year-to-date issuance has been investment grade, up from 7% in 2022.

Figure 3. Healthy convertible issuance provides opportunities for convertible arbitrage

Global convertible issuance, $ billions, year to date as of 9/30/23

Source: BofA Global Research.

Across the credit markets, a large maturity wall is on the horizon, beginning in 2025. As companies begin to address their refinancing needs, we maintain our belief that convertibles will be a popular choice for issuers. We just don’t know whether that will be this year or next. With most potential issuers in quiet periods during the first month of every quarter because of pending earnings releases, we expect October issuance to be low. In November and early December, we’ll see just how motivated companies are to raise capital, but the next leg up in convertible issuance looks more likely to be a 2024 story.

The increase in convertible arbitrage has offset a reduction in the SPAC portion of the portfolio. SPACs are now 2% of CMNIX after peaking at almost 10% of the fund. While we have sold a few SPACs, most of the decrease has resulted from the natural runoff of 2021 issuance with terms of two years or less. Over the last few years, SPACs served the fund well, contributing upside with limited volatility, and we would continue to buy new SPACs on the terms we bought them in 2021. However, the SPAC new issue market has been quiet since late 2021.

Hedged Equity Strategy: Focused on Steady Returns

We position the hedged equity strategy with the goal of providing steady returns whether the stock market is going up or down. In a quarter when both stocks and bonds declined (with the S&P 500 Index and Bloomberg US Aggregate Index both falling more than -3.0%), the hedged equity component of CMNIX was flat.

In a higher interest environment, we can earn more from selling calls, which highlights part of the attraction we see in the hedged equity strategy with overnight interest rates at 5%. We have been more defensively positioned in recent years, which proved advantageous over the quarter.

In Calamos Market Neutral Income Fund, we have consistently maintained a 40% notional value of net long puts. This has served the fund well, and we believe it will continue to do so, based on the parameters of the fund’s mandate. Given that CMNIX is designed to serve as a fixed income alternative, we are especially mindful of taking on too much residual equity risk.

When Textbook Asset Allocation Falls Short, CIHEX Uses Higher Rates to Earn Extra Credit

Calamos Hedged Equity Fund (CIHEX)

Eli Pars, CFA

Summary

- We manage CIHEX with the goal of dampening equity portfolio volatility and managing drawdowns.

- As a rise in long-term Treasury rates roiled both stocks and bonds during the quarter, CIHEX demonstrated relative resilience, declining less than both the stock and bond market.

- Whereas higher interest rates cause headwinds for bonds and stocks, our hedged equity strategy can benefit because higher rates give us the opportunity to earn more from selling calls.

CIHEX for enhanced equity diversification

The sell-off that began a few months ago in the long end of the Treasury market accelerated in September, ultimately igniting a pullback in the equity market. And once again, the textbook asset allocation of 60% stocks and 40% bonds failed investors, with both the S&P 500 Index and the Bloomberg US Aggregate Bond Index declining more than 3.0%. The lack of diversification benefits between stocks and bonds seems to be a recurring theme in our post-zero-percent interest-rate world.

Given this backdrop, we believe the case for Calamos Hedged Equity Fund remains as strong as ever. Calamos Hedged Equity Fund (CIHEX) is an equity alternative designed to help investors dampen the impact of equity market volatility and drawdowns. During the quarter, the fund performed in line with this goal, mitigating the market drawdown.

Tailwinds for hedged equity

We continue to like the opportunity set in hedged equity. The rise in overnight interest rates coupled with relatively low volatility has led to some interesting trades becoming available in the options market. For example, we have positioned the option book with a trade that is structured to pursue 65% of the market’s upside and 35% of the market’s downside at its expiration in 15 months. In a higher interest environment, we can earn more from selling calls, which highlights part of the attraction we see in the hedged equity strategy with overnight money at 5%. (For more on the impact on interest rates on option pricing, see Co-Portfolio Manager Dave O’Donohue’s video blog, “Higher Rates are an Opportunity for Hedged Equity Strategies.”)

Our investment approach is designed to take advantage of market opportunities by being favorably positioned for as many outcomes as possible. Consistent with this, we continually seek ways to enhance our process while maintaining our intended risk/reward parameters. Since CIHEX’s launch almost nine years ago, having at least a 40% notional value of net long puts aligned with the market environment and has served the fund well. The fund is currently above the floor, and we anticipate this positioning will continue over the short to medium term. However, the environment calls for us to allocate capital in a more efficient manner due to current tail risk pricing. This environment makes put spreads more attractive (bidding up the put we are selling in a put spread). Given our expectation that this dynamic will persist, we believe there will likely be periods when a more flexible approach (without a hard minimum) will allow us to maintain comfortable levels of downside risk mitigation more efficiently.

Average Annualized Total Returns, as of 9/30/2023

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower.

The fund’s gross expense ratio as of the prospectus dated 3/1/2023 is 0.92% for Class I shares.

Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average. All performance shown assumes reinvestment of dividends and capital gains distributions.

Harnessing Convertible Opportunity: Bottom-Up Selection and Growth Themes Guide the Way

Calamos Convertible Fund (CICVX)

Jon Vacko, CFA, and Joe Wysocki, CFA

We believe:

- Our proprietary research and identification of secular themes position Calamos Convertible Fund advantageously.

- Continued emphasis on balanced convertibles aligns with CICVX’s pursuit of lower-volatility equity participation.

- Select opportunities exist in among yield alternatives, but we maintain a cautious stance on the most distressed credits.

- Recent issuance has offered investor-friendly characteristics, and a “higher-for-longer” interest rate environment may stoke increased convertible issuance.

The beginning of the third quarter of 2023 was characterized by a continuation of the equity rally of the first half of the year. Amid cooling inflation, stable geopolitical risks, and slowing but healthy economic and employment conditions, investors appeared more comfortable embracing a soft-landing narrative, However, the third quarter ended on a choppy note. Despite the Fed’s most recent pause in raising interest rates, market participants weighed the implications of the central bank’s intentions to keep rates “higher for longer.” Furthermore, investors also digested the potential impacts of the United Auto Workers strike, higher gas prices, and the prospect of a government shutdown; we would note that these have historically been more transitory risks to the economy.

Looking forward, we are cautiously optimistic but see multiple positives and negatives pushing and pulling the market. We believe additional Fed moves will remain data-dependent. This likely generates heightened uncertainty, but volatility has historically created opportunity in the convertible asset class. Any stabilization of the macro backdrop could turn what has been a narrow, larger-cap-driven S&P 500 leadership period into broader strength, which we believe would benefit convertibles, given many issuers lean toward more mid-cap, growth-oriented companies.

Within Calamos Convertible Fund (CICVX), our overall focus remains on bottom-up company selection and actively managing risk/reward tradeoffs. Convertible securities combine attributes of stocks and bonds and vary in their levels of equity and fixed income sensitivity. Within CICVX, we maintain our preference for balanced convertible structures that provide a favorable asymmetric payoff profile by offering potentially attractive levels of upside equity participation with less exposure to downside moves. We have also found opportunities among convertibles with higher levels of fixed income sensitivity; these can benefit from spread compression while offering attractive yields and good structural risk mitigation from potential equity market weakness. We remain selective in regard to the lowest quality credits, instead preferring companies with solvent business models, improving financial metrics, and balance sheet liquidity.

Technology, health care and consumer discretionary remain CICVX’s largest sector allocations. Relying on our proprietary bottom-up company analysis, we favor companies with improving margins and free cash flow, accelerating returns on invested capital, attractive valuations, and the ability to execute well despite macro uncertainties. We also focus on identifying innovative companies positioned to benefit from enduring secular themes. Secular trends, such as cybersecurity and electric vehicle adoption, serve as a tailwind in uncertain periods and help us identify firms with valuations that are most likely to be rewarded over time. Other secular themes represented in the fund include automation, productivity enhancement, and artificial intelligence. Companies exposed to these themes are advantageously positioned as businesses seek solutions to higher labor, manufacturing, and interest costs in the current economic environment.

Convertible new issuance accelerated into September and is on track to match historical long-term trends for the year. This year’s issuance has been characterized by investor-friendly higher coupons and lower conversion premiums. We’ve also been encouraged to see more investment-grade companies issue convertibles. We remain optimistic about issuance prospects and believe the pace will continue to be strong as companies increasingly recognize the lower-borrowing-cost benefits of issuing convertibles in lieu of traditional bonds. The combination of a sizable amount of debt maturing in 2025 across bond markets and the Fed’s higher-for-longer interest rate stance could serve as an accelerant for near-term issuance.

Ready for Market Upticks and Potential Pullbacks Outlook

Calamos Global Convertible Fund (CXGCX)

Eli Pars, CFA

- Oil prices, Fed policy, and political uncertainty contribute to a questionable growth outlook for 2024.

- Given these crosscurrents, our focus remains on achieving the best risk/reward profile through bottom-up security selection.

- Convertible issuance remains strong year-to-date, and we expect healthy issuance in 2024 as companies seek to refinance maturing debt across the credit markets.

During the third quarter, stock and bond markets fell into the red by about the same degree. Global convertibles, which blend equity and fixed income characteristics were not immune to these pressures, but provided a degree of resilience, with the Refinitiv Global Convertible Bond Index losing less ground.* In a post-zero interest rate world, we don’t believe we’ve seen the last of simultaneous declines in stocks and bonds. We believe that global convertibles can continue to provide benefits, with active management enhancing the potential of the asset class.

The Fed seems (mostly) done with raising rates, but the market’s obsession with the Fed continues, with investors now fixated on when the Fed will start cutting rates again. But with the economy holding up quite well, it’s hard to see why the central bank would cut rates unless inflation falls below its 2% goal. With oil prices flirting with triple digits, that final drop in inflation may also be pushed out further on the horizon. And that’s before we consider that we have a big election next year. It’s hard to see the Fed wanting to get in the middle of that mess.

All of this combines for a questionable outlook for growth in 2024. This is the point where we remind our readers that we’re not macro traders, just convertible managers. We will stick to our fundamental process and work to get the best risk/reward profile possible. We continue to position Calamos Global Convertible Fund to participate in upside equity rallies while also seeking to manage the downside if the market pulls back. The Fund remains overweight to the US and the technology sector and underweight Europe.

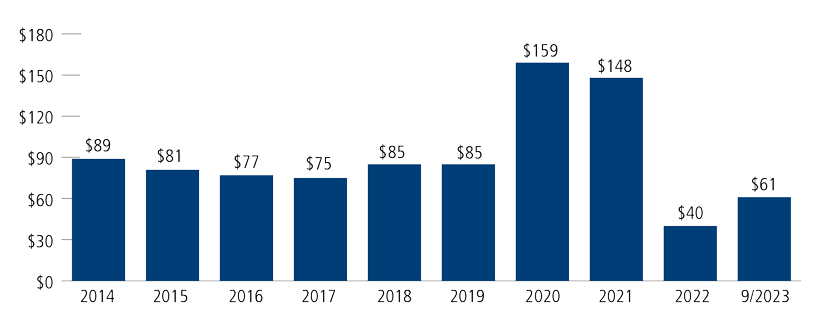

The global convertible market continued to see healthy issuance in the third quarter, and we remain active in the new issuance market. Global issuance totaled $20.5 billion for the third quarter and $60.9 billion year to date, which compares favorably with $39.5 billion in issuance for all of 2022.

Figure 1. 2023 global convertible issuance has proceeded at a healthy pace

$ billion, year to date as of 9/30/23

Data as of 9/30/23. Past performance is no guarantee of future results.

Source: BofA Global Research, ICE Data Indices, LLC.

In prior commentaries, we have discussed the potential for a large uptick in investment grade issuance. During the third quarter, we saw signs that this trend is taking hold, including a large investment-grade oil company domiciled in Italy. According to Bank of America Global Research, 30% of year-to-date issuance has been investment grade, up from 7% in 2022.

Across the credit markets, a large maturity wall is on the horizon, beginning in 2025. As companies begin to address their refinancing needs, we maintain our belief that convertibles will be a popular choice for issuers. We just don’t know whether that will be this year or next. With most potential issuers in quiet periods during the first month of every quarter because of pending earnings releases, we expect October issuance to be low. In November and early December, we’ll see just how motivated companies are to raise capital, but the next leg up in convertible issuance looks more likely to be a 2024 story.

Finding Opportunities in a More Muted Growth Environment

Calamos Growth and Income Fund (CGIIX)John Hillenbrand, CPA

- The continued slowing of the US economy and more balance between opposing growth forces warrant a neutral risk positioning for the fund, in our view.

- We believe optimal portfolio positioning includes selective risk positioning in areas that have real growth tailwinds, in companies with improving returns on capital in 2024, and in equities and fixed income with valuations at favorable expected risk-adjusted returns.

- As the growth outlook for many parts of the US economy shifts, we also seek to capitalize on shorter-term cyclical growth themes.

- Over the short- and intermediate-term, improved real returns on capital can drive higher equity prices, and we see attractive long-term upside in the US equity market from current market levels, which we believe are at fair value for a majority of US companies.

At the beginning of 2023, we outlined the case for increasing the risk in the fund, focusing on selective areas of the economy that we believed should show improving economic growth in 2023 and 2024 as well as on companies that could improve returns on capital during that time. Our premise to selectively add risk was based on several factors, including our conviction in the long-term US economic growth trajectory, positive policy changes, and improvement in certain parts of the economy, despite some opposing forces that were slowing growth down in other economic sectors. The events of the first three quarters of 2023 (the slowing of central bank rate increases, continued moderate slowing of inflation and economic growth, corporate cost-cutting measures, and the acceleration of spending in AI-related areas) have in aggregate supported that risk profile. Risk asset returns were positive during this time, although there was a significant dispersion of returns across sectors and industries.

As we look forward to the end of 2023 and into 2024, the growth outlook appears more muted than at the beginning of 2023. Opposing economic forces have become more balanced as policy shifts (elimination of some government policies and a cost-cutting agenda in the US Congress) are balancing out positive end-demand trends at the consumer and corporate levels. We continue to see slowing but positive economic growth over the next year, but the timing for a reacceleration in growth is more difficult to predict. In addition to this more balanced growth view, the growth outlook for many parts of the US economy continues to shift (for example, due to rising energy prices in recent months versus a decline in the first part of the year, and a slowing of travel consumption from the fast pace over the summer). Therefore, we remain vigilant in our effort to identify short-term cyclical investment themes. We continue to assess the investment opportunities within this environment with a further focus on real growth and return improvement areas. Finally, we continue to monitor security and asset-class valuations to target appropriate returns in this volatile environment.

In addition to areas with favorable cyclical factors, we believe companies that can improve profitability in a slower-growth environment are good investments. Many companies are focused on improving their returns on capital through improved efficiencies, normalized supply chains, and revised investment strategies based on the current interest-rate environment. The pace of corporate cost-cutting and restructuring has increased over the past several quarters across several areas, providing more opportunities to identify companies with improving returns on capital. Over the short and intermediate term, improved real returns on capital should drive higher equity prices.

We remain confident that the positive long-term growth trajectory of the US economy and the cash flow generation capabilities of US companies are intact. The ability of management teams to identify emerging short- and long-term trends and the adaptability of business models and cost structures are central to our long-term favorable view. We see attractive long-term upside in the US equity market from current market levels, which we believe are at fair value for a majority of US companies.

We believe the best positioning for this environment is a defensive risk posture, with added risk in specific areas that have real growth tailwinds, in companies with improving returns on capital in 2024, and in equities and fixed income with valuations at favorable expected risk-adjusted returns. We see compelling prospects for companies that have exposure to new products and geographic growth opportunities (examples can be found in healthcare, electric vehicles, and AI-related infrastructure and software), specific infrastructure spending areas (in materials and industrial sectors), and the normalization of supply chains and parts of the service economy.

We are still favoring higher-credit-quality companies with improving free cash flow. We are selectively using options and convertible bonds to gain exposure to some higher-risk industries. From an asset-class perspective, cash and short-term Treasuries remain useful tools to lower volatility in a multi-asset-class portfolio given their yields.

Quality Growth Holds Its Appeal as Economic Pressures Mount

Calamos Growth Fund (CGRIX)

Matt Freund, CFA, Michael Kassab, CFA

We believe:

- Mixed economic signals warrant vigilance.

- Companies with exemplary balance sheets and attractive cash flows offer the best prospects for near-term outperformance.

- We see long term upside in AI and the benefits it can bring to a vast array of businesses.

The third quarter started off with significant momentum. The economy had managed to digest the earlier banking disruptions without a hitch, the consumer was still spending at a healthy pace, and energy prices were well behaved. Stocks across all sectors generally rose through the end of July.

That optimism quickly faded as a growing list of concerns came into focus. Energy prices began a steady climb and are now once again approaching $95 a barrel. Interest rates have become increasingly problematic (despite the Fed pause) as 10-year Treasury rates rose to levels not seen since the 2008 recession. At the same time, the market is growing increasingly concerned about the outlook for corporate earnings (which were expected to show significant growth in the second half of the year) as higher rates, labor costs, a stronger dollar, and weakening consumer expectations become more widespread.

Our confidence in “fortress” growth stocks persists although many gave back some of their strong gains in the third quarter. Importantly, within the US equity market, as measured by the S&P 500 Index, there were only two positive sectors in the quarter (energy and communication services), while traditionally defensive sectors, like utilities and consumer staples, underperformed. Smaller companies fared even worse.

The economy continues to flash mixed signals. The current trend of positive but tepid growth will likely continue for the next couple of quarters. However, a surprising number of factors are pointing toward further softening: the inverted yield curve, tighter lending standards, higher energy costs, increasing labor costs, and higher financing costs. These all add up to growing profit pressures on the private sector. In addition, the rest of the world remains weaker than the United States and, therefore, unlikely to provide a boost to domestic growth.

In an environment where growth may prove increasingly scarce, we believe asset-light companies with the flexibility and financial strength to continue funding their growth initiatives—regardless of the economic backdrop—should be able to outperform. As a result, we continue to favor quality growth companies with stellar balance sheets and attractive free cash flows. We believe these companies are better positioned to capitalize on the opportunities that volatile markets provide, as seen in the largest companies’ first-mover advantage of AI. On the other end of the spectrum, we are increasingly cautious about the outlook for unprofitable technology companies.

Although some of the euphoria surrounding AI stocks has abated in recent weeks, we have maintained considerable exposure to this investment theme through our positioning in semiconductor, cloud infrastructure, and software stocks. Undoubtedly, investor enthusiasm around AI will ebb and flow over time, but we remain confident this technology will bring new applications and widespread benefits to a vast range of businesses beyond the technology sector. As always, we remain committed to a selective and thoughtful approach as we sort through what lies ahead for this exciting innovation.

A Market Focused on Growth Fundamentals: Early Innings for Our Investment Style

Calamos Timpani Small Cap Growth Fund (CTSIX), Calamos Timpani SMID Growth Fund (CTIGX)

Brandon Nelson, CFA

- We expect start-stop and rotational market conditions over the near term but believe we are in the early innings of an upcycle for our investment style

- The Calamos Timpani funds are tilted toward stocks that we believe offer above-average growth prospects and very visible fundamental strength—and we are encouraged these characteristics are gaining traction in the market.

- Small caps are relatively inexpensive, have tended to do well in periods after bear market bottoms and are entering what historically has been a seasonally strong period running from October through April.

The third quarter saw overall weakness in equity markets, led lower by mid and small cap stocks. The smallest of the small were especially weak this quarter, as seen in the performance of the Russell Microcap Index, down -7.9%, and in the Russell Microcap Growth Index, down -12.0%

The market was in “risk-off” mode for most of the quarter, especially in August and September, two months that have tended to be seasonally difficult for equity markets. The underlying weakness in equity prices was at least partially caused by rising oil prices and rising 10-year US Treasury bond yields. Both rose each month of the quarter and caused investors to question the overall outlooks for earnings estimates and the valuation multiples paid on those estimates.

In addition to increasing oil prices and Treasury yields, another theme that gained traction during the quarter related to health care and a specific group of weight loss drugs known as GLP-1s (short for glucagon-like peptide 1 agonists). Clinical data continues to be released, but investors are encouraged by the potential for these drugs to improve not only patient aesthetics but also overall patient health. This excitement does have a downside for other industries, however, as some investors suspect a healthier society may result in lower demand for certain medical devices and medical procedures. We won’t know the true implications for some time, but stocks are moving in the meantime.

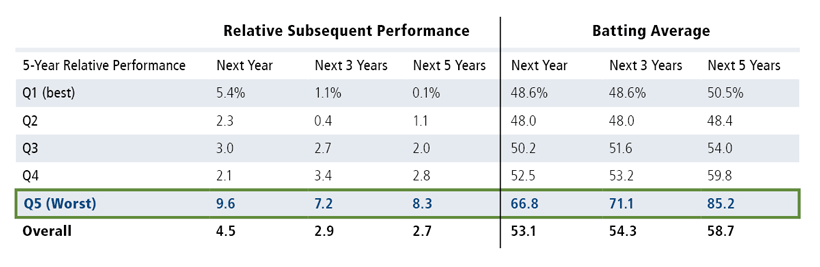

Although small caps have underperformed during the quarter and year to date, the outlook for them looks compelling. Small caps are relatively inexpensive and have tended to do well in periods after bear market bottoms (see our post “5 Reasons for Small Caps and Calamos Timpani Small Cap Growth Fund”). Small caps are also entering what historically has been a seasonally strong period running from October through April. Regarding valuation, small caps look extremely stretched to the downside relative to large caps. Looking back at more than 90 years of data, research by Jefferies shows that the most significant dislocations have historically tended to be a positive indicator for future small cap performance. The table below shows the historically strong relative performance for small caps versus large caps over the next one, three, and five years, with high probabilities of confidence (“Batting Average”).

When performance has been this bad, small caps have historically enjoyed long bounce backs

Outperformance of small caps over large caps

Past performance is no guarantee of future results.

Note: performance is annualized. Batting average is the % of time that small beats large. Source: Center for Research in Security Prices (CRSP®), the University of Chicago Booth School of Business, Jefferies. Large and small are defined by CRSP based on placing market caps into deciles. Deciles 1 and 2 are large and 6 through 8 are small.

We believe Calamos Timpani Small Cap Growth Fund (CTSIX) and Calamos Timpani SMID Growth Fund (CTIGX) are well positioned. Both funds are tilted toward stocks that we believe offer above-average growth prospects and very visible fundamental strength. Stocks with those characteristics were out of favor for most of 2022 as valuation multiples compressed, but since early February 2023, many of these stocks are back on track with the market.

In other words, we believe we are in the early stages of a new upcycle for our particular investment style. That, combined with the potential to see a recovery in the overall small cap asset class, has us feeling upbeat on an intermediate-to-long-term basis. Admittedly, the short-term is murky, with many macro sources of concern. This murkiness is causing performance to have many stops, starts, and rotations. We’re focused on finding stocks that have company-specific secular growth, and thus are theoretically less vulnerable to some of that macro murkiness. We believe this approach makes the most sense, especially in this environment.

Global Investment Themes Spotlight, 3Q 2023

Calamos Evolving World Growth Fund (CNWIX) Calamos Global Opportunities Fund (CGCIX), Calamos Global Equity Fund (CIGEX), Calamos International Growth Fund (CIGIX), Calamos International Small Cap Growth Fund (CSGIX)

Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA

The following is an adaptation of our recent commentary, “3Q 2023 Global Investment Theme Spotlight: India, obesity treatments, Chinese electrical vehicles and energy” (Read the commentary in its entirety here).

Our investment process marries bottom-up fundamental analysis with the identification of top-down considerations. Here, we highlight four themes represented in our portfolios:

- In India, pro-growth policies are bearing fruit on the vine of the country’s long-term growth story, with stocks across sectors benefitting.

- Demand for obesity treatments creates growth opportunities not only for biopharmaceuticals but also for companies solving supply chain challenges.

- Supported by policy tailwinds, China continues to extend its global leadership in electric vehicles.

- In the energy sector, favorable supply/demand trends support our positive but selective outlook.

Theme 1: India’s Pro-Growth Policies

We believe India’s growth story has plenty of runway ahead. Many reforms have taken root and are bearing fruit, and the execution of additional pro-growth policies pushes on. All of this comes as India establishes itself as a regional manufacturing hub through its “Make in India” program, Production Linked Incentive scheme, and friendshoring, while leveraging its massive lower-cost workforce and strengthening its consumer base. These forces are coming together to drive capex and housing upcycles. Job and wage growth remain robust across the country, consumer balance sheets have been bolstered post-Covid, and corporate balance sheets are in stronger shape after a multiyear deleveraging cycle.

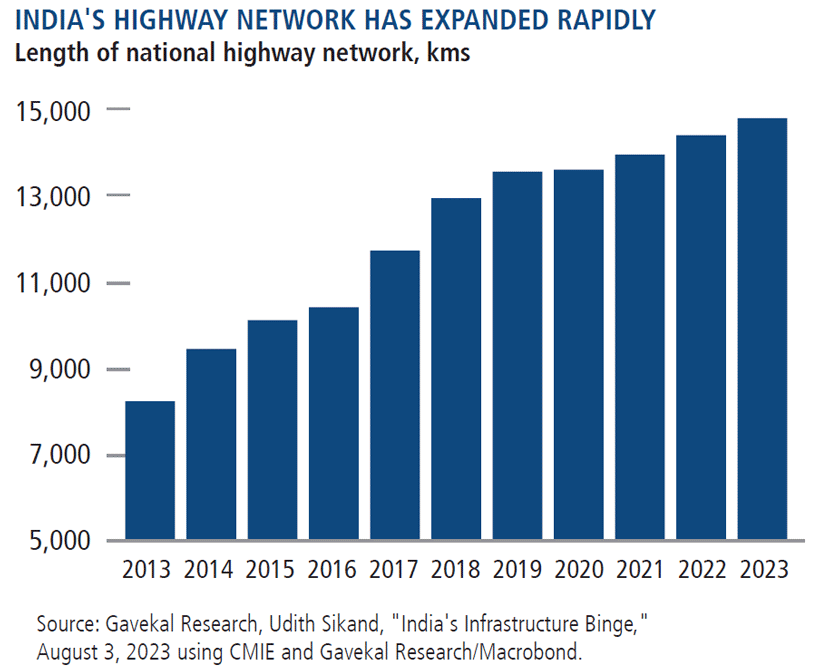

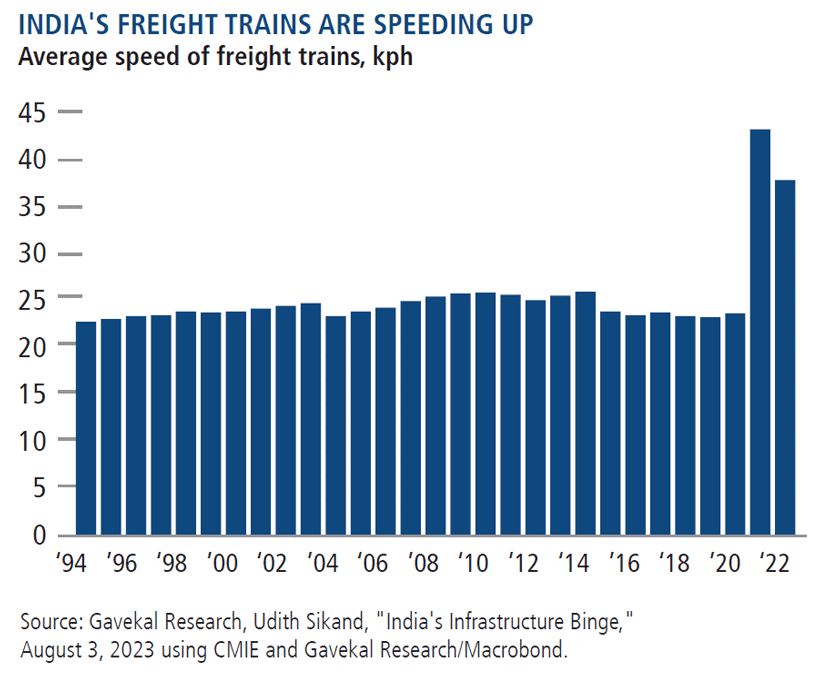

The Indian government has implemented a range of strategies to enhance the country’s logistics capabilities (including the expansion of highways and faster freight trains), thereby raising overall economic productivity and expanding India’s importance in global trade. Pro-growth policies are taking hold in private markets as well, with the size of total private project announcements reaching a new decade high.

Although energy prices and equity valuations both add some risk of near-term volatility to India’s equity market, we believe there is abundant opportunity that will only increase in the medium and long term, supported by a confluence of growth in the manufacturing and consumer sides of the economy. Over the past quarter, we’ve increased positions in India’s electronics manufacturing, railways, transport, autos, online travel, food delivery, and jewelry industries.

Theme 2: Obesity Treatments

Over the past three years, a key biopharmaceutical breakthrough has paved the way for safe, convenient, and effective treatments for obesity. The potential benefits of these drugs may be far broader than weight loss. This summer, a leading biopharmaceutical company reported that its top weight loss drug also reduces major adverse cardiovascular events, such as heart attack, stroke, and cardiovascular death by 20%. Although yet unproven, there also are hopes that these drugs could also treat other diseases, such as Alzheimer’s disease.

Disruption on this scale creates both opportunities and risks, and we are vigilant to both. One way we are participating in the opportunity is through investments in leading biotechnical firms. But we’re also looking into other niches. Demand has been so strong for these drugs that manufacturers have been unable to keep up, leading to significant shortages. Businesses that are alleviating these pressures have a real edge. We maintain positions in companies addressing supply chain bottlenecks, such as those making vials and autoinjectors that contain and deliver weight loss medicine.

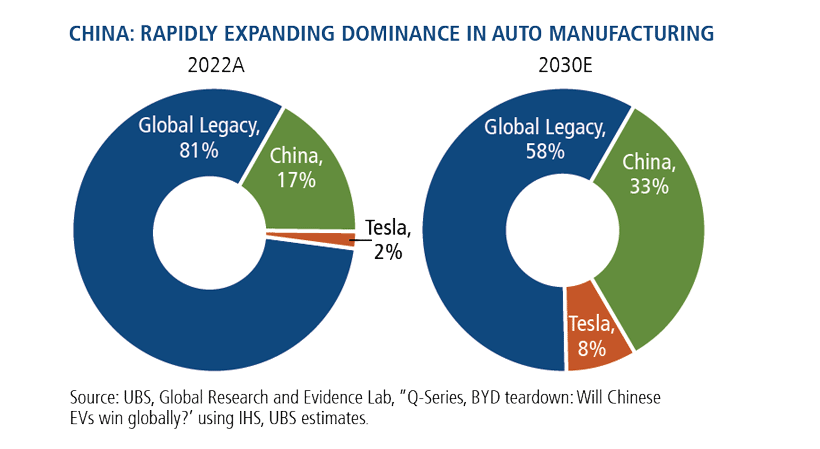

Theme 3: China’s Electric Vehicle Ecosystem

Chinese auto manufacturers are becoming more competitive not only in China but also globally. China already leads the world in electric vehicle (EV) adoption. Chinese companies are at the forefront of EV innovation, with the lowest-cost battery production at the largest scale and are also making significant strides in areas such as autonomous driving, rapid charging, and battery swapping.

We see continued growth potential in China’s electric vehicle ecosystem, with domestic demand supported by tax incentives and China’s slow economic recovery. Chinese EV manufacturers are enjoying tailwinds as local consumers increasingly favor domestic vehicles. Our portfolios have exposure to China EV manufacturers we believe can not only be successful in China but in other parts of the world.

Theme 4: Energy

Global oil demand is likely to remain resilient, with a variety of factors keeping prices high. When energy prices spiked in 2022, the US government released excess inventory from the Strategic Petroleum Reserve (SPR) to help balance the market. The SPR is now at its lowest level since the mid-1980s, so a move by the US to release more oil to offset the recent price spike wouldn’t have the same impact. Additionally, in response to the weaker oil prices seen in the first half of 2023, OPEC+ has reduced its oil output in recent months, causing upward pressure on prices as demand has outpaced supply. Looking further out to the medium term, we are unlikely to see a major rush of new supply coming to market to meet future demand, given underinvestment in oil-and-gas capital expenditures over the past decade.

The flipside of this capital discipline is improved balance sheet health and shareholder returns. We continue to view the sector positively and favor exposure to integrated oil and gas and exploration-and-production companies with direct exposure to underlying commodity price strength. Our portfolios also own equipment and service contractors that stand to benefit from strong activity growth in international and offshore markets.

Higher-Quality Companies for a “Higher-for-Longer” Rate Environment

Calamos Antetokounmpo Sustainable Equities Fund (SROIX)

Jim Madden, CFA, Tony Tursich, CFA, and Beth Williamson

- SROIX’s positioning reflects our belief that a well-diversified portfolio of high-quality companies is advantageously positioned to produce long-term returns.

- We seek high-quality companies that effectively manage nonfinancial and financial risks.

- In an environment of higher interest rates, companies with high debt levels may face added pressure.

After a torrid first half of 2023, stocks took a breather in the third quarter. The large-cap tech-stock domination that propelled the market higher during the first half of the year waned, and the tech sector underperformed the market (as measured by the S&P 500 Index) for the quarter. Energy and communication services were the only sectors within the index that posted positive quarterly returns.

From a capitalization perspective, mega caps continue to dominate the S&P 500 Index, with the market caps of the largest 31 companies in the S&P 500 Index about equal to the combined market caps of the other 469. How fast companies this big can continue to grow is a fair question.

The Calamos Sustainable Equities team has always focused on the advantages of diversification. We believe that holding a well-diversified basket of high-quality stocks for the long term enhances our ability to produce superior returns. Heavy reliance on a small number of stocks or a single sector may produce outsized returns in the short term, but the downside risk, often ignored by investors, is equally large.

While SROIX is well-diversified across industries and sectors, its holdings share important characteristics. Across the portfolio, we have sought high-quality companies that have strong financial metrics and are addressing nonfinancial risks related to governance, ecological impact and human development.

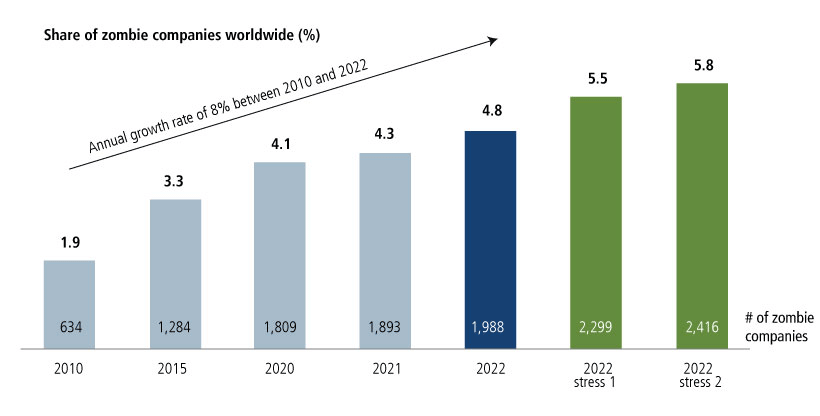

In an environment of higher interest rates, we maintain a focus on identifying and investing in high-quality companies with lower levels of debt than their peers. Although the Fed paused interest rate hikes in September, its language was cautious regarding the timing of future rate cuts. Following more than a decade of essentially free money, it’s important to keep an eye on the effects of higher rates as the “higher for longer” scenario becomes more possible. The graph below shows the increase in “zombie companies” (i.e., companies with operating profits that fall short of their interest expenses).

Avoiding a zombie company apocalypse: SROIX invests in companies with lower debt

Source: Kerney.com, “Dawn of the debt,” September 14, 2023. Stress test 1 represents a 1.5-fold interest rate increase. Stress test 2 represents a 2-fold increase. Increases are applied to individual companies’ existing interest payments.

These “zombies” could soon experience further difficulties. Historically, the economy starts to feel the effect of interest rate increases 18 to 24 months after the date of the first hike. We are now about 18 months out from the first hike in this latest cycle. Against this backdrop, we believe our focus on quality fundamentals will be especially important—both for pursuing returns and managing risks.

Braking (and Not Breaking) the Economy

Calamos High Income Opportunities Fund (CIHYX), Calamos Total Return Bond Fund (CTRIX), Calamos Short-Term Bond Fund (CSTIX)

Matt Freund, CFA, Christian Brobst, and Chuck Carmody, CFA

We believe:

- There is a high level of uncertainty around economic outcomes.

- The growing possibility of future Fed cuts supports the case for increasing portfolio durations across the Calamos fixed-income funds.

- Credit spreads reflect an overly sanguine outlook and we are reducing exposure to credits vulnerable to a cyclical downturn.

Progress on inflation and surprisingly resilient economic growth allowed the Federal Reserve to pause its rate hiking campaign at its September 20 meeting. This pause affords the committee another six weeks to evaluate incoming data. It’s clear the Fed is looking for continued improvement in PCE Core Services (ex-housing). The message stayed the same and was two-fold. First, the Fed is confident a restrictive policy stance has been reached. Second, the central bank stands ready to do more if necessary. Despite this strong reassurance, long-maturity interest rates moved to a 15-year high.

We agree that monetary policy is restrictive at current levels, as evidenced by trailing 12-month inflation (core PCE) below the Fed funds effective rate and real yields on Treasury Inflation-Protected Securities well above 2% across the maturity spectrum. We expect future months and quarters to display some deterrence to consumer and business investment as a reduction in disposable income through higher borrowing costs roll into more areas of economic activity. We are squarely in the “impatiently waiting” phase, looking to ascertain how much economic momentum will be lost from past policy changes. We believe there is still a high level of uncertainty around potential economic outcomes and a recession cannot be dismissed.

We’ve seen fundamentals weaken modestly in levered credit. The traditional high yield market experienced year-over-year declines in both revenue and EBITDA through the end of the second quarter for the first time since 2020. Recall that prior quarter results looked healthier with 7.5% year-over-year growth in EBITDA, but the aggregate results relied heavily on significant strength within the leisure, energy and transportation industries. Although the direction of progress may have changed, aggregate levels of leverage and interest coverage continue to look healthy in our evaluation. We are monitoring the situation closely to determine whether a new trend towards weakness is emerging or whether results are simply becoming more volatile as the instability in input prices, labor costs, and consumer behavior show up in erratic results. Credit spreads in both the investment grade and high yield markets have widened slightly as strong balance sheets and technicals have offset the growing suspicion that results in coming quarters will be weaker.

On the topic of capital access, we believe developing private credit markets have ample capital available to fill the liquidity gap that occurs when banks and other traditional capital sources pull back. These new capital sources, along with low-cost, fixed-rate Covid-era debt, are likely to extend the transmission lag with which the Fed’s monetary policy affects economic activity. Nevertheless, a recession is still a possibility as liquidity conditions continue receding.

Positioning Implications

Recent increases in Treasury yields moved the market into closer harmony with the Fed’s own expectations for its forward rate path. Futures markets now indicate that at least two rate cuts will occur in 2024, down from the five cuts the market had priced in last quarter. Although this feels more measured, we believe rates could eventually reflect a scenario where no rate cuts are priced in for the next calendar year. We have been gradually increasing portfolio durations across strategies in expectation of peak-Fed policy rates and a greater likelihood that the next rate move is a cut. This leaves us with a modestly long benchmark duration in both Calamos Total Return Bond Fund and Calamos Short-Term Bond Fund. The duration of the Calamos High Income Opportunities Fund remains below its benchmark duration, but interest rate sensitivity in the high yield market is a smaller driver of risk and return. This has also led to selective reductions of our leveraged loan positions, although we maintain a significant loan allocation across mandates based on relative value and seniority considerations.

In our estimation, credit spreads reflect an outlook that is too sanguine. We are beginning to see a deterioration in fundamentals within the leveraged finance space. Although it is too early to determine whether this is a wobble or a new trend forming, we are actively reducing exposure to credits we evaluate to be more exposed to a downturn in cyclical activity, credits with weak contingent liquidity or credits with exposure to rapid deterioration of asset value. Based on our fundamentally driven investment philosophy, we believe there are select high yield issuers where investors are being well compensated for associated risks, and we are maintaining allocations in those areas. We are also increasing allocations to securitized structures that offer relative value in comparison to investment grade corporate debt.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here