Since I last wrote about China’s leading sportswear company ANTA Sports Products (OTCPK:ANPDY) in April this year, its stock has declined by 10.7%, which is at odds with my Buy rating on it. In fact, it has seen a largely weakening trend since.

I still believe, however, that the fundamental story is unchanged, if not improved now, as the prospects for China look better now, its own performance continues to be strong and its market multiples have become more competitive.

Improved prospects for China

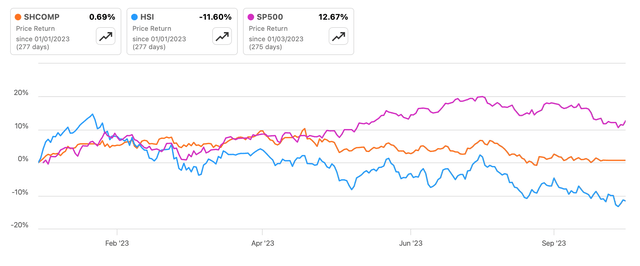

In understanding why ANTA Sports Products has softened in the recent past, the backdrop of China plays an important part. China’s stock markets have had a challenging year so far, with the Shanghai Composite (SHCOMP) essentially flat year-to-date [YTD] and the Hang Seng (HSI) actually declining. This compares unfavourably to a 13% rise in the S&P 500 (SP500) during this time (see chart below).

Index Returns (Source: Seeking Alpha)

Muted investor confidence had a good basis, of course. The post-lockdown Chinese economy didn’t quite accelerate as fast as expected, with the industrial sector in general and the real estate sector causing concern. Continued stress between the US and China and limited support to the economy from authorities added to the concerns.

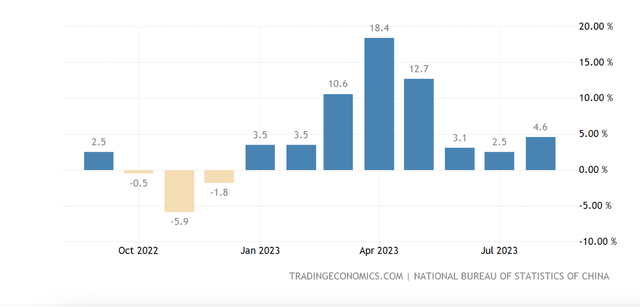

But things appear to be getting back on track, with China’s economy having “bottomed out” as the new catchphrase for it. With a series of measures by the Chinese government to encourage the economy, signs of improvement are already visible across indicators like retail sales and industrial production. The outlook for the economy is getting upgraded too.

All of this, and specifically, improving retail sales are positive for the ANTA Sports Products stock, which has seen a softening despite robust financial performance, as discussed next.

Retail Sales (Source: Trading Economics)

Healthy financials

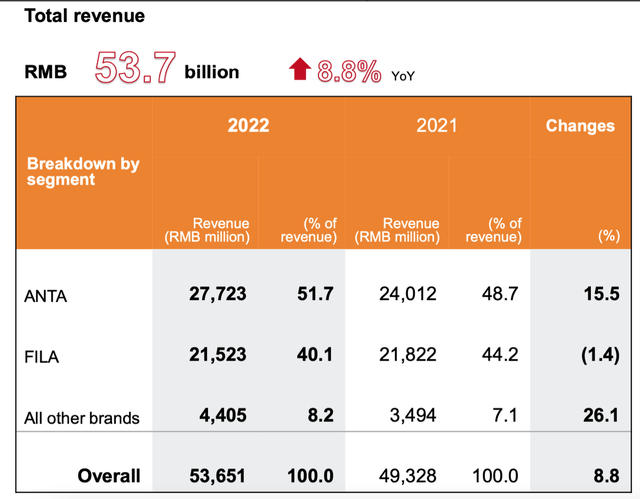

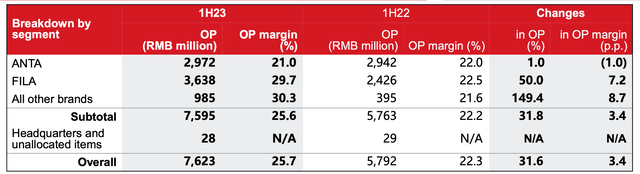

When I last wrote, the latest numbers available were for the full year 2022, during which the company had seen good performance. Its revenues had risen by 8.8%, primarily as the ANTA brand raced ahead. The operating margin was notable too, at 20.9%, ahead of its peers.

Source: ANTA Sports Products

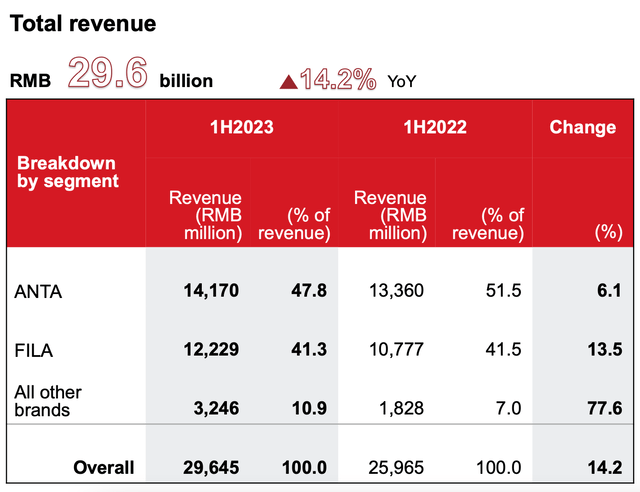

It continued to grow at a fast clip in the first half of the year (H1, 2023) as well. Investors were clearly happy with its performance, as the numbers released in August resulted in a 7.5% increase in its price on the day. Despite some softening in China’s retail sales growth towards the end of the first half of the year, the company actually came out ahead, with a 14.2% year-on-year (YoY) revenue growth. The company’s operating margin strengthened further to 25.7% during H1 2023, and its gross margin improved too.

FILA’s performance was particularly strong both in terms of revenues and margins (see tables below) on a weak base year, as it was disproportionately impacted by the pandemic and global raw material inflation. The growth for ANTA softened, however, after strong results last year.

Source: ANTA Sports Products Source: ANTA Sports Products

Improved market multiples

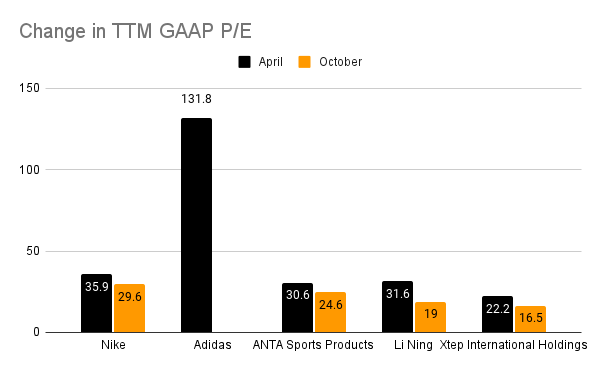

With better earnings and a weak price trend, ANTA Sports Products’ trailing twelve months [TTM] price-to-earnings (P/E) ratio also looks more favourable in two respects. One, it has declined to 24.6x from 30.6x. And second, it’s also more in line with its past decade’s average figure of 25.7x.

Next, let’s look at its forward P/E ratio, which I estimated with the assumption that both revenue growth and net margin, at 16%, remain constant in H2 2023 from H1 2023. The resulting ratio, at 22.5x, is also competitive compared to the market leaders in China’s sportswear market, NIKE (NKE) and adidas (OTCQX:ADDYY). While Nike has a forward P/E of 25.7x, that for Adidas is at 24.9x.

On the downside, the P/E is still significantly higher than that for the consumer discretionary sector, which is at 14.9x. Also, it’s still higher relative to its Chinese peers even now (see chart below), the same as the last I checked. There’s some justification for this premium, though. ANTA has maintained its lead among Chinese sportswear manufacturers like Li Ning (OTCPK:LNNGY) and Xtep International Holdings (OTCPK:XTEPY) and has higher margins as well.

Source: Seeking Alpha

Good long-term returns

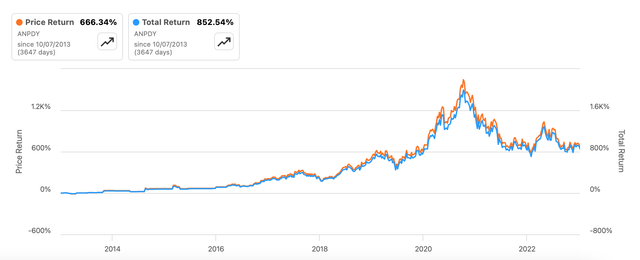

The long-term returns on ANPDY have declined significantly from 1,400% since April to 666%, but even with the decline, it’s still quite a healthy number. With a more positive outlook on China now, there’s a good chance that it can see a further uptick. In any case, if its past and current financials are anything to go by, there’s little to halt its increase over time. And these are just the price returns.

Returns (Source: Seeking Alpha)

Total returns are even higher, at 852.5% over the last 10 years. The company’s TTM dividend yield is muted, at 1.8%, but there’s something to be said for the fact that it has paid dividends consistently over the past 14 years. It has also grown its dividends over the past three years, and going by its improved earnings this year, the trend may well continue.

What next?

Despite a smaller than expected recovery post lockdowns in the Chinese economy, ANTA Sports Products has continued to race ahead with strong results in H1 2023. These numbers are even more encouraging as the prospects for China now look better, which is already showing up in the latest retail sales figures. This could imply continued, if not accelerated, demand for the company’s products.

Even if it were to grow at the same rate as seen in H1 2023 however, my forward estimates show that ANPDY’s P/E ratio looks competitive compared to peers. In any case, its TTM P/E looks good anyway. Its long-term returns and sustained dividend payouts also make a continued case for the stock. With it having fallen since I last checked, the case for it has become stronger. I reiterate the Buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here