Natural Gas Services Group, Inc. (NYSE:NGS) recently delivered double digit net sales growth, and management expects even more improvement coming. I believe that further diversification of its compressors, geographical expansion, outside the Permian Basin, and lower net leverage could bring further stock price increases. There are a number of risks coming from supply chain issues to crude price volatility or covenant agreement, however I believe that the company is undervalued.

Natural Gas Services

Natural Gas Services is a natural gas and treatment equipment supplier company located in Texas. The company designs, manufactures, sells, rents, and distributes gas compressors and flare systems to other manufacturing factories. Customers are primarily participants in natural gas exploration and production, which are concentrated almost 55% over the Permian Basin, although they also extend into Oklahoma and New Mexico.

The operations of this company are divided into three operating segments, which are the rental segment, the sales and service segment, and the administration and maintenance segment. The first of these segments is the one that has brought the most operational benefits to the company as it, through contracts with a minimum term of 24 months, introduces its products into the productive and extractive facilities of its clients by charging a fee. Additionally, clients obtain great benefits from renting this equipment since they achieve a significant reduction in operating costs and higher productive margins in terms of the production and understanding of natural gas. Natural gas Services is responsible for the maintenance and installation of all this rented equipment.

The sales segment is responsible for directing the company’s production, which includes gas compressor parts and equipment as well as complete compression equipment.

Management Expects Further Improvement In The Coming Years, And Analysts Reported Beneficial Market Expectations

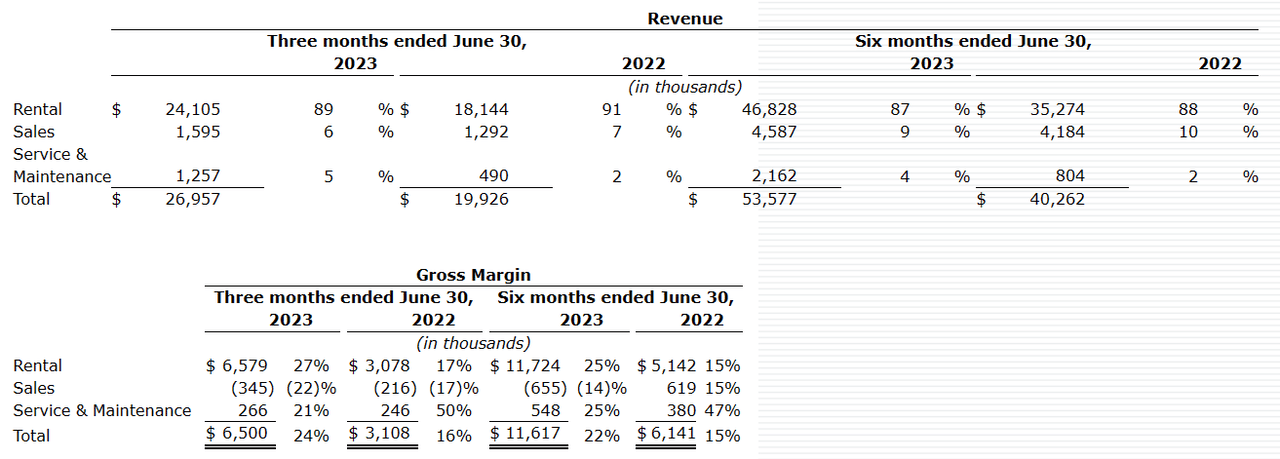

From 2021 to 2022, the company managed to increase its revenues by a double digit, mainly supported by increases in its equipment retail activities. I believe that the figures are quite beneficial in line with the recent comments from management, expecting further improvement.

We are starting to see the results of our 2023 capital program in our revenues, margins and bottom lines. The overall environment in our industry continues to be positive and we anticipate further improvement. Source: Quarterly Report

Source: Quarterly Report

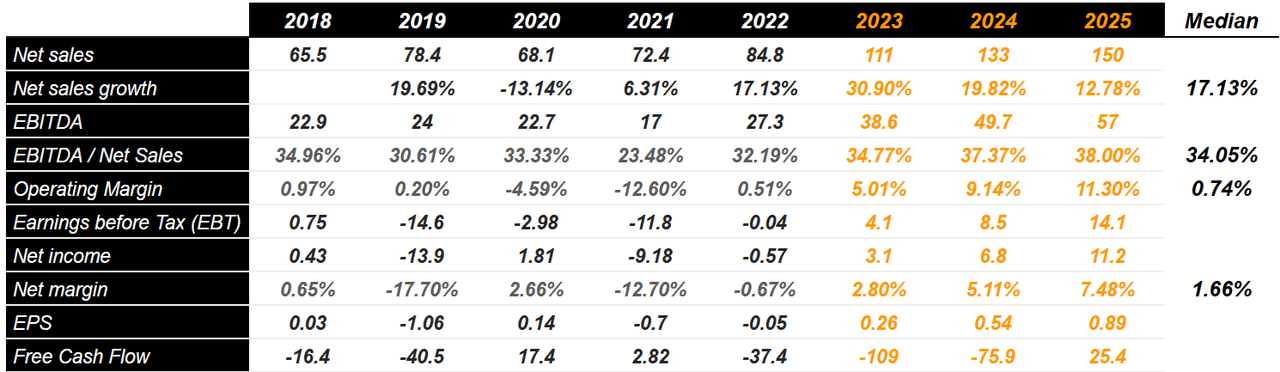

I believe that most analysts out there expect a beneficial future for Natural Gas Services. My expectations are not far from those of other financial analysts, so I think that readers may want to have a look. Expected net sales growth is expected to be close to 30%-12% in 2023, 2024, and 2025, with 2025 EBITDA of $57 million, and 2025 EBITDA margin of 38%. Besides, with growing net income margin, 2025 net income would stand at about $11 million, with 2025 EPS close to $0.89 per share. Finally, 2025 FCF would stand at $25.4 million.

Source: S&P

Balance Sheet Assessment: There Are Some Risks From The Total Amount Debt

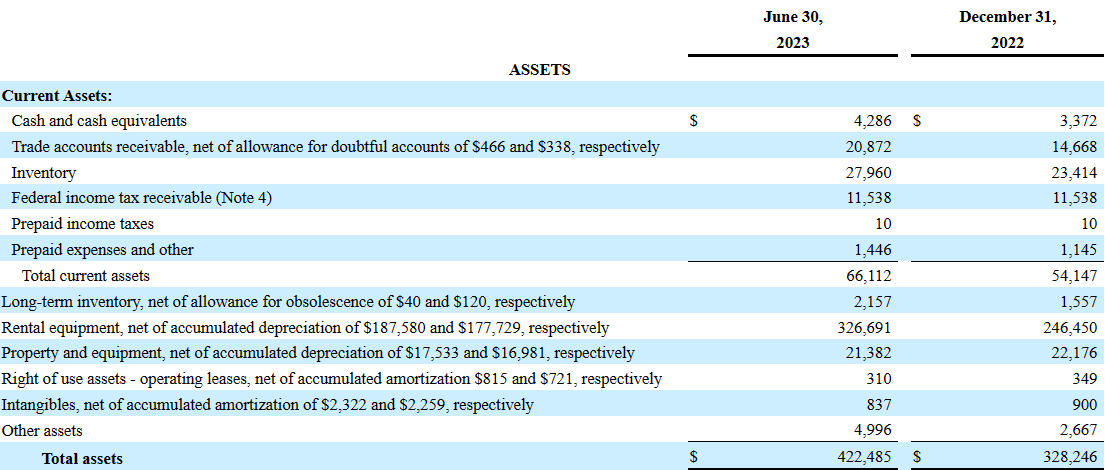

As of June 30, 2023, the company did not seem to report a significant amount of liquidity. Current assets included cash and cash equivalents worth $4 million, trade accounts receivable of $20 million, and inventory of $27 million. Total current assets stood at $66 million, a bit below the total amount of current liabilities.

With total assets of close to $422 million, the asset/liability ratio is more than 2x, so I believe that the balance sheet appears quite solid. With that, investors may want to have a close look at the total amount of long term debt, which represents close to one-third of the total amount of rental equipment.

Source: 10-Q

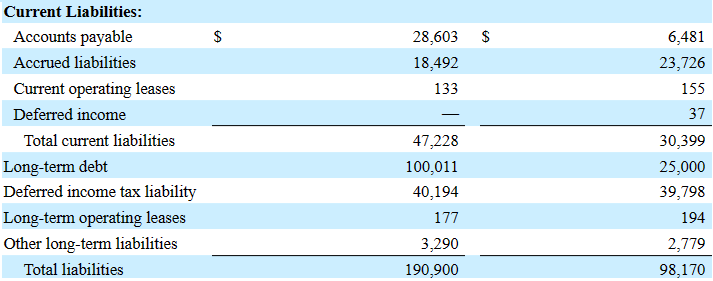

Long term liabilities include debt of $100 million, deferred income tax of $40 million, and other long-term liabilities of $3.2 million. Finally, total liabilities are equal to $190 million.

Source: 10-Q

Given the total amount of debt, I did study carefully the interest rates being paid. In a credit agreement signed recently, the company noted a weighted average interest rate of 7.32%. I used figures close to the interest rate being paid for assuming the cost of capital in my financial model.

At December 31, 2022, we had $25.0 million outstanding under the New Credit Agreement with a weighted average interest rate of 7.32%. On December 31, 2022, we had $5 million of availability under the New Credit Agreement. Source: 10-k

The company also signed several credit agreements that depend on the leverage ratio being reported and the SOFR rate. Finally, it is also worth noting that Natural Gas Services did sign several covenant agreements that may restrict the number of activities that the company may execute. As a result, acquisition of large targets may not be possible.

The Applicable Margin is determined based upon the leverage ratio as set forth in the most recent compliance certificate received by the Lender for each fiscal quarter from time to time pursuant to the Amended and Restated Credit Agreement. Depending on the leverage ratio, the Applicable Margin can be 2.00% to 2.75% for Base Rate Loans (as defined in the Amended and Restated Credit Agreement) and 3% to 3.75% for Term SOFR Loans and for requested letters of credit. Source: 10-k

In addition, we are subject to certain financial covenants in the Amended and Restated Credit Agreement that require us to maintain a leverage ratio, as defined, lesser than or equal to 3.50 to 1.00 as of the last day of each fiscal quarter ending on or prior to December 31, 2024 and 3.25 to 1.00 for the fiscal quarter ending March 31, 2025. Source: 10-k

With regard to the current leverage ratio, I believe that it is worth noting that in the last quarter, management reported a ratio of close to 2.53. I believe that the debt appears quite under control as the company appears to be in compliance with all the covenants of the credit agreement.

Outstanding debt on our revolving credit facility as of June 30, 2023 was $100 million. Our leverage ratio at June 30, 2023 was 2.53 and our fixed charge coverage ratio was 4.17. The company is in compliance with all terms, conditions and covenants of the credit agreement. Source: Quarterly Report

FCF Catalyst: Larger Compressors, And Geographical Expansion

Natural Services Group has a long-term strategy aimed at increasing profits and improving operating margins thanks to further expansion of the rental segment, which includes the production of large-sized compressors. Under my base case scenario, I assumed that a large compressor may bring larger FCF margins and stock price increases.

I also assumed that the geographical expansion and the expansion of operations towards new areas form one of the channels through which Natural Gas Services could find business growth.

We will continue to expand our operations in existing areas, as well as pursue focused expansion into new geographic regions as opportunities are identified. Our largest rental area is the Permian Basin (approximately 55.6% of rental revenues in 2022), where we have continued to gain market share and believe we have the most expansion opportunities going forward. Source: 10-k

A Diversified Offering Of Compressors Will Most Likely Bring Lower Net Sales Volatility, And May Help Fight Competition.

Under my financial model, I assumed that Natural Gas Services would be able to extend its offering, and the portfolio may become even more diversified. As a result, a large number of products may bring even more clients with different applications, which may lower net sales volatility. Management also noted that more products will most likely enhance relationships with clients as the company may be able to satisfy widely varying pressure, volume, and production conditions.

A diversified compression product line helps us compete by being able to satisfy widely varying pressure, volume and production conditions that customers encounter. Source: 10-k

Acquisitions Could Happen, However Management May Have To Respect Its Covenants

Furthermore, inorganic growth is part of the growth strategy. However, I did not assume significant inorganic growth, mainly because management has not bought many targets in the past. In this regard, note the previous increases in goodwill. Finally, I believe that the covenant agreements signed with debt inventors may lower the potential for acquisitions.

Source: Ycharts

Financial Model

For the assessment of my financial mode, I took into account previous cash flow statements, mainly changes in working capital, changes in receivables, inventories, and payables as well as capex, net income, and previous FCFs. I believe that my figures are quite conservative. However, I invite readers to have a look at previous financial figures, and form their own opinion.

Source: Ycharts

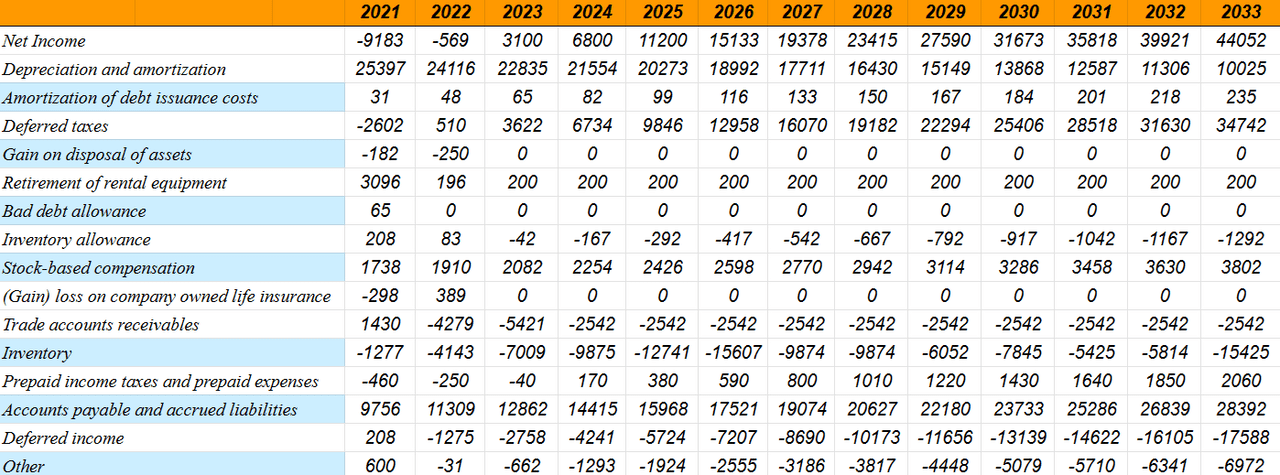

My financial model includes 2033 net income close to $44 million and 2033 depreciation and amortization of close to $10 million, but no amortization of debt issuance costs, no gain on disposal of assets, and no gain on retirement of rental equipment.

Besides, with a 2033 inventory allowance of -$2 million, stock-based compensation of about $3 million, and changes in trade accounts receivables of close to -$3 million, my model also includes changes in inventory of about -$16 million. I also assumed prepaid income taxes and prepaid expenses of $2 million.

Source: My Cash Flow Expectations

Finally, assuming changes in accounts payable and accrued liabilities close to $28 million, deferred income close to -$18 million, and capex of -$15 million, 2033 FCF would be $64 million.

Source: My Cash Flow Expectations

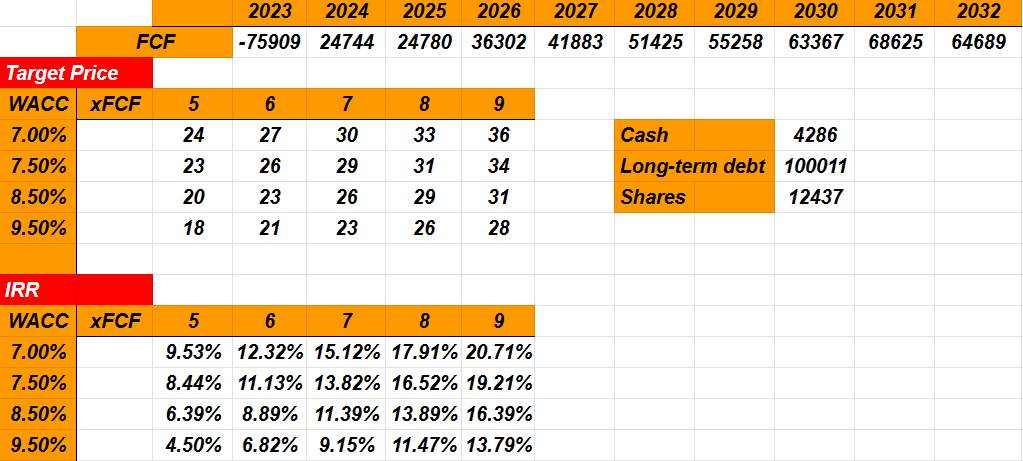

My results included FCF going from $24 million in 2024 to about $64 million in 2032. Additionally, I assumed exit multiples close to 5x-9x, which appear, in my view, quite conservative and in line with the assumptions of other analysts.

Besides, if we also include cost of capital around 7% and 9.5%, the implied forecast would stand at about $18-$36, with a median around $23 and $29 per share. My model also implies an internal rate of return around 4.5% and 20%. In all the cases, the current stock valuation appears significantly smaller than my price forecasts. I do believe that the company is undervalued.

Source: My Cash Flow Expectations

Competitors

The equipment industry for compression gases is highly competitive and is made up of a few competitors that aim to concentrate market portions in the areas of greatest activity. For each region in this sense, there is a high degree of consolidation in the market since the relationships between clients and suppliers are very close.

Risks

One of the risks for this company is the concentration it has both geographically and on sales to its clients. Along with this, the high degree of competition and the almost total dependence on the activity of the gas and extraction sector are risks to be taken into account within this analysis. To this we must add the volatility in oil prices and how this translates to the company’s pricing strategy, consequently to its operating margins. In the same way, the company’s ability to manage the growth of its rental segment as well as to develop new contracts in the short term is essential to comply with its strategy of increasing profits.

Ultimately, it is important to highlight that the company maintains high operating costs, and likewise has debt with short-term obligations, and the combination of these factors together could generate complications.

Conclusion

Natural Gas Services recently delivered double digit sales growth, and management expects even more improving figures. In my view, if the company brings more large-sized compressors, expands into new geographic regions outside the Permian Basin, and offers a more diversified portfolio of compressors, we can expect FCF growth. There are obvious risks from the total amount of debt, the covenant agreements, or changes in the crude oil price, however I believe that the company appears quite undervalued.

Read the full article here