A Quick Take On Agiliti

Agiliti, Inc. (NYSE:AGTI) sells medical and healthcare equipment products and maintenance services in the United States.

I previously wrote about Agiliti with a Neutral Hold outlook.

Deteriorating fundamentals and turnover at the CEO level lead me to question the firm’s leadership selection capabilities and near-term prospects.

My outlook on AGTI in the near term is Bearish [Sell].

Agiliti Overview And Market

Minnesota-based Agiliti was founded to provide a range of medical and healthcare equipment products and related services to the U.S. healthcare system.

The firm is led by Chief Executive Officer Tom Leonard, who was previously CEO of Agiliti from 2015 through March 2023.

The company’s main service offerings include:

-

Onsite managed services

-

Clinical engineering services

-

Equipment solutions.

The firm’s customers include thousands of hospitals, delivery networks and alternate site medical care providers, both privately-held and government-owned.

Market research firm Prescient Strategic Intelligence estimated the repair & maintenance market size at a much higher level, at $8.3 billion in 2019 and expected to grow at a CAGR of 9.2% from 2020 to 2030.

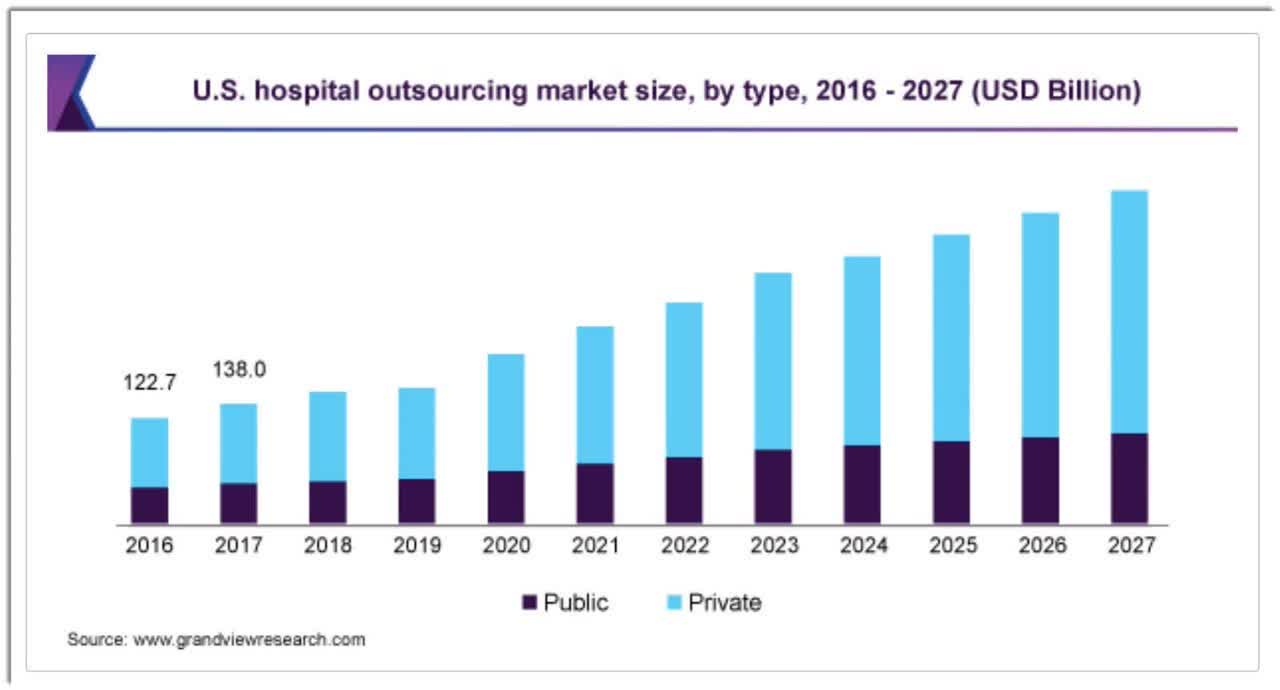

Grand View Research estimated the global hospital outsourcing market size at $271 billion in 2019 and expects it to grow at a CAGR of 10.4% from 2020 to 2027.

Below is a chart showing the historical and expected future growth of the U.S. hospital outsourcing services market:

Grand View Research

Major competitive or other industry participants include:

-

Allscripts

-

Cerner

-

The Allure Group

-

Integrated Medical Transport

-

Sodexo

-

Aramark

-

LogistiCare Solutions

-

Flatworld Solutions

-

Alere

-

ABM Industries

Agiliti’s Recent Financial Trends

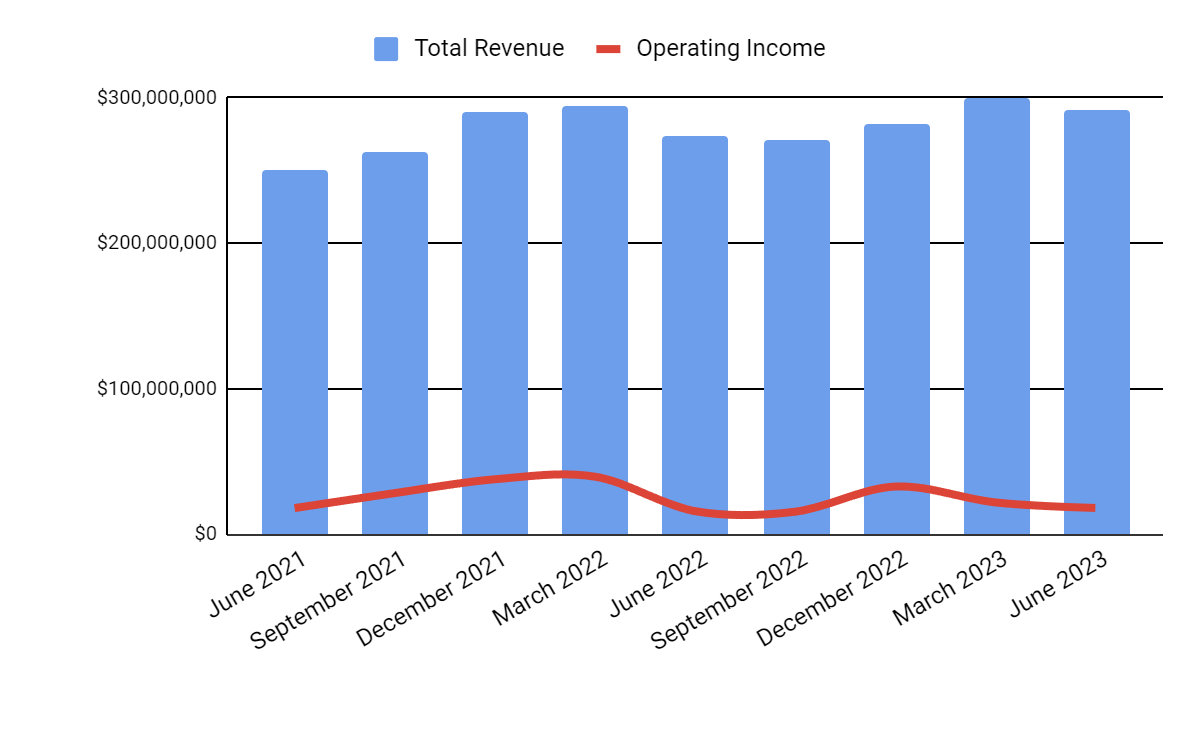

Total revenue by quarter has continued to grow subject to seasonal factors; Operating income by quarter has varied within a range:

Seeking Alpha

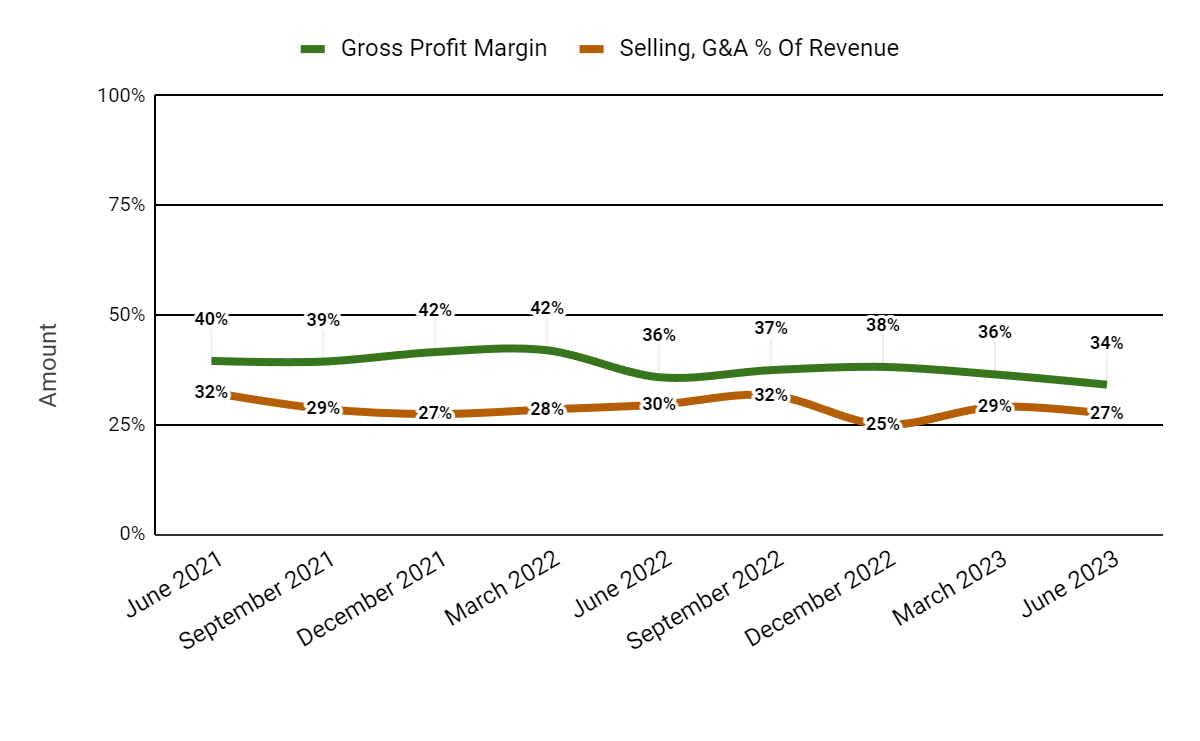

Gross profit margin by quarter has trended lower in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter have varied within a narrow range recently:

Seeking Alpha

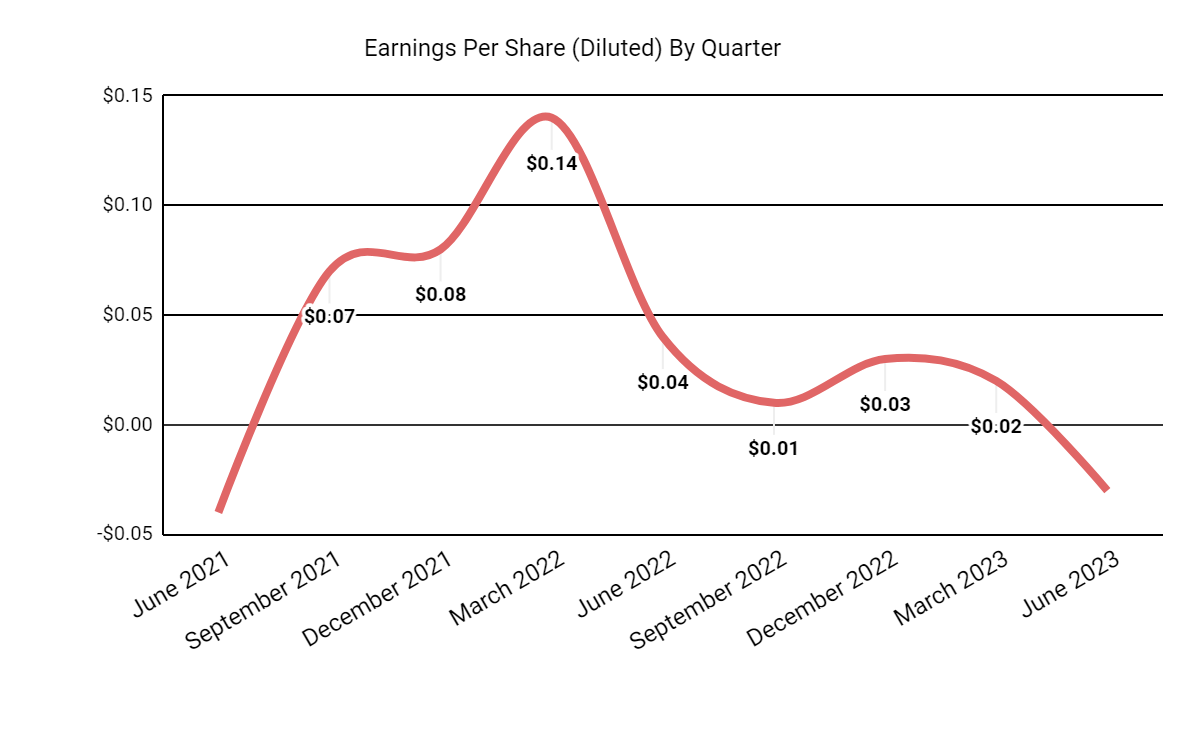

Earnings per share (Diluted) have dropped substantially and have turned negative recently:

Seeking Alpha

(All data in the above charts is GAAP.)

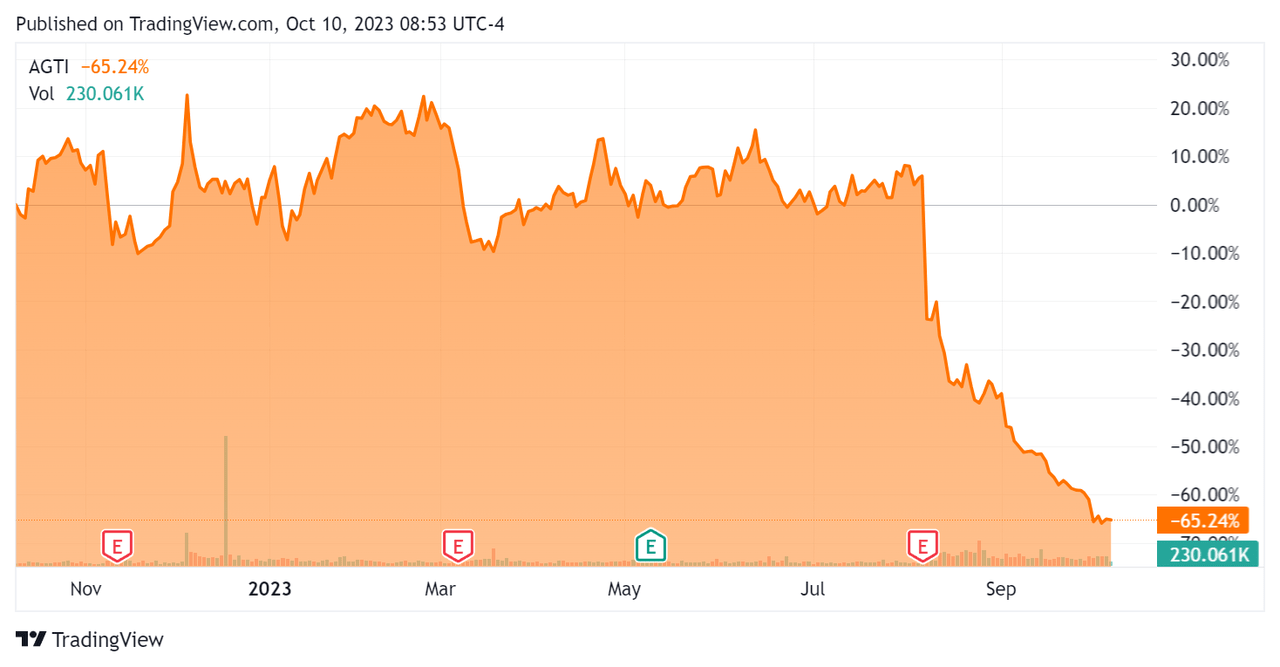

In the past 12 months, AGTI’s stock price has fallen 65.24%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $13.9 million in cash, equivalents and trading asset securities and $1.1 billion in total debt, all of which was long-term.

Over the trailing twelve months, free cash flow was $88.0 million, during which capital expenditures were $93.1 million. The company paid $19.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Agiliti

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.7 |

|

Enterprise Value / EBITDA |

7.5 |

|

Price / Sales |

0.7 |

|

Revenue Growth Rate |

2.0% |

|

Net Income Margin |

38.0% |

|

EBITDA % |

22.7% |

|

Market Capitalization |

$759,030,000 |

|

Enterprise Value |

$1,940,000,000 |

|

Operating Cash Flow |

$181,060,000 |

|

Earnings Per Share (Fully Diluted) |

$0.03 |

|

Free Cash Flow Per Share |

$0.66 |

(Source – Seeking Alpha.)

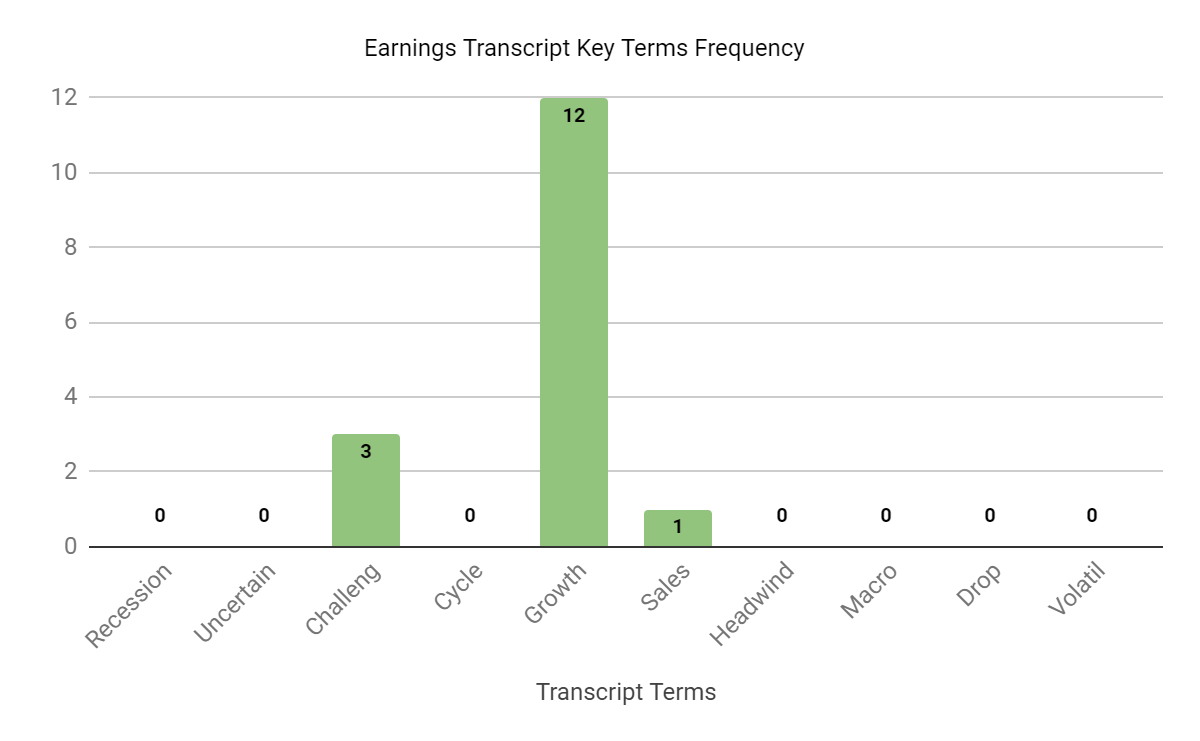

Sentiment Analysis

The chart below shows the frequency of certain keywords in the most recent earnings conference call:

Seeking Alpha

Analysts asked leadership about equipment rental segment dynamics and lower EBITDA margins.

Management responded that lower equipment rental utilization was offset by other business uptrends and expects that rental activity will increase over time.

Lower EBITDA margins were due to reduced rental activity and onboarding of new customers, which tends to lower margins initially.

Commentary On Agiliti

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management’s prepared remarks highlighted the longer-term nature of new deals, necessitating higher upfront servicing costs leading to a longer ramp toward profitability.

The company’s PNR business exhibited slowing activity “due to reduced demand that resulted from the significant medical equipment purchases” made by its customers in recent years.

Agiliti also won contracts from two large ASC franchises for “services including clinical engineering, surgical equipment repair and surgical laser rental.”

Total revenue for Q2 2023 rose by 6.2% year-over-year, while gross profit margin fell by 1.7%.

The company’s employee retention “has remained steady in many job categories.”

Selling and G&A expenses as a percentage of revenue dropped 2.1% YoY, and operating income rose by 13.8%.

The company’s financial position is concerning, with limited liquidity, high debt, but strong positive free cash flow.

Looking ahead, revenue growth for the full year 2023 is expected to be only 4.3% over that of 2022.

If achieved, this would represent a drop in revenue growth rate versus 2022’s growth rate of about 8% over 2021.

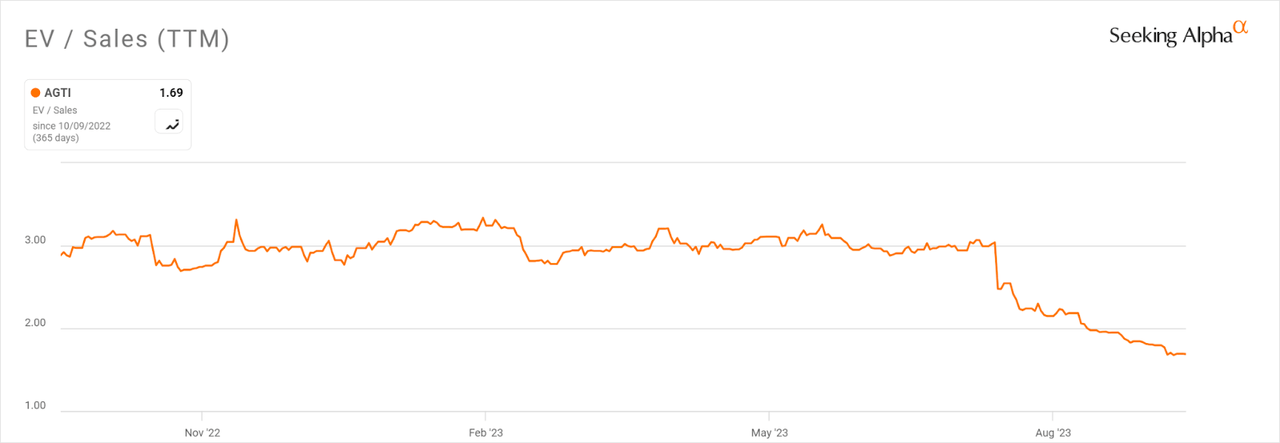

In the past twelve months, the firm’s EV/Sales valuation multiple has fallen by 41%, as the chart from Seeking Alpha shows below:

Seeking Alpha

On October 2, the firm replaced CEO Boehning, whom it appointed on January 9, 2023, with previous CEO Tom Leonard.

With Leonard back in the driver’s seat after just retiring months earlier, we have to wonder how long the company will continue until a search for a new CEO is started.

Uncertain leadership and a weak revenue outlook make me question the firm’s prospects in the near term.

Accordingly, I’m Bearish on AGTI [Sell] for the time being.

Read the full article here