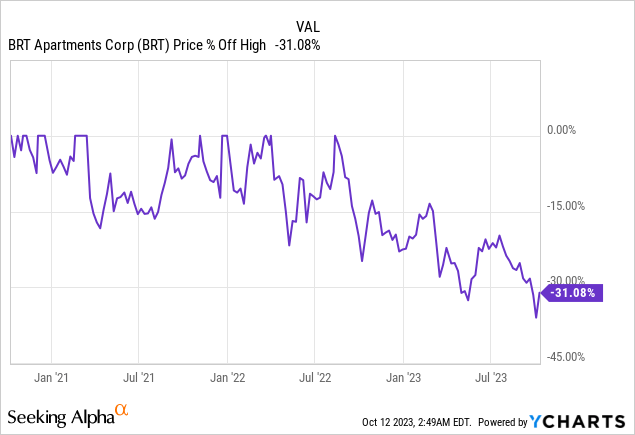

BRT Apartments Corp (NYSE:BRT) is a small-cap residential REIT that focuses on apartments as the name implies. The stock is down 31% from recent highs and it might be approaching a compelling valuation at the current levels for income investors with long-term focus.

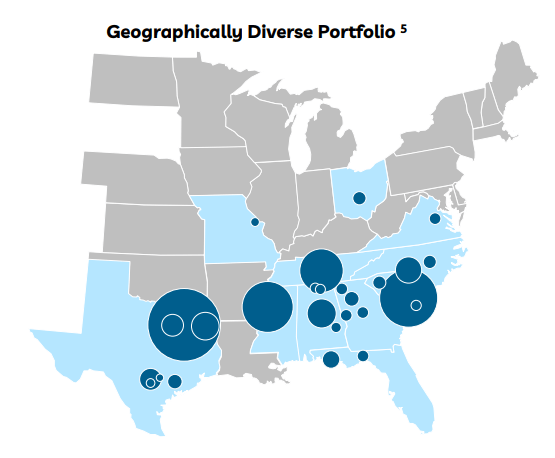

The company owns and operates a total of 33 properties and close to 9 thousand apartment units mostly located in the region called the Sun Belt (southeast of the US). This region has certain advantages such as low cost of living, fast growing economy, nice weather almost all year long (exception being hurricanes), generally low level of government regulations (some call it “business friendly”), higher rate of population growth and relatively low rates of unemployment. BRT currently enjoys an occupancy rate of 96% and collects an average rent of $1,215.

BRT Geographical Distribution (BRT)

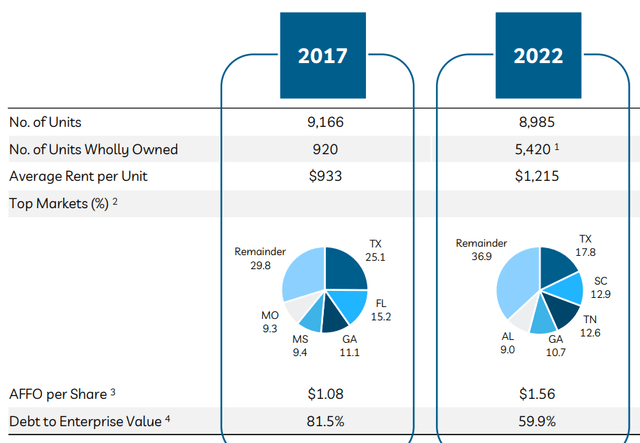

The company has been in a transformation mode since 2017 as it started to look at all its existing properties and shifted its focus towards higher performing properties and started to offload some low performing properties. This accomplished two things for the company. First, its average performance and return-on-investment got better. Second, its debt and leverage ratio also dropped significantly. Notice that the company’s total number of units actually fell between 2017 and 2022 but it’s wholly owned units multiplied. Also its AFFO (Adjusted Funds From Operations) per share rose from $1.08 to $1.56 and its debt-to-enterprise leverage dropped from 81.5% to 59.9%. The company would like to keep this number below 60% in the long term and this is a fairly conservative goal.

BRT 2017-2022 Transition (BRT)

The company seeks growth through strategically planned acquisitions. It focuses on buying properties that are located in high-growth areas (both in terms of population growth and economic growth), low level of unemployment, cheap property values and 90% or more occupation rate. Once the company acquires a property, it makes necessary updates and upgrades to the property so that it can maximize its return on investment.

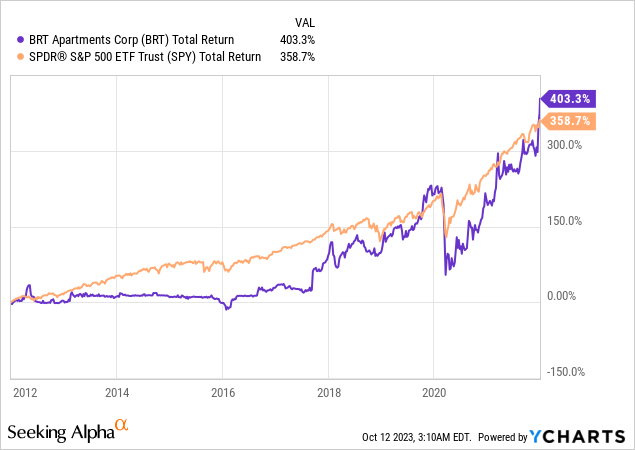

Even though the company’s share price has been underperforming recently, this hasn’t always been the case. In the last 2 years almost all REIT stocks got decimated because of rising rate environment and this created a buying opportunity for those REITs that offer higher quality. If you look at the 10-year period between 2012 and 2022 this stock actually outperformed S&P 500 (SPY) in total returns which includes dividends. The company did a fine job of creating value for investors over the years and it could continue to do so again once this difficult period for REITs ends.

If you had bought $10k worth of the stock 5 years ago and held until today while reinvesting dividends you would be generating about $1,300 annually now which is a 13% yield on your original investment. Keep in mind that there has been times in the past when the company had to cut its dividends significantly and there is no guarantee that it won’t happen again.

BRT Income Growth (Portfolio Visualizer)

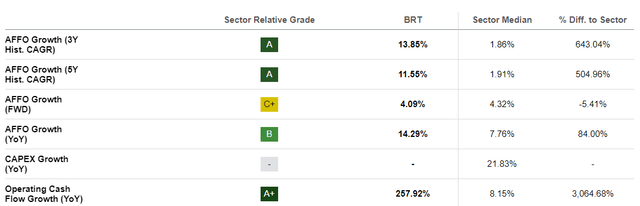

Even in this difficult environment, if you look beyond the company’s stock price, the company’s performance is actually quite impressive. In the last 3 years the company posted an annualized AFFO growth rate of 13.85% and in the last 5 years its AFFO growth rate came at an annualized rate of 11.55% as compared to its sector median which came in single digits. The company was also able to grow its operating cash flow at a rate much higher than its sector average.

BRT Growth Figures (Seeking Alpha)

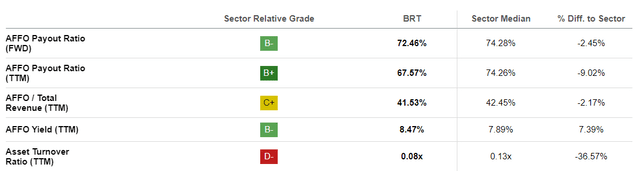

The stock currently has a dividend yield close to 6% and this yield seems to be somewhat sustainable. The company’s current payout ratio is 72.5% which is slightly below sector average. What this means is that the company pays 72.5 cents in dividends for each $1 it generates in AFFO. Typically you want this number to be below 1 because higher numbers would indicate that the company is distributing more than it’s earnings and signals that the dividend may not be sustainable which usually means there will be a cut or elimination of the dividend unless the company grows its earnings. Legally speaking a REIT has to distribute 90% or more of its net income to investors in dividends in order to keep their REIT status but most REITs will use AFFO as their earnings metric which may be different than their EPS, which is why they can get away with paying less than 90% of their earnings in dividends and still keep their REIT status.

BRT Payout Ratios (Seeking Alpha)

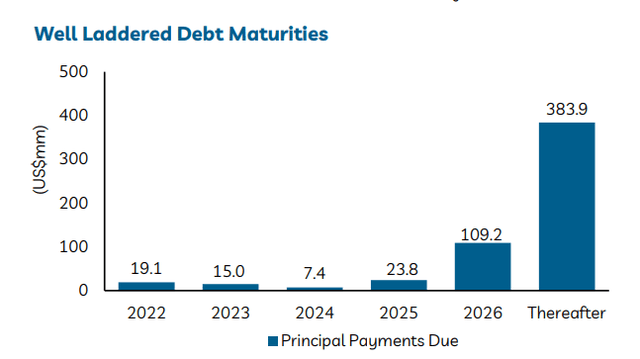

The company has some debt (as almost all REITs do) and this is normal when operating in real estate. The good news is that most of its debt isn’t due until at least 2026. The bad news is that a good portion of the company’s debt is in adjustable rate which means there is a real risk that the company’s debt servicing can become significantly more expensive if yields keep rising the way they have been lately.

BRT Debt Maturity (BRT)

The possibility of rising interest rates is probably the biggest risk for investors of this company. The Fed wants to keep rates higher for longer in order to battle inflation and keep it from making a comeback and we’ve seen mortgage rates climb above 7% for the first time since 2007. Most REITs are already down 30% or more from their recent highs so one could say that this issue could be already “priced in” but it’s impossible to tell. Investors with long-term focus should not worry too much about short term stock fluctuations except perhaps see them as an opportunity to add more shares at cheaper prices to boost their long term income.

One could also say that the company could benefit from the current environment in two ways. First, high inflation allows the company to raise its rent prices and increase its earnings. This could also help the company “inflate its debt away” over time as its debt level will look smaller and smaller in comparison to how fast prices are rising. Second, high interest rates make it difficult for apartment-dwellers to buy a house so it ensures that they stay in apartments. Roughly two thirds of Americans are home-owners and many of them bought their homes (or refinanced them) when interest rates were much lower so a lot of current home owners will sit tight and inventory of homes will be short. This will unfortunately force some first-time buyers to stay in apartments but it’s not so unfortunate for companies like BRT.

All in all, BRT seems like a good investment for long term investors who’d like to add an apartment REIT to their portfolios to boost their income. The REIT bear market we’ve been seeing in the last 2 years made this stock 30% cheaper even though the company’s fundamentals didn’t change much (except getting a bit better). I’d be a buyer at the current price but I’d only suggest you to buy if you plan on holding for the long term. This is not a good stock for short-term trading.

Read the full article here