A Quick Take On PlayAGS

PlayAGS, Inc. (NYSE:AGS) provides electronic gaming machines and online gaming to the gaming industry in the U.S. and overseas.

I previously wrote about AGS with a Neutral Hold outlook.

The firm has seen robust demand for some of its new products and may see growth in its installed base with new casino openings and expansions.

However, my current cash flow analysis suggests PlayAGS, Inc. stock may be fully valued here, so I reiterate my previous Neutral [Hold] outlook.

PlayAGS Overview And Market

Las Vegas-based PlayAGS was founded to offer electronic slot machines, table games and equipment, and social online casinos for B2B and B2C.

The firm is led by President and CEO David Lopez, who has been with the AGS since 2014. Lopez was previously the President of Global Cash Access from 2012 – 2014 and COO of Shuffle Master from 1998 – 2011.

PlayAGS offers products in three segments:

-

Table Products

-

Interactive Social Casino Games

-

Electronic Gaming Machines [EGM].

The company’s geographic focus has primarily been North America, although it has employees around the globe, including Australia, Israel, and Mexico.

According to a 2022 market research report by Data Bridge Market Research, the worldwide Casino Gaming Equipment market size was an estimated $7.1 billion in 2021 and is forecast to reach $11.1 billion by 2029.

This represents a projected CAGR (Compound Annual Growth Rate) of 5.5% during the period of 2022 to 2029.

The primary reasons driving the market’s growth are the growing popularity of reconfigurable electronic gaming machines and an increase in casino gaming worldwide.

Also, EGMs are gaining popularity in modern casinos, due to being user-friendly and easily upgradeable to different games and win rates.

A key market challenge is the availability of substitutes such as lotteries, horse race betting, sports betting, and casino games.

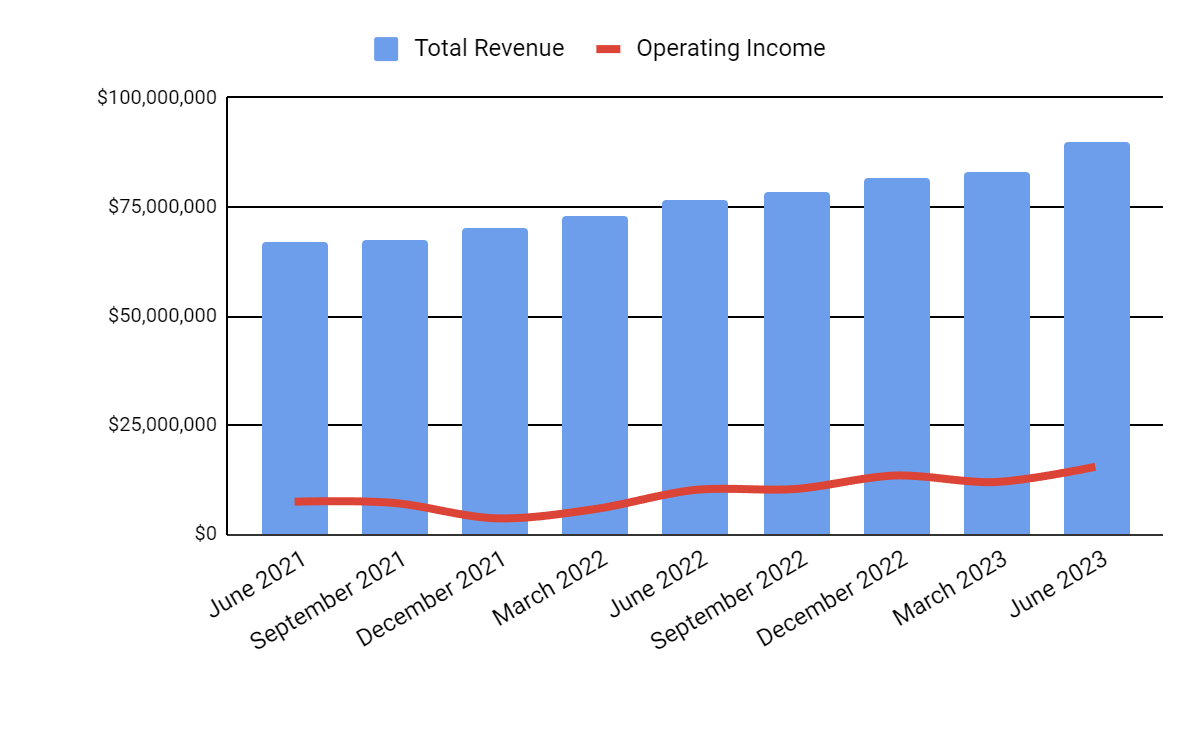

PlayAGS’ Recent Financial Trends

Total revenue by quarter has continued to grow; Operating income by quarter has trended higher recently:

Seeking Alpha

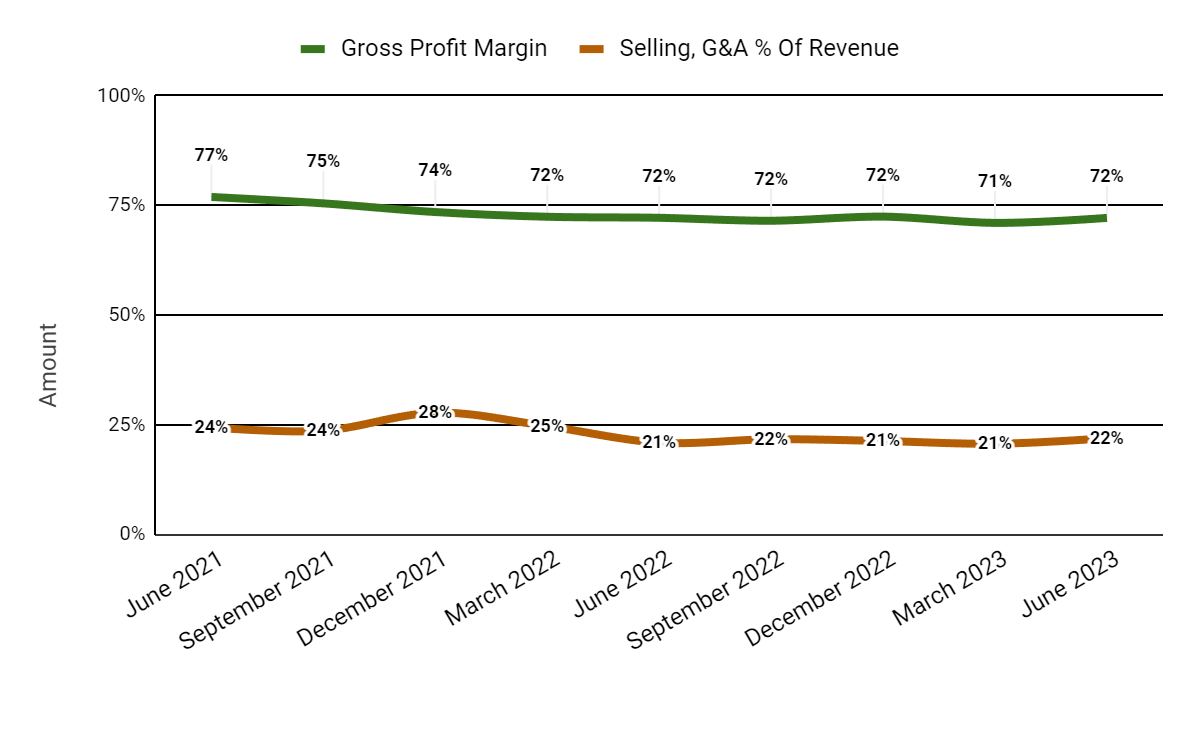

Gross profit margin by quarter has been trending lower; Selling and G&A expenses as a percentage of total revenue by quarter have varied within a narrow range.

Seeking Alpha

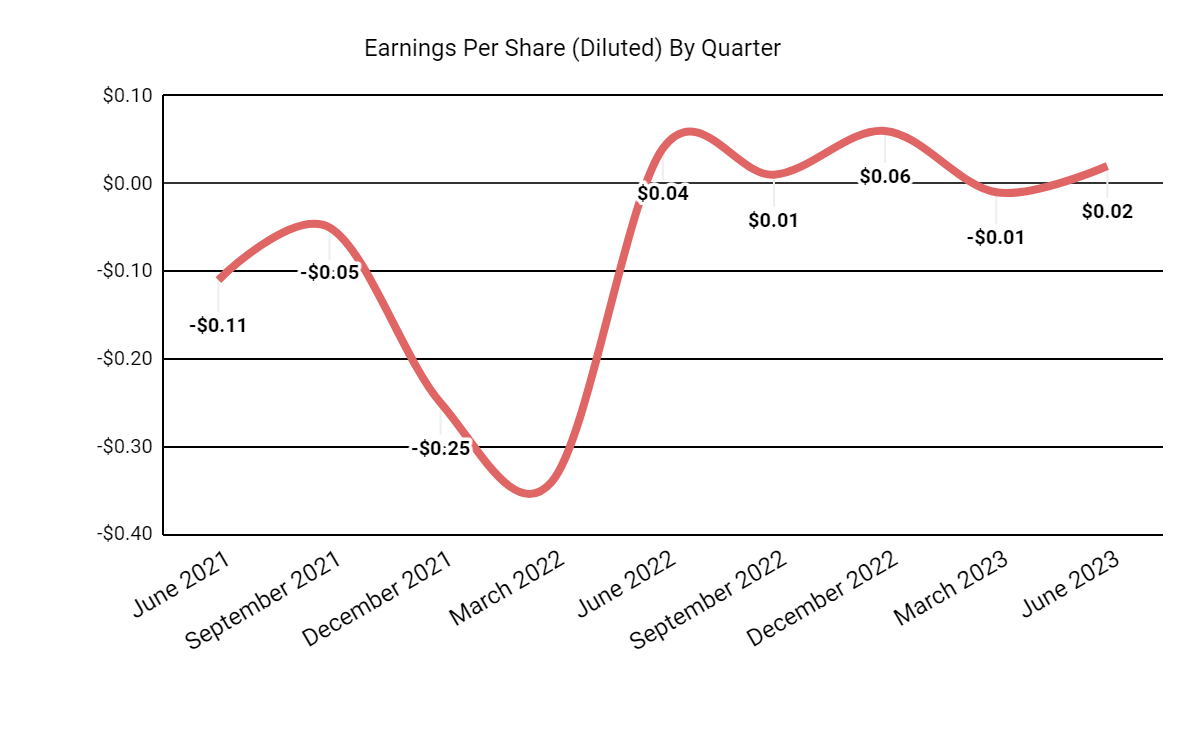

Earnings per share (Diluted) have fluctuated in positive territory within a narrow range:

Seeking Alpha

(All data in the above charts is GAAP.)

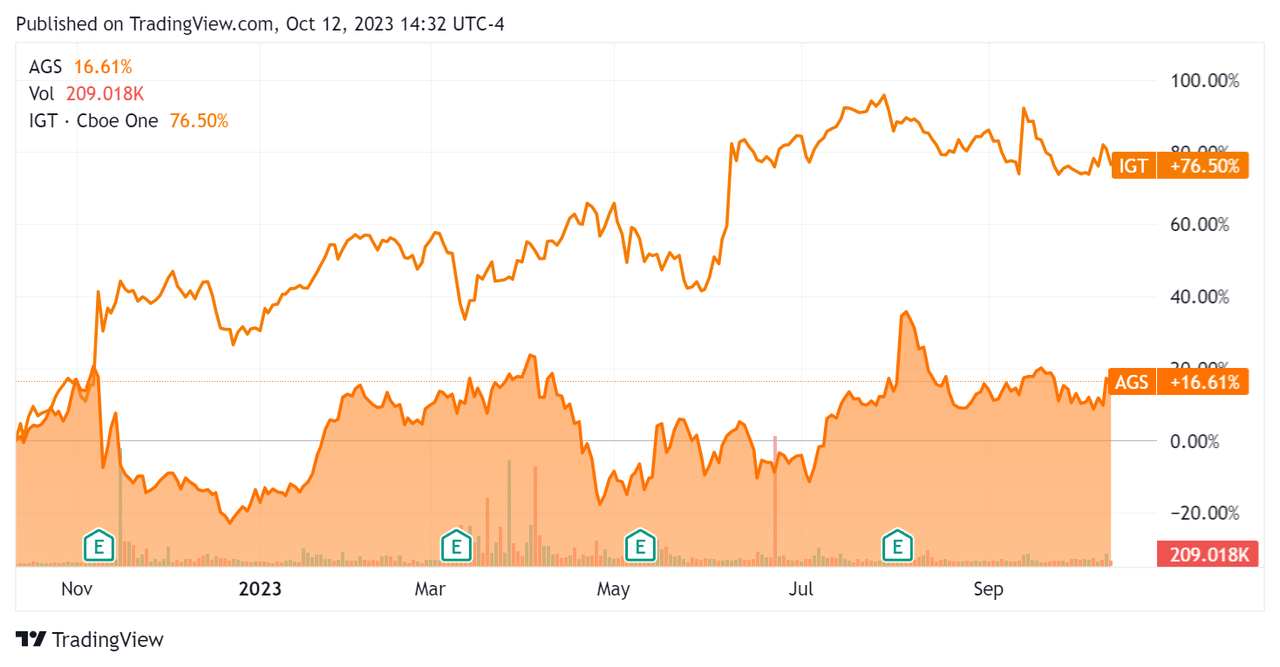

In the past 12 months, AGS’ stock price has risen 16.61% vs. that of International Game Technology’s (IGT) rise of 76.5%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $41.8 million in cash, equivalents and trading asset securities and $553.7 million in total debt, of which $6.1 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $26.7 million, during which capital expenditures were $46.0 million. The company paid $9.2 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For PlayAGS

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.3 |

|

Enterprise Value / EBITDA |

5.8 |

|

Price / Sales |

0.7 |

|

Revenue Growth Rate |

16.1% |

|

Net Income Margin |

1.1% |

|

EBITDA % |

39.9% |

|

Market Capitalization |

$246,460,000 |

|

Enterprise Value |

$771,870,000 |

|

Operating Cash Flow |

$72,680,000 |

|

Earnings Per Share (Fully Diluted) |

$0.08 |

|

Free Cash Flow Per Share |

$0.12 |

(Source – Seeking Alpha.)

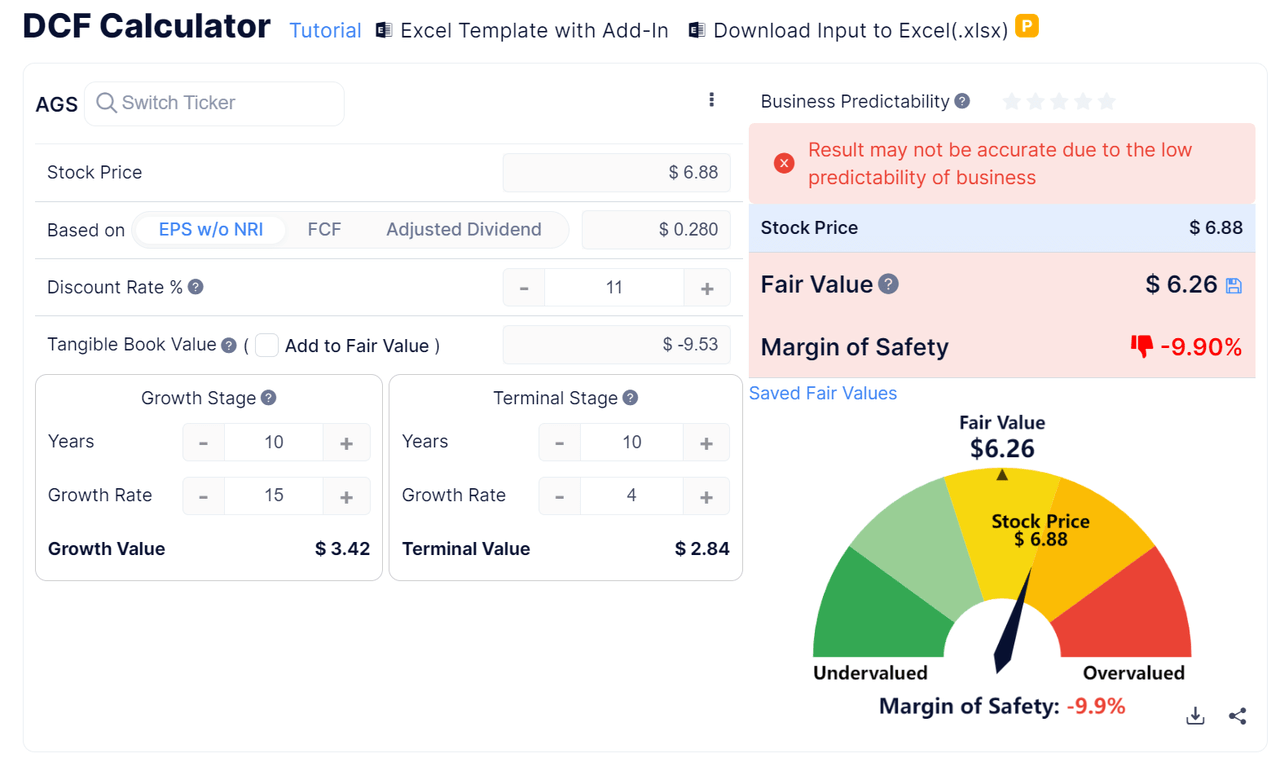

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

GuruFocus

Based on the DCF, the firm’s shares would be valued at approximately $6.26 versus the current price of $6.88, indicating they are potentially currently fully valued.

As a reference, a relevant partial public comparable would be International Game Technology:

|

Metric [TTM] |

International Game Technology |

PlayAGS |

Variance |

|

Enterprise Value / Sales |

2.9 |

2.3 |

-19.7% |

|

Enterprise Value / EBITDA |

8.6 |

5.8 |

-32.0% |

|

Revenue Growth Rate |

4.0% |

16.1% |

304.3% |

|

Net Income Margin |

6.3% |

1.1% |

-83.2% |

|

Operating Cash Flow |

$859,000,000 |

$72,680,000 |

-91.5% |

(Source – Seeking Alpha.)

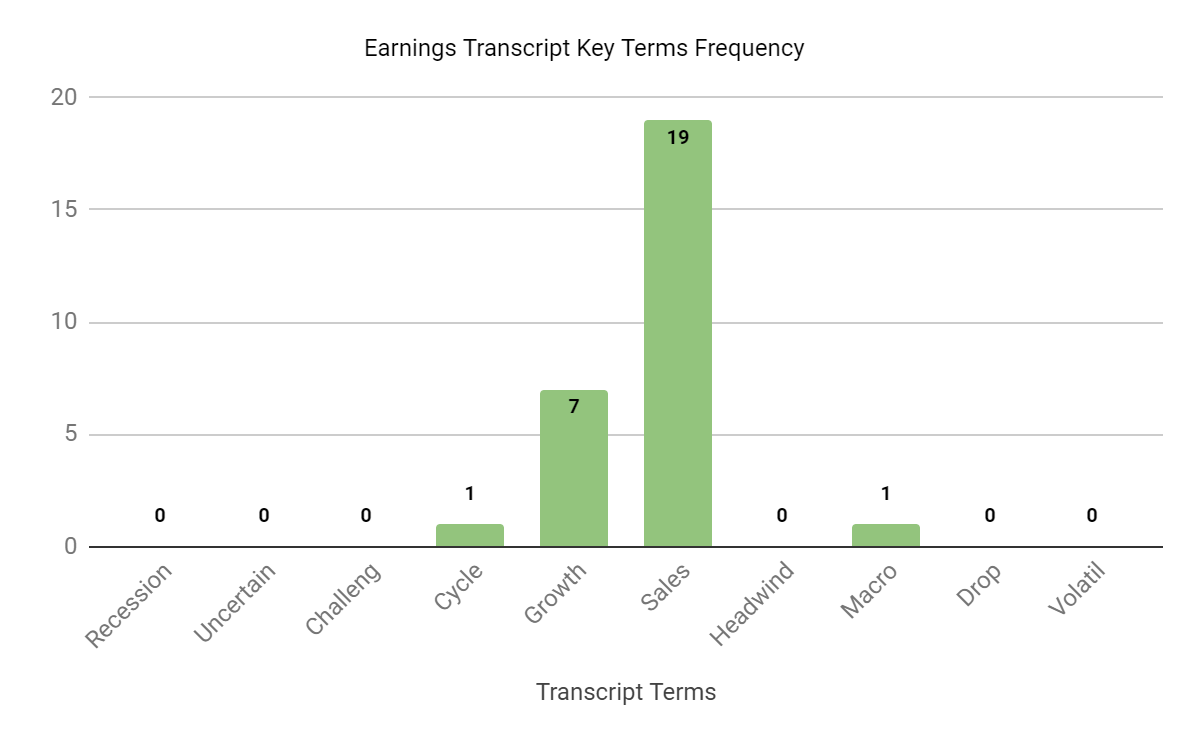

Sentiment Analysis

The chart below shows the frequency of various keywords during the company’s most recent earnings conference call.

Seeking Alpha

Analysts asked management about its leverage goals, R&D spending and operating leverage for its interactive business.

Management said it is focused on getting to below 3x leverage and to refinancing its debt for savings.

The company doesn’t see a need to increase R&D spending and expects to see operating leverage from its interactive business starting in 2024.

Commentary On PlayAGS

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management’s prepared remarks highlighted growing revenue for the 10th consecutive quarter.

Net leverage dropped from 3.8x at the beginning of the year to 3.6x, and the company expects to exit 2023 with net leverage of between 3.25x and 3.5x.

Notably, management said that demand for its new Spectra cabinet “remains robust.”

Also, for its table products, the PAX card shuffler has accounted for more than 265 units sold in an “industry long dominated by one company.”

Total revenue for Q2 2023 rose by 17.2% year-over-year, and gross profit margin was flat.

Management didn’t disclose any client or revenue retention rate metrics.

Selling and G&A expenses as a percentage of revenue were up by 1% YoY, while operating profit increased by an impressive 52.0%.

The company’s financial position is moderate, with significant long-term debt and positive though not strong free cash flow.

Looking ahead, 2023 revenue is expected to rise by 12.7% over 2022.

If achieved, this would represent a drop in revenue growth rate versus 2022’s growth rate of almost 19.2% over 2021.

In the past twelve months, the firm’s EV/EBITDA valuation multiple has fallen by 10.8%, as the chart from Seeking Alpha shows below:

Seeking Alpha

A potential upside catalyst to the stock could include the scheduled opening of new casinos and expansions, which may lead to continued growth in its installed base.

As for valuation, my DCF suggests PlayAGS, Inc. stock may be fully valued at its present level of around $6.90, so I’m inclined to retain my previous Neutral [Hold] outlook for the near term.

Read the full article here