I love biotech investing. While I search sectors and stocks from around the world for deep value opportunities, the biotech sector year in and year out often delivers the best returns for my portfolio. When I invest in biotech, I’m looking for a few different set ups. I either want a rapidly growing company with new technology or a busted biotech that has been left for dead.

Both types of investments often produce great gains as long as they meet certain other criteria. The criteria is quite easy to follow. The company should have cash on hand to handle expenses for at least two years. The company should have upcoming catalysts and the company should have a high level of insider ownership. Before making an investment, I prefer that the company meets two out of three of these criteria. CRISPR has upcoming catalysts and cash on hand but does not have significant insider buying. However it does have considerable institutional ownership and I consider it a solid buy at the current price.

CRISPR therapeutics (NASDAQ:CRSP) was brought to my attention a few months ago and recently I decided to take a closer look. CRISPR Therapeutics AG, a pioneering gene editing corporation, specializes in the advancement of gene-driven medications for critical ailments, harnessing its innovative Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR) and CRISPR-associated protein 9 (Cas9) platform. This state-of-the-art CRISPR/Cas9 technology empowers precise and guided modifications to the genetic code. The company maintains a multifaceted portfolio of therapeutic initiatives that span across various disease domains, including hemoglobinopathies, oncology, regenerative medicine, and rare medical conditions.

Seeking Alpha

Currently with a market cap of around $3.5 billion dollars, CRISPR is priced near the bottom of its 52 week range and has upcoming catalysts due before the end of the year. Just two years ago CRISPR traded at over $100 per share and was considered by many to be a possible buyout candidate. In 2021, J.P. Morgan had a $160 price target on the company which you can read more about here. In the first quarter of 2022, social media buyout speculation was mentioned here and Vertex seemed a likely possible acquirer. With a possible FDA approval now mere months away and CRSP trading near its yearly low, it seems that CRSP is in an even better possible acquisition target today than it was in 2021 or 2022.

Cash on Hand

Despite a high cash burn rate, CRISPR has managed its finances extremely well. Relying on partnerships to provide non-dilutive financing CRISPR has prudently looked out for shareholders.

Seeking Alpha

A recent agreement with Vertex (VRTX) regarding diabetes type 1 treatments provided $100 million dollars up front and an additional possible $230 million for milestone payments. You can read more about the agreement here.

Upcoming Catalysts

Sickle cell disease (SCD) has been awarded priority review status by the FDA, with an approval decision scheduled for December 8, while a standard review for transfusion-dependent beta thalassemia (TDT) is expected to wrap up by March 30, 2024.

Sam Kulkarni (CEO) quotes at Citi’s 18th Annual Biopharma Conference:

“Here we are on the cusp of what could be the first approved CRISPR-based medicine in the world with exa-cel later this year.”

Sam Kulkarni highlights the significant milestone of potentially having the first approved CRISPR-based medicine with exa-cel. Sam emphasized the groundbreaking nature of their work. He suggests that they are at the forefront of a new era in medicine with the potential approval of exa-cel. This claim underscores the innovative nature of their research and the potential impact on the medical field.

-

“We’ve built our own manufacturing facility, we have our own development engine.”

Sam asserts that the company has invested in building its own manufacturing and development capabilities. This quote conveys the company’s commitment to self-sufficiency. By having their own manufacturing facility and development engine, they can control the process from start to finish. This control can lead to increased efficiency and innovation, which is crucial in the biotech industry.

“The next part of the journey for the company is how do you become a $25 billion company in the next three to four years?”

Sam discusses the company’s ambitious growth target of becoming a $25 billion company within a specific timeframe. This quote reflects the company’s strategic vision. Sam is setting a clear and ambitious goal for the company’s future. Achieving a $25 billion valuation in a relatively short period requires significant expansion and success in the biotech sector. In my opinion, this quote shows the possible growth trajectory that CRISPR is trying to accomplish. If the company delivers on this growth, shareholders will see shares appreciate almost 8 times their current value. In regards to risk reward this probably highlights the top end expectations of shareholders.

“And as you see these patterns over time, the antibodies, the first 10 years, there was a certain pattern in terms of market acceptance and market excitement.

Sam suggests that there are patterns of market acceptance and excitement in the biotech industry over time. By drawing parallels between the history of biotech, specifically the acceptance of antibodies as a treatment modality, and the emerging field of gene editing, he implies that just as antibodies evolved from a novel concept to established therapeutics, gene editing, including CRISPR, is following a similar trajectory.

“This is the first CRISPR-based medicine that’s going to go forward for approval.

After ten years of efforts, exa-cel represents a significant milestone as the first CRISPR-based medicine to undergo the approval process. This statement underscores the historic significance of their work. Being the first in a field as innovative as CRISPR-based medicine is a groundbreaking achievement. It implies that they are pioneering a new era in medicine, which could pave the way for future CRISPR-based therapies.

“And from a safety standpoint, we’ve done a very robust preclinical package for going into clinic.”

The emphasis on the thoroughness of their preclinical safety evaluations provides optimism regarding the December 8th FDA meeting. This statement also demonstrates the company’s commitment to safety and quality. The reference to a “robust preclinical package” suggests that they have conducted extensive testing and evaluation to ensure that their therapy is safe for clinical use. Safety is a critical aspect of any medical advancement and data seems to support this idea.

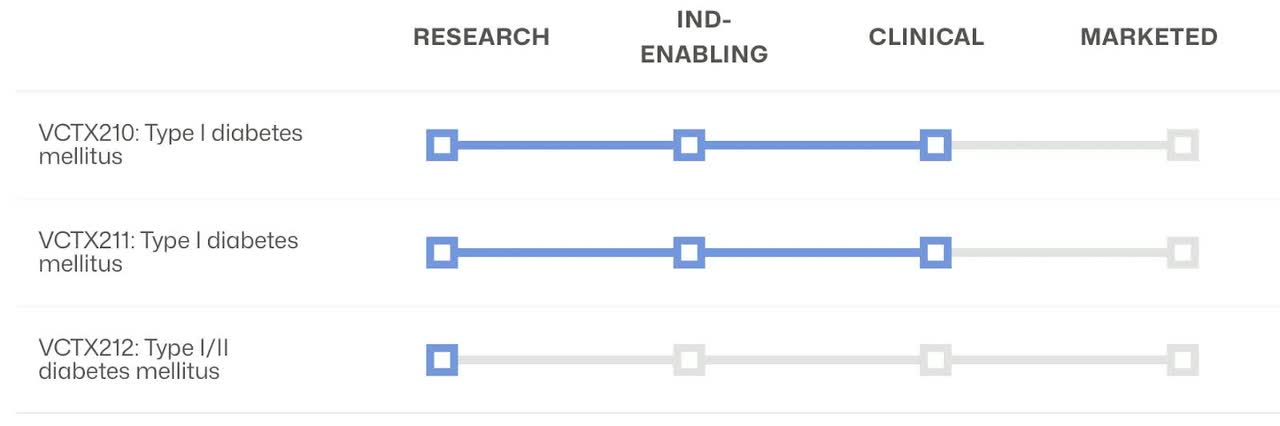

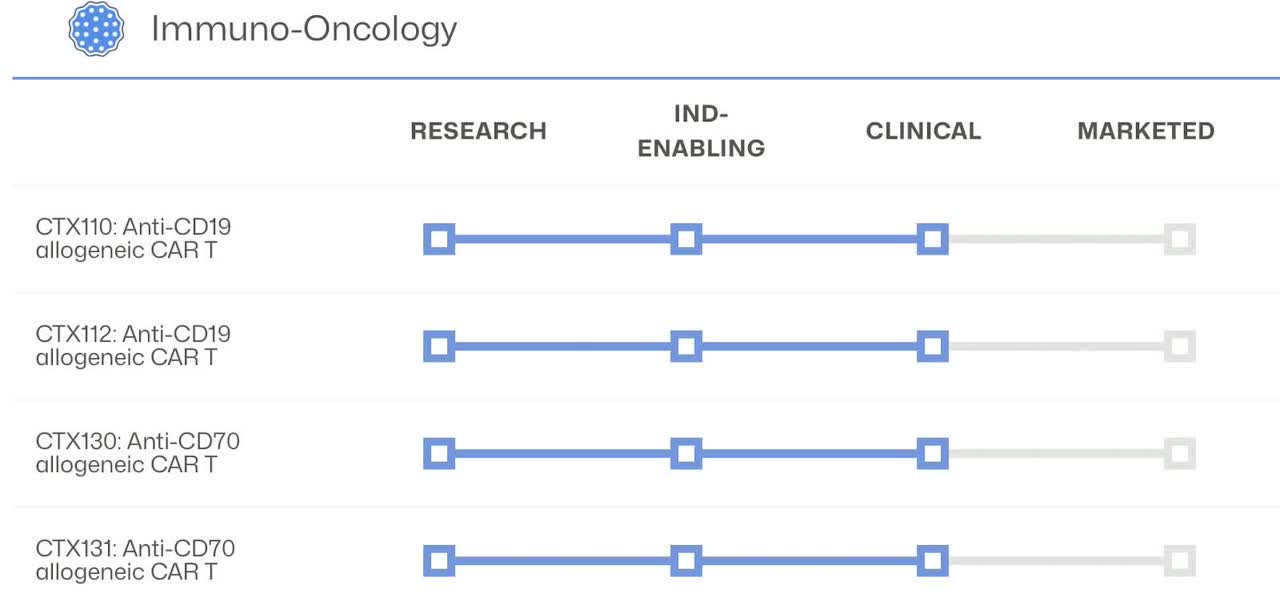

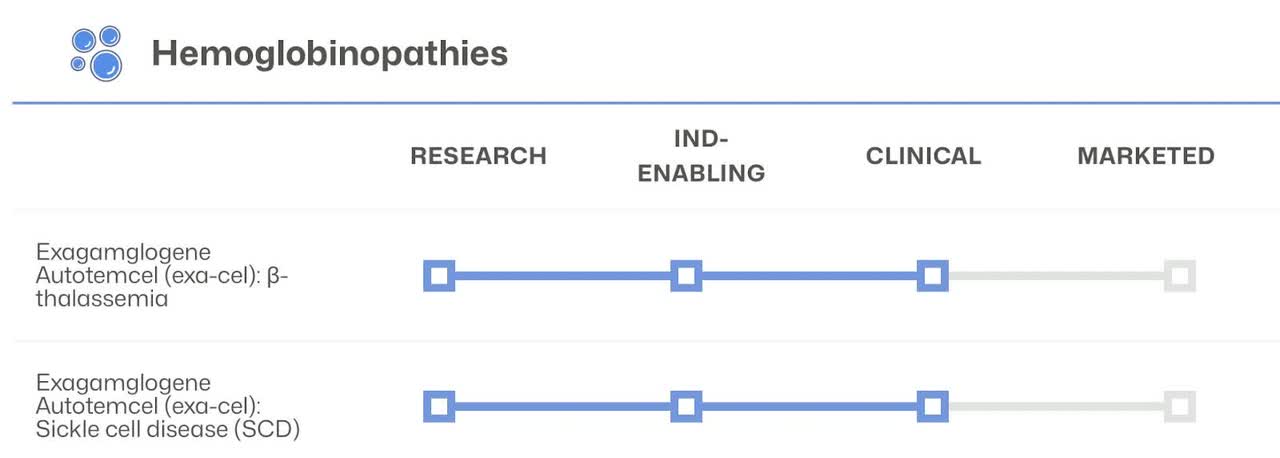

Pipeline

CRISPR’s robust diabetes platform combined with the immuno-oncology and hemoglobinopathies therapies have multiple drugs in stage 3 and are close to reaching the market. These therapies/drugs show how the company can apply its technology to a wide range of diseases and health issues.

CRISPR Website CRISPR Website CRISPR Website

Overall, the future at CRISPR seems rather bright.

The diabetes platform uses allogeneic, gene-edited, immune-evasive, stem cell-derived beta-cell replacement therapy and Investigational allogeneic, gene-edited, immune-evasive, stem cell-derived beta-cell replacement therapy with additional gene edits that aim to further enhance cell fitness.

The Immuno-oncology platform uses Autologous, ex vivo CRISPR/Cas9 gene-edited investigational therapy in which a patient’s own hematopoietic stem cells are edited to produce high levels of fetal hemoglobin in red blood cells, allogeneic CRISPR/Cas9 gene-edited CAR T cell therapy in development for the treatment of CD19+ malignancies that incorporates additional edits designed to enhance CAR T potency and reduce CAR T exhaustion, allogeneic CRISPR/Cas9 gene-edited CAR T cell therapy in development for the treatment of hematologic malignancies and investigational allogeneic CRISPR/Cas9 gene-edited CAR T cell therapy in development for the treatment of solid tumors that incorporates additional edits designed to enhance CAR T potency and reduce CAR T exhaustion.

The hemoglobin therapies made in partnership with VRTX include autologous, ex vivo CRISPR/Cas9 gene-edited investigational therapy in which a patient’s own hematopoietic stem cells are edited to produce high levels of fetal hemoglobin in red blood cells.

I only included the stage 3 drugs and did not even cover the In Vivo approaches to utilizing their technology. The pipeline is diverse and has depth to fuel potential growth for the next decade. To read more about CRISPR’s pipeline I suggest looking at the company’s website.

Risks and Concerns

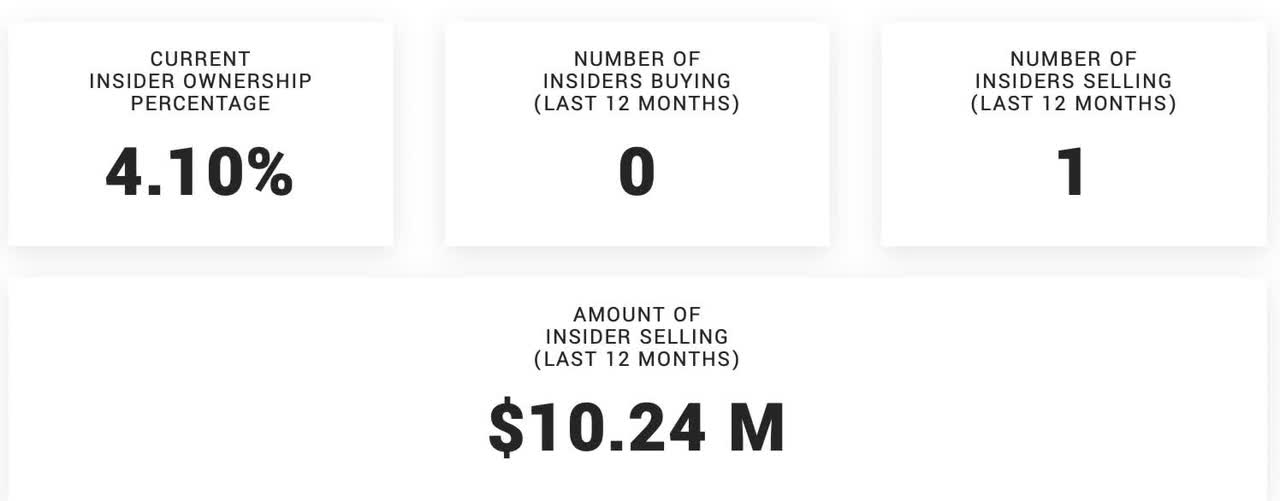

Insider Ownership: Not one insider has been buying shares on the open market and the CEO has been regularly exercising his options and selling shares. Since 96% of his salary is in bonuses including stock options, the regular sales do not concern me too much. If numerous insiders were selling at higher levels, I would be more concerned about it. However, insiders sell for a variety of reasons and all of these sales seem rather regular. The CEO still owns less than half of one percent of the company which could be valued at a little over $16 million dollars. I also think that with upcoming binary catalysts these sales could be just part of an overall prudent investment strategy.

Marketbeat

Regulatory Approval: The company’s biggest concern is obtaining regulatory approval for their CRISPR-based medicine, exa-cel. While they are on the cusp of potentially having the first approved CRISPR-based medicine, the approval process is highly complex and involves rigorous safety and efficacy evaluations. Any setbacks in the regulatory process could delay market entry and commercialization.

Market Acceptance: The reference to historical trends in the biotech industry, such as the evolution of antibodies and RNAi, highlights the concern of market acceptance. CRISPR-based medicines are relatively new, and it may take time for them to gain widespread acceptance among healthcare providers, payers, and patients.

Manufacturing and Scalability: Building their own manufacturing facility is a significant achievement, but the challenge lies in scaling up production to meet potential high demand for CRISPR-based therapies. Ensuring consistent, cost-effective, and scalable manufacturing is a concern, especially as they aim to address multiple diseases.

Payer and Reimbursement Landscape: Ensuring that payers, including commercial payers and government programs like Medicaid and CMS, are willing to cover the costs of CRISPR-based therapies is a significant concern. The company must navigate the complex landscape of healthcare reimbursement to make the therapy accessible to patients.

Physician Training and Infrastructure: Preparing qualified treatment centers and healthcare professionals to administer the therapy effectively is a concern. This includes ensuring that medical staff are trained to handle the entire treatment process, from collecting patient cells to infusing them with the edited cells.

Competition: While the transcript does not explicitly mention competition, the field of gene editing is highly competitive, with multiple companies working on CRISPR-based therapies. CRISPR Therapeutics must stay ahead in terms of innovation, safety, and efficacy to maintain a competitive edge in the market. bluebird’s (BLUE) platforms appear to be a direct competitor to CRSP.

Meeting Growth Targets: Setting a goal of becoming a $25 billion company within a specific time frame is ambitious. Achieving this growth target is a concern, as it requires rapid expansion, successful product launches, and market penetration.

Unexpected Regulatory Questions: The company acknowledges that they cannot predict all the questions that may arise during the regulatory approval process. Addressing unexpected questions or concerns from regulatory agencies can be challenging and may impact timelines.

Final Thoughts

The most significant upcoming catalysts for CRISPR Therapeutics are related to sickle cell disease (SCD), which has been granted priority review status by the FDA, with an approval decision scheduled for December 8. Additionally, a standard review for transfusion-dependent beta thalassemia (TDT) is expected to conclude by March 30, 2024. The CEO of CRISPR Therapeutics, Sam Kulkarni, has expressed optimism about the potential approval of exa-cel, which could become the world’s first CRISPR-based medicine. Sam’s quotes underscore the groundbreaking nature of their work and the company’s commitment to safety and robust preclinical testing.

CRISPR’s strong cash position and diverse pipeline highlight the possible growth of the company. With its robust diabetes platform, immuno-oncology therapies, and hemoglobinopathies treatments, the company is close to reaching the market with multiple drugs in stage 3. These therapies demonstrate how CRISPR can apply its technology to a wide range of diseases and health issues, which could make it a formidable player in the biotech industry or a potential takeover candidate.

One concern is that there has been no notable insider buying, although the CEO’s sales can be attributed to regularly exercising stock options. Regulatory approval also remains a significant concern, as does the time it might take for CRISPR-based medicines to gain widespread market acceptance. Scalability and manufacturing challenges, reimbursement issues, and competition from other gene editing companies add to the complexity. Achieving the ambitious growth target of becoming a $25 billion company within a few years comes with its own set of uncertainties.

Despite these concerns, CRISPR Therapeutics shows promise as an investment opportunity, with its innovative technology, upcoming catalysts, and strong pipeline. Regulatory hurdles, market acceptance, and competition are all reasons for caution. With the stock currently trading near its four year low, I believe that shares present a good value opportunity and I rate CRSP a buy. As always please do your own due diligence before buying any stock and good luck investing.

Read the full article here