Company logo ((company website))

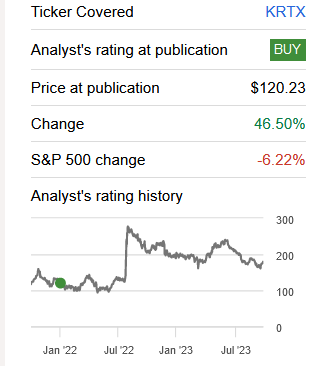

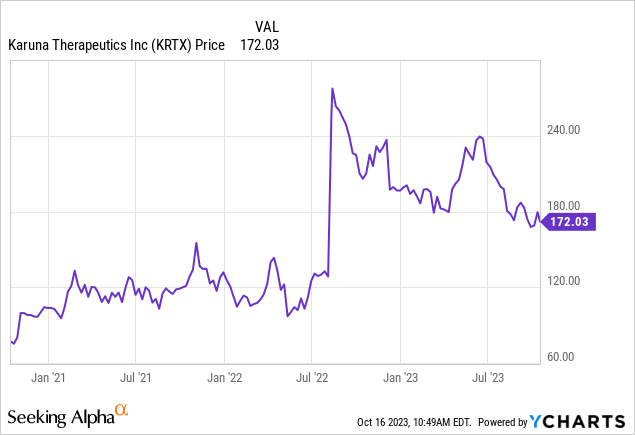

I recommended Karuna Therapeutics, Inc. (NASDAQ:KRTX) in 2022 before the Phase 3 data for KarXT in treating schizophrenia. The stock reached a peak of $290 (165% gain) after the successful Phase 3 trial and is up 41.5% at present since my last Buy rating despite the recent pullback.

Seeking Alpha Rating (Seeking Alpha)

The stock has pulled back recently and is at a good buy level ahead of the upcoming NDA decision (end of this year) and PDUFA for KarXT in schizophrenia (in mid-2024).

Reiterating Buy rating on the common stock with a first price target of $268 (54% upside in 1-year timeframe) based on enterprise discounted cash flow, DCF valuation method.

The valuation is based on my estimate for peak global risk-adjusted revenue for KarXT = $9 billion in 2030.

Karxt could become a new standard of care in a huge global market

Schizophrenia is a $12 billion/year global market (2020), expected to reach $26 billion/year by 2030 (10-K). It affects ~24 million patients globally and ~2.8 million patients in the U.S. It is one of the leading causes of disability worldwide. The top-selling drug Abilify had over $7.5 billion/year in global sales. New treatments are needed as up to 30% of patients do not respond to currently approved treatments.

KarXT, the company’s leading product candidate, has two components: xanomeline, a muscarinic agonist that activates M1 and M4 receptors, and trospium chloride, a muscarinic antagonist that blocks the activation of M2 and M3 receptors in the peripheral tissues. By combining these two components, KarXT aims to enhance the efficacy of xanomeline in the CNS while reducing its side effects in the periphery. It has shown the first novel mechanism of action to treat schizophrenia in decades.

The advantages of this drug over the currently approved treatments for this common condition are:

– Higher potency.

– Faster onset of action.

-Significant reduction in both positive and negative symptoms of schizophrenia. There are negative symptoms in 40% of patients with no FDA-approved treatments.

– Better safety profile, no weight gain, extrapyramidal symptoms, or daytime sleepiness.

– Improvement in cognitive function (vs. decreased cognitive function with approved antipsychotics).

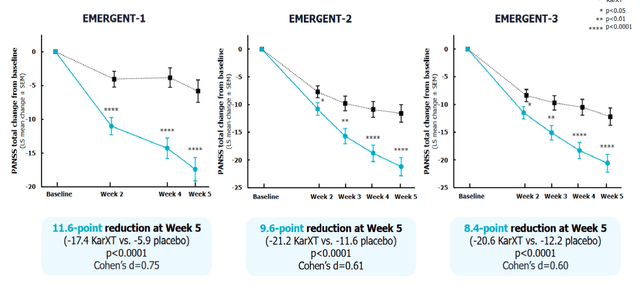

Phase 3 EMERGENT-1 and 2 trials testing KarXT as a monotherapy showed a significant reduction in schizophrenia symptoms as measured by PANSS score compared to the placebo at week 5 (p<0.0001). A significant improvement in both positive and negative symptoms of schizophrenia was seen.

Phase 3 data for KarXT in treating schizophrenia (Investor presentation)

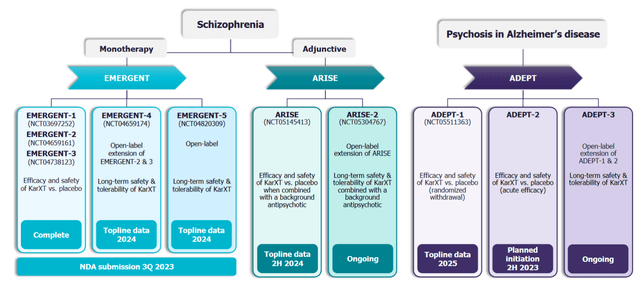

The company submitted a New Drug Application for the FDA approval of KarXT in treating schizophrenia at the end of September. Based on an average FDA review period of 60 days, I expect a positive decision by the end of this year and the PDUFA to be scheduled in mid-2024.

Other indications for KarXT that could expand the target market are:

– Adjunctive treatment for schizophrenia

– Psychosis in Alzheimer’s disease.

KarXT is also being evaluated in a Phase 3 ARISE trial vs. placebo as an adjunctive treatment for schizophrenia in patients with inadequate response to their current antipsychotic therapy. This is a randomized, placebo-controlled, flexible-dose trial with six weeks treatment duration. Based on the low bar of a placebo comparator, I expect a positive result. The data is expected in 2H 2024. Another Phase 3 open-label ARISE-2 trial is ongoing in this indication to test long-term safety and tolerability.

Another large target market for KarXT is psychosis in Alzheimer’s disease. Psychotic symptoms are seen in ~10-75%% of Alzheimer’s patients, a disease affecting 6.7 million patients in the U.S. The U.S. target market is ~1.2 million patients in this indication. There are no FDA-approved treatments for this indication. Currently, used off-label antipsychotic medications have side effects and increase mortality in this patient population. The Phase 3 program in this indication consists of two Phase 3 randomized, placebo-controlled trials in patients with mild-moderate psychosis due to Alzheimer’s disease: ADEPT-1 and ADEPT-2, which have a treatment duration of 12 weeks. The bar for success is low since the comparator is a placebo.

The company is also developing advanced oral and long-acting injectable formulations of KarXT, which could increase patient compliance.

Patents for the drug extend till 2039.

KarXT Phase 3 programs (Investor presentation)

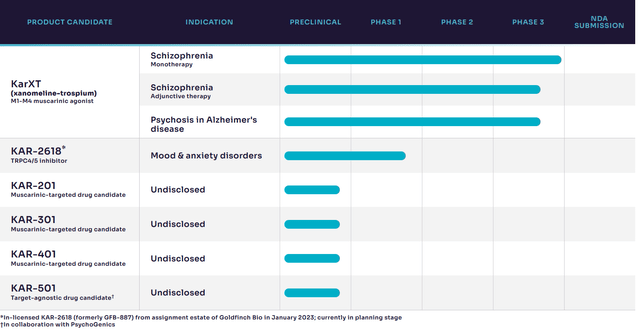

Other product candidates in the pipeline that could increase target markets

KAR-2618, a TRPC4/4 channel product candidate, was licensed from Goldfinch Bio and has shown early safety and efficacy in Glodfinch’s clinical trials. It is planned to be developed in mood and anxiety disorders. Phase 1 data is expected in H1 2024.

Product pipeline (Investor presentation)

Management with big pharma experience

CEO Bill Meury has over 25 years of industry experience, including Executive Vice President/ Chief Commercial Officer at Allergan (acquired by AbbVie for $63 billion). Chief Medical Officer Stephen Brannan served as the Therapeutic Head of Neuroscience at Takeda (TAK) and held senior roles at Novartis (NVS), and Eli Lilly (LLY). Chief Commercial Officer Kane served as Executive Vice President and Chief Commercial Officer at BioXcel Therapeutics and also held senior-level commercial positions at Allergan, Pfizer (PFE), and Sepracor (acquired for $2.6 billion). His experience would be invaluable in the successful commercialization of the company’s product candidates.

The stock is undervalued based on DCF valuation

Balance sheet

The company is expected to have $1.3 billion in cash reserves, which are adequate for the next 12 months at the current operating cash use of $300 million in the last 12 months. There is no long-term debt.

Valuation using the enterprise DCF method

In my calculations, I input the U.S. launch for KarXT in schizophrenia in 2024, reaching a peak revenue of $6 billion in 2030. The input U.S. price was average sales price, ASP=74% of the average wholesale price of $25,000/year/patient, similar to recently launched antipsychotic drugs (in line with Pharmagellen guide), a prevalence of 2.8 million and cumulative probability of reaching the market=75%. I input fully owned program in the E.U. (launch in 2025), reaching a peak revenue of $1.5 billion/year in 2030. The input price was $9,250/year/patient (half of the U.S. A.S.P.), a prevalence of 1.5 million, and a cumulative probability of 75%. For the Greater China market (launch in 2025), I input A.S.P. = $9250/year, prevalence of 8 million, and cumulative probability of 75%, resulting in a peak revenue of $8 billion/year in 2030 for the partner Zai Lab. For the royalties revenue for Karuna, I input tiered royalties ranging from 11% to 16%, resulting in a peak royalty revenue of $1.2 billion in 2030. I adjusted 10% royalties payable to PureTech and Eli Lilly (LLY).

Using these calculations, my estimate for the peak revenue for KarXT is $9 billion in 2030. I have not input potential future revenue in other key rest of the world territories like Japan, which could add to further future estimated revenue.

| Territory | Prevalence | Input price/year | Probability | Peak revenue estimate (2030) |

| U.S. | 2.8 million | $18,500 | 75% | $6.2 billion |

| E.U. | 1.8 million | $9,250 | 75% | $1.5 billion |

| Greater China (royalties) | 8 million | $9,250 | 75% | $1.2 billion |

| Total risk-adjusted revenue in the above territories | $9 billion (2030) |

For the operating value calculation, I input cost of revenue = 50% of revenue, EBITDA = 32% of revenue, and free cash flow =18% of revenue (average for the pharma industry). I used a discount rate of 10%, decreasing to 8% after the 2025 launch of KarXT. For the terminal value, I used half of the sum of discounted cash flows till 2030. Using these inputs, the forecasted enterprise value of the operations is $9.6 billion.

For equity value calculation, I input 98% of the cash reserves (1.27 billion), deferred tax assets of $548 million, and total liabilities of 13.8 million (operating lease liability). The input diluted share count was 30.8 million.

Using these inputs, my estimate for the fair value per share is $268 using this valuation method. I have not input KAR-2618 in treating major depressive disorder and anxiety disorder, two large target markets, which could add further upside to the stock price.

Link to DCF Model.

Catalysts:

– Year-end 2023: NDA decision for KarXT in treating schizophrenia is expected by year-end.

– H1, 2024: Phase 1 data for KAR-2618 in treating major depressive disorder and anxiety disorders.

– 2H, 2024: Potential approval and launch of KarXT in schizophrenia

– 2H, 2024: Top line data from Phase 3 ARISE trial testing KarXT as an adjunctive treatment for schizophrenia in 2H, 2024.

– 2024: Top line data from open-label Phase 3 EMERGENT-4 and EMERGENT-5 trials for KarXT testing long-term safety and tolerability in schizophrenia.

– H1, 2025: Top line data from Phase 3 ADEPT-1 trial for KarXT in treating psychosis in Alzheimer’s disease.

Reiterating Buy on Karuna Therapeutics common stock with a first price target of $268 (54% upside in 1-year timeframe).

Disclaimer

Risks in this investment include underwhelming data, unexpected side effects, unfavorable FDA decision, etc. which may cause the stock price to fall.

This post represents my own opinion and is not professional advice. Please conduct your own due diligence or consult a professional investment advisor before making any investment decisions. Investing in developmental stage biotech/pharma stocks is risky, and it is possible to lose the entire capital.

Read the full article here