Investment Thesis

Our current investment thesis is:

- We believe Sally Beauty Holdings (NYSE:SBH) will continue to see <3% growth and market share loss, as Management is unable to improve the market perception of its brand and increase popularity. This will mean moderate returns but continued negative market sentiment. Its peers are growing better and are closing the margin gap, which we expect to continue.

- Upside is present in the event of a takeover, with good value for an acquiring brand. With the company substantially undervalued relative to its FCF (~25% FCF yield), an acquirer can be more particular about culling bad parts of the business (loss-making locations) without having to pay for them.

Company Description

Sally Beauty Holdings, headquartered in Denton, Texas, is a global distributor and retailer of professional beauty supplies. The company operates through two main segments: Sally Beauty Supply, serving both retail consumers and salon professionals, and Beauty Systems Group, catering exclusively to salon professionals.

Share Price

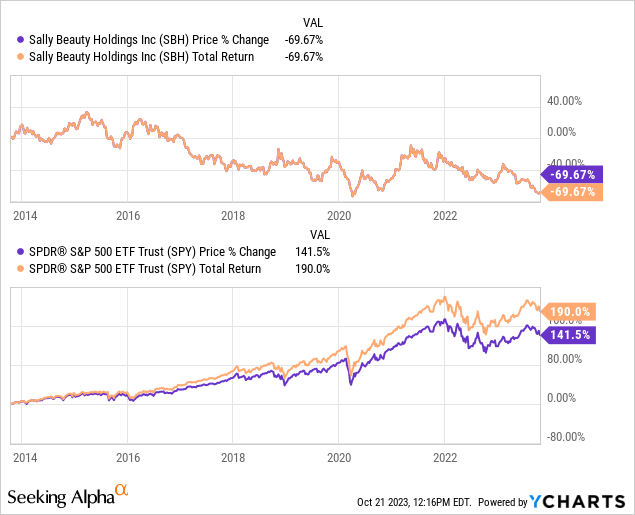

SBH’s share price performance has been disappointing, losing over 60% of its value during the last decade in a consistent, unrelenting fashion. This is a reflection of the company’s poor financial development during this period and a change in industry dynamics.

Financial Analysis

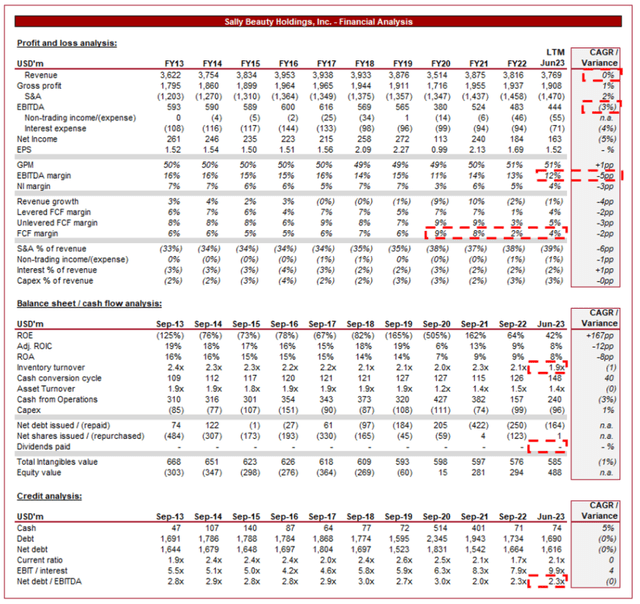

Sally Beauty financials (Capital IQ)

Presented above are SBH’s financial results.

Revenue & Commercial Factors

SBH’s revenue has traded flat during the last decade, with growth initially in the LSDs, followed by 5 fiscal years of decline in 6 years. EBITDA has lagged behind this, with a CAGR of (3)%.

Business Model

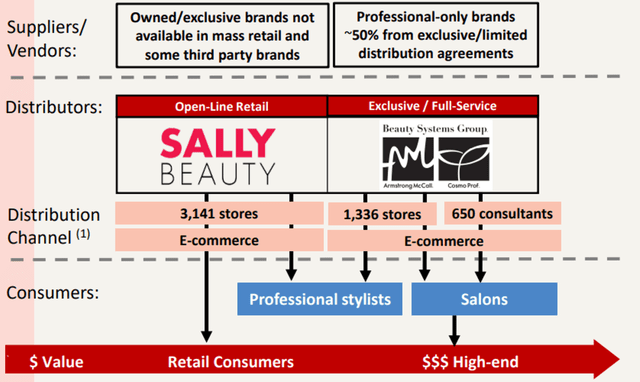

Business model (Sally Beauty)

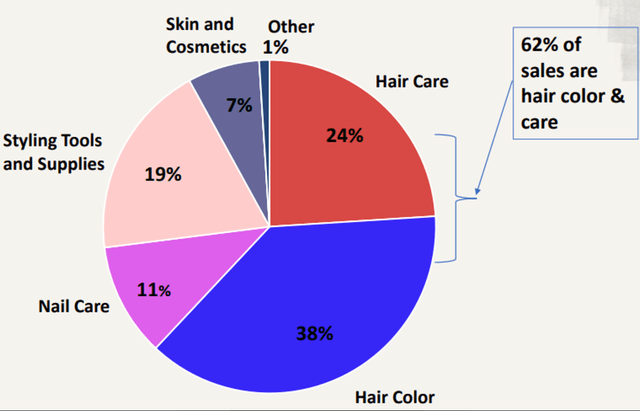

SBH operates as a retailer of beauty products, catering to both individual consumers and professional hairstylists. It offers a wide range of beauty and salon products, including hair color, styling tools, skincare, and nail care items. Its stores operate as a one-stop-shop for the everyday consumer and professionals alike, although the professional segment also utilizes consultants for targeted selling.

The company’s product mix is diversified, although with a clear focus on hair. This is a similar case for its professional segment (naturally), with 83% of sales in color or care.

Retail Product Mix (Sally Beauty)

SBH has developed private label and exclusive brands, which have allowed the company to earn higher profit margins. These products are sold exclusively in SBH’s stores, encouraging customer loyalty, and are only possible due to the development of its brand. Management is currently focused on increasing its own brand penetration to >50%.

Own brands (Sally Beauty)

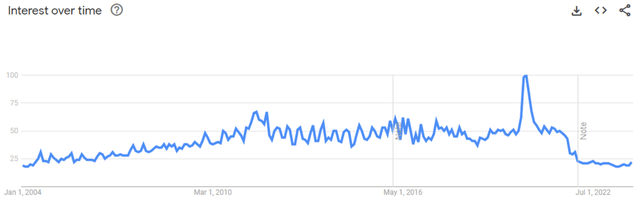

SBH offers an online platform for browsing and purchasing products, as well as understanding the wider services it offers. The company’s penetration thus far has been poor, and is reflective of its overall only presence, with <10% of sales from this channel.

We believe its weak online presence is one of the key reasons its growth has been poor. During the last decade, we have seen an aggressive digitalization of society, with consumers increasingly shopping, and being influenced by, online channels (social media and e-commerce). As the following illustrates, interest in Sally’s business has lacked development for an extended period. This is due to a shift in consumer spending to its competitors, who are more effectively marketing their business to consumers.

Brand interest (Google)

Management has attempted to offset this weakness through revitalization efforts, launching sub-brands, concept stores, and new products, all of which have failed (or at least not succeeded). We attribute this to its fundamental inability to resonate with a younger audience, with none of these efforts connecting with this demographic sufficiently. Another dataset we would point to is Instagram. Sally has less than 1m followers and is currently getting <500 likes on most of its posts, illustrating a complete lack of engagement.

Our view is that the company needs to take note of other beauty businesses and how they are operating. More partnerships with influencers, limited edition collaborations, more social media marketing, etc. Instead, the business is doubling down on stores and brands.

Brand revitalization efforts example (1) (Sally Beauty) Brand revitalization efforts example (2) (Sally Beauty)

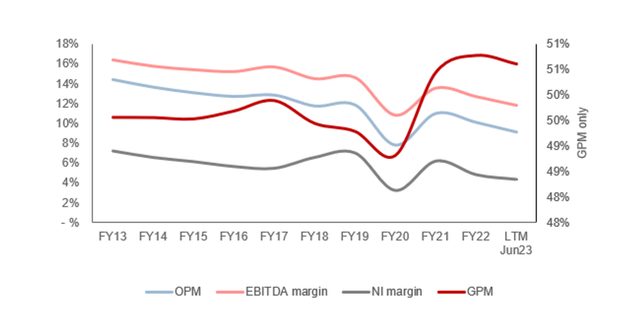

Margins

Margins (Capital IQ)

SBH’s margins have broadly traded flat, which is unsurprising given the company’s scale. With limited commercial development during this period but a core demographic to target, we have not seen margins slide significantly. This at least positions the business well to bounce back should growth successfully return.

Our concern here, however, is that S&A spending has increased as a proportion of revenue to 39% (+6ppts), which implies Management has attempted to improve revenue with little success. We believe it is clear Management is unsure how it can reinvigorate interest.

Quarterly results

SBH’s recent performance has materially slowed, with top-line revenue growth of (2.8)%, (2.4)%, 0.8%, and (3.2)%. In conjunction with this, margins have slightly softened, continuing the downward trend since the peak post-pandemic year (FY21).

This decline is a reflection of the current macroeconomic environment in our view. With elevated interest rates and inflation, consumers are experiencing an uplift in living costs, contributing to a reduction in discretionary and non-core spending to protect finances. Naturally, this has a range of retail and services businesses, with SBH not immune.

The benefit the company has is that it targets women, who disproportionately compromise the US population and control/influence over 85% of spending decisions. This has historically allowed women-focused businesses to outperform and also remain resilient, which is not the case for SBH. We attribute this to its wider commercial weakness.

Looking ahead, we suspect the environment will continue to present difficulty, with the risk of a recession remaining high due to the compounding negative impact throughout the economy. With 5 negative growth quarters in the last 6, we see little resilience from SBH which implies it will continue to struggle, although growth will naturally normalize.

Key takeaways from its most recent quarter are:

- Following the difficulties faced in recent quarters, the company has taken the decision to close a number of its stores. In Q3, the company saw a reduction of 352 locations.

- Comparable sales increased 0.6%, although we are not overly impressed by this given the slide in gross profit margins. Further, e-commerce growth was only 3% and comprises <10% of revenue, implying penetration continues to be disappointing.

- Management is rolling out a number of operational improvements across the business seeking to protect margins, which are having minimal impact in achieving stabilization. This will contribute to some improvement once demand improves but the fundamental issues remain unaddressed.

Balance Sheet & Cash Flows

SBH is reasonably financed, with an ND/EBITDA of 2.3x. The company’s interest coverage is 10x and interest represents 2% of revenue, reducing any liquidity or solvency concerns.

Inventory turnover continues to slip, suggesting demand is sequentially declining beyond the level expected by Management. This is contributing to a softening of its FCF margin, although the business has broadly achieved consistent cash returns.

Said cash has historically been used to buy back shares, although recently Management has preferred deleveraging, which we consider a good decision given the interest rate environment. Diluted share count has declined ~32% during the decade, implying impressive potential.

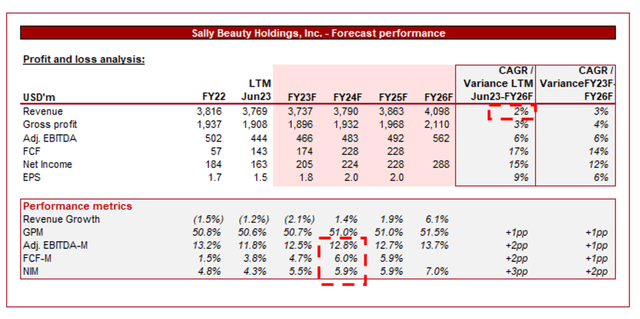

Outlook

Outlook (Capital IQ)

Presented above is Wall Street’s consensus view on the coming years.

Analysts are forecasting a continuation of SBH’s weak growth, with a CAGR of 2% into FY26F. In conjunction with this, margins are expected to remain broadly flat.

We consider these forecasts to be reasonable. Management has attempted several strategies to improve growth, to no avail. We have little faith that any improvement can be achieved. Further, with a lack of improved growth, margins are unlikely to improve.

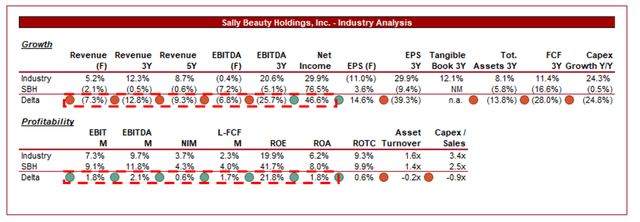

Industry Analysis

Specialty Stores Stocks (Seeking Alpha)

Presented above is a comparison of SBH’s growth and profitability to the average of its industry, as defined by Seeking Alpha (23 companies).

SBH is performing moderately relative to its peers, although this further illustrates the fundamental issues with the company. SBH’s growth is noticeably below its industry average, with this forecast to continue into the forward period. This is a reflection of its loss in market share and lack of competitiveness.

SBH does continue to boast its strong margins, however. Management has done well to maintain this level and is unwilling to compromise. This will ensure that, at a minimum, buybacks and moderate returns cash returns can continue once demand turns positive again.

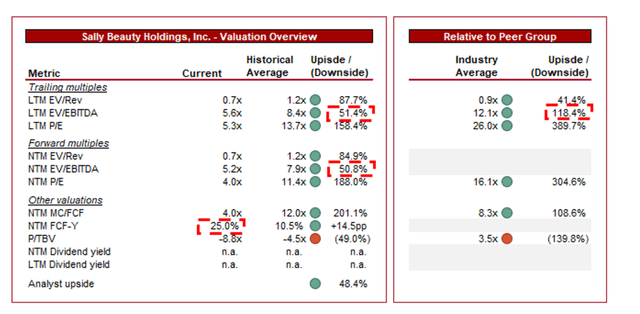

Valuation

Valuation (Capital IQ)

SBH is currently trading at 6x LTM EBITDA and 5x NTM EBITDA. This is a discount to its historical average.

A discount to SBH’s historical average is warranted in our view, owing to the difficulties in attempting to reinvigorate demand. Further, the company now faces greater margin risk if this commercial position is not turned around, as it retreats from markets through store closures. At ~50%, we believe the discount is likely overplayed. We would have suggested closer to ~30%.

Further, SBH is currently trading at a ~120% discount to its peers on an LTM EBITDA basis and ~300% on an NTM P/E basis. This is clearly completely overdone, although a discount is certainly warranted. This reflects the degree to which investors have turned sour on the growth potential of the company.

This is a classic case of moderate-to-bad company trades at an attractive price. At a 25% NTM FCF yield, the stock appears ridiculously cheap. Speculators could do incredibly well buying this business at this price.

We are not convinced, however, and neither are investors it appears. Its valuation has trended down consistently with this extended period of stagnation and so the widening discount is deceiving.

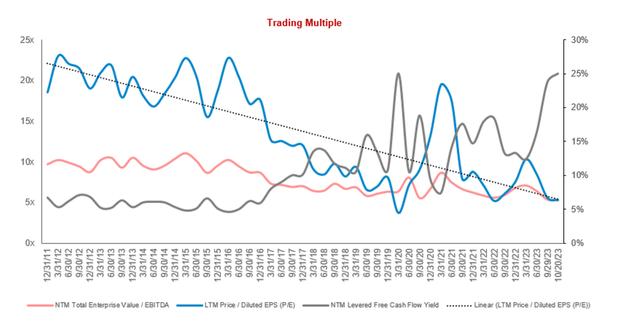

Valuation evolution (Capital IQ)

M&A

With SBH trading so cheaply, we believe the company represents an impressive takeover target. A fashion-forward online business with strong brands could do well to partner these with SBH’s infrastructure and reach, while also having better capabilities to reinvigorate growth. More broadly, a retail business with a strategic goal in mind could be an option.

At a minimum, the acquirer can physically access individuals globally who are still shopping in the traditional channels, while closing underperforming stores or those in unimportant locations. The upside would come through elevating SBH’s core brands.

Margins would be the biggest issue as SBH is unlikely to be accretive but with synergies and economies of scale, we could see SBH push toward an EBITDA-M of ~18% as a division within a group.

We have not explored any potential options, although note the following could be considered: e.l.f. Beauty (ELF), Ulta Beauty (ULTA), Amazon (AMZN) (as part of Amazon Beauty), CVS Beauty, Dufry (OTCPK:DUFRY), Natura (NTCO), and Coty (COTY).

Key Risks With Our Thesis

The risks to our current thesis are:

- Successful implementation of digital strategies

- Innovative product launches

- Strategic partnerships (Think in the vein of Sephora (OTCPK:LVMHF) and Kohl’s (KSS))

Final Thoughts

SBH has experienced a lost decade. The company has seen no revenue growth, flat margins, and a decline in competitiveness. The beauty industry as a whole has developed rapidly during this period and SBH has been left behind in our view. The company is currently living off its historical product and brand strength but is losing market share day by day.

Management has tried and failed to jumpstart growth, with our belief that its fundamental strategy is incorrect. We do not see this changing any time soon.

The only interesting thing about this company is its valuation, which is incredibly low. The company does generate good FCF and so there is fundamental value at a price. For us, we do not buy bad businesses at any price and so without commercial development, we will maintain a hold rating.

This said, things could quickly change if the company is taken over.

Read the full article here