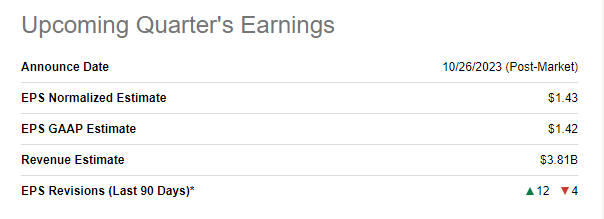

Republic Services, Inc. (NYSE:RSG) will report its Q3 earnings after hours on Thursday, October 26th. Analysts expect the company to report $1.43/share on the back of $3.81 billion revenue. Should Republic Services meet these numbers, it’d represent an EPS growth of ~7% and revenue growth of ~6%. Not too bad for a company (or whole industry) that is generally looked down upon as an investment choice.

Let’s preview Q3 in detail, with a focus on the following:

- Expectations heading into Q3 report

- The company’s recent earnings history

- Things to watch in the Q3 report

- Valuation heading into earnings

- Technical setup heading into earnings.

RSG Earnings Preview (Seekingalpha.com)

Mixed Expectations

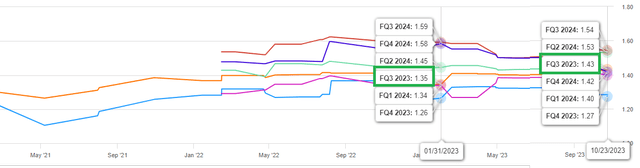

Republic Services goes into Q3 report with mixed expectations as while 12/16 EPS revisions have been to the upside, just 4/13 revenue revisions have been to the upside. This suggests that analysts expect the company to have operated more efficiently in Q3 to compensate for reduced sales expectations. Overall, heading into Q3, RSG is expected to report $1.43 cents/share, which is up 6% since the beginning of the year.

RSG Q3 Revisions Count (Seekingalpha.com) RSG FQ3 EPS Trend (Seekingalpha.com)

Beat or Miss? Enviable History

Republic Services has beaten both EPS and revenue estimates in each of the last 8 quarters. In fact, based on data available on Seeking Alpha, the EPS streak stretches to the last 12 quarters and revenue beat goes back to the last 9 quarters. Quite impressive. 4 out of the last 5 EPS beats have been by at least 10%, while the revenue beats have been much smaller with the biggest beat in the last 10 quarters being by about 4%. Using historical data, I am predicting EPS to come in between $1.50 and $1.55 (a minimum beat of 5%) and for revenue to come in at $3.85 billion (1% to 2% beat at best).

RSG Earnings Surprise (Seekingalpha.com)

Things To Watch

- In each of the last 4 quarters, Republic Services, Inc. has paid more than $100 million towards interest expenses with the two most recent quarters averaging $125 million. This should not be too surprising given the interest rates, but is something to monitor in Q3 report as well.

- Operating expenses jumped up 10% YoY in Q2 2023 and 18% YoY in Q1 2023. Based on that trend, I expect Q3 2023’s operating expenses to cross at least $800 million, only the 2nd time ever that would have happened should it materialize.

- I expect the price per ton of recycled commodity to continue decreasing YoY, as 2022 likely represented the peak for the time being. In Q1, price per ton of recycled commodity dropped $96 YoY while Q2 dropped $99 YoY. Q3 2022’s average price per ton was $162 and I expect that to come in well below $100 for Q3 2023. The company processes 6 million tons of recycling each year and the price decrease here is clearly material.

- Otherwise, I expect Republic Services to report an usual Q3, quietly going about its ways without much fanfare. Just like their services have been for my home and neighborhood.

Valuation

- With a forward multiple of nearly 27, I’d argue RSG stock is going into earnings perhaps a touch overvalued given its earnings prospects. But then, peer Waste Management, Inc. (WM) is trading at a forward multiple of 26.

- With a median price target of $166 from 17 analysts, RSG stock appears reasonably attractive here as it is currently trading 16% away at $143. The lowest price target being $155 suggests there is relative margin of safety buying here.

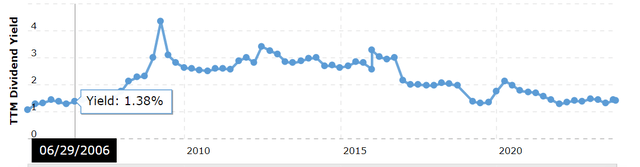

- As a result of the stock’s strong performance over the last 5 years where it has more than doubled, its current yield is at one of its lowest points dating back to 2006 at least, except for a brief period in 2019. With much safer options outside the stock market yielding more than 5% these days, it is hard to make the case for a stock yielding 1.50% and trading at full, if not premium, valuation.

RSG Yield (Macrotrends.net)

Technically Alright

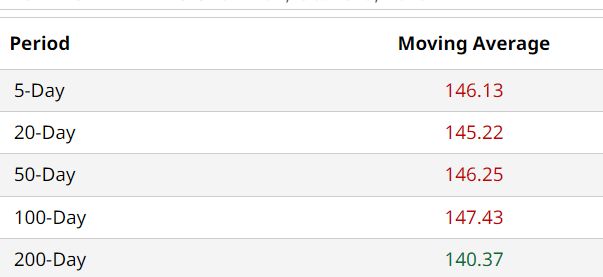

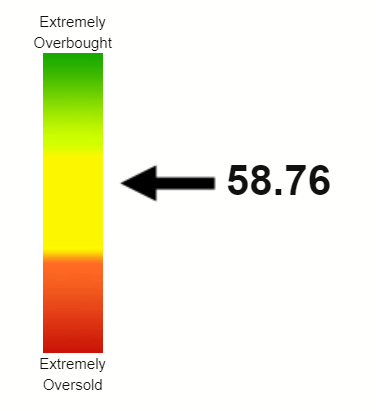

RSG stock is heading into Q3 earnings with a reasonable technical setup as the stock is above the all-important 200-Day moving average but is below all the other moving averages. The $140s zone appears to have a lot of support based on the numbers below. However, should the Q3 report disappoint, the bottom may give out. A Relative Strength Index [RSI] of nearly 60 suggests the stock has reasonable momentum here but also has enough room to increase in price before getting technically overbought. Q3 report will go a long way in determining the direction obviously.

RSG Moving Avgs (Seekingalpha.com) RSG RSI (Stockrsi.com)

Conclusion

The market has undoubtedly been choppier in the second-half of the year compared to the fairly smooth sailing in the first-half. Stocks like RSG may catch more bids as investors may seek safety in such an environment, as highlighted by this upgrade.

As far as the Q3 report is concerned, Republic Services is unlikely to surprise investors in either direction. As I alluded to above, I am a happy current customer of Republic Services, and one day, look forward to being a happy investor as well. But the price for Republic Services, Inc. just isn’t right for me to initiate a position here.

Read the full article here