Thesis

While they might be boring, short term bond funds have delivered in 2023. We are experiencing yet another market correction, with analysts split on whether we are going to have a soft or hard landing next. In today’s environment retail investors are best served by doing simple things rather than try to chase a market which is unsure of its ultimate direction. A simple decision at the beginning of 2023 would have been to stay entirely in cash like instruments such as the PIMCO Enhanced Short Maturity Active Exchange-Traded Fund ETF (NYSEARCA:MINT).

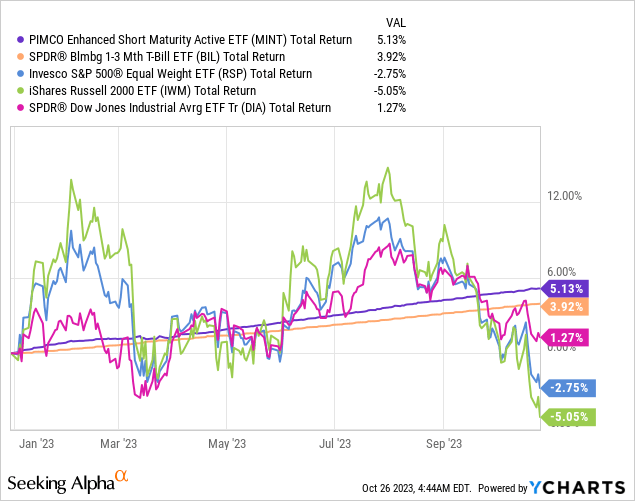

While very boring, such a decision would have been a very rewarding one:

We can see from the chart above how MINT was able to deliver a nice steady total return this year, outperforming so far most of its short term cash parking vehicles peers as well as a number of equity indices, such as the Invesco Russell 2000 ETF (IWM), the Invesco S&P 500 Equal Weight ETF (RSP) and the Dow Jones via the (DIA) ETF. The graph above is presented from a ‘total return’ perspective, thus dividends are included.

Boring sometimes pays off, especially in uncertain markets. We feel 2023 is not going to be a year when a retail investor needs to be a hero, and for those that are not very active investors simple choices are going to be very rewarding ones. At the current pace MINT is set to offer a total return in excess of 6% for 2023 with an incredibly low annualized volatility of 0.63%.

We feel this trend is going to continue for at least another 6 months, with interest rates staying higher for longer, and the economy slowly absorbing higher rates in each of its sectors, such as housing, CRE lending and consumer credit.

What does MINT actually do

MINT is a short term corporate bond fund with an ultra-low duration profile and a diversified portfolio:

Portfolio Metrics (Fund Website)

Rather than invest in T-Bills outright, a retail investor can purchase a corporate bond fund like this one, where a spread to treasuries can be picked up with a relative safe credit risk and duration profiles. It is important to note that while the fund has a 30-day SEC yield of only 5.53%, its portfolio yield is 6.21%, meaning that the 30-day SEC yield is going to slowly move higher towards the portfolio yield as time passes.

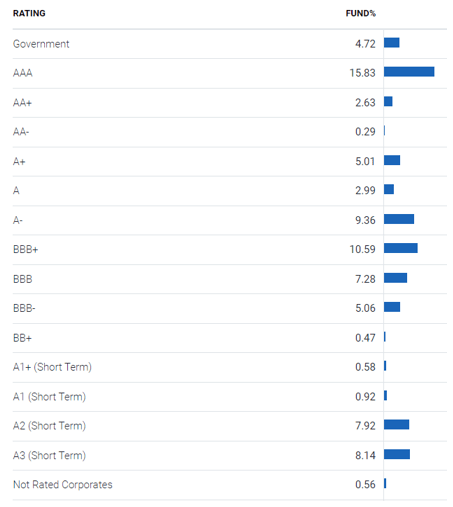

The fund is basically made up of investment grade debt only:

Ratings (Fund Fact Sheet)

The riskier ‘BBB’ credits make up only 23% of the fund’s collateral. There is a tiny 0.47% ‘BB’ bucket that is related to fallen angels or split rating names. The fund also contains a sizable allocation to commercial paper, which you can see in the ‘Short Term’ ratings section. Commercial paper is ultimately corporate risk, just issued in a different format from bonds:

Commercial paper is an unsecured, short-term debt instrument issued by corporations. It’s typically used to finance short-term liabilities such as payroll, accounts payable, and inventories. Commercial paper is usually issued at a discount from face value. It reflects prevailing market interest rates. Commercial paper involves a specific amount of money that is to be repaid by a specific date. Minimum denominations are $100,000. Terms to maturity extend from one to 270 days. They average 30 days.

A well-composed granular short term bond fund can easily absorb a couple of defaults if they occur given the low representation in the collateral pool and the historic recovery rates on senior unsecured debt.

MINT risk profile

This is where this fund excels in term of offering a very compelling risk/reward profile:

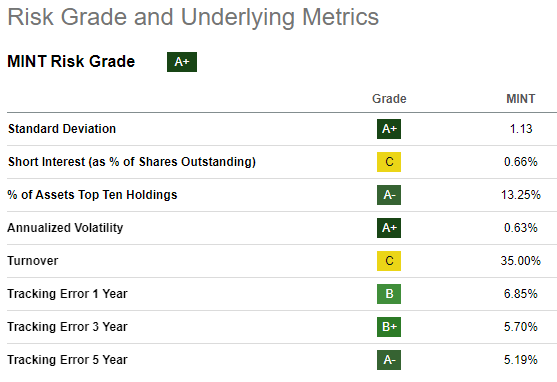

Risk Profile (Seeking Alpha)

The vehicle has a very low standard deviation of 1.13% and an extremely low annualized volatility of 0.63%. This translates into an expected -1% drawdown in normalized market conditions.

The fund manages its probability of default via a high grade collateral and a very short dated tenor profile. However, MINT has a high exposure to financials, which can introduce one-off events in terms of failures as we have seen with the regional banks crisis earlier this year when investment grade entities defaulted in a matter of weeks. Financials are a very particular sector, because their solvency largely depends on trust, and defaults occur in very short time-frames.

From an interest rate sensitivity standpoint the fund is very well set-up:

Duration Profile (Fund Website)

The fund has an effective duration of 0.09 years, which translates into a lack of impact to the fund from higher rates from a mark to market perspective. As interest rates rise the fund is able to turn-over its collateral fast enough due to maturities that it does not take profit and loss hits from higher rates. This has been a winning formula in 2022 and 2023.

What comes next for MINT

As long as rates stay high MINT is going to deliver a high yield. The fund is moving towards a 6.2% 30-day SEC yield as time passes. Given its collateral composition and risk metrics, expect a drawdown of around -1% if we have a very significant risk-off event in the markets. Despite its large financials composition we are not worried about the probability of default embedded in this portfolio.

Expect a continuation of the 2023 performance here, with a nice upward sloping total return line for MINT, and a comfortable ‘clipping the coupon’ action for retail investors here.

Conclusion

In an uncertain market boring can deliver, and MINT has done that. The fund is moving towards a total return profile for 2023 in excess of 6%, with virtually no volatility, beating most asset classes this year. The fund has a negligible duration profile and a collateral pool entirely made up of investment grade credits. All else equal, we should see the fund’s 30-day SEC yield move higher towards its portfolio yield of 6.2% as time passes by. Expect a low volatility profile with an increasing 30-day SEC yield here. It has been more than a year since we last covered this name, and in today’s uncertain market MINT delivers a high total return with an almost inexistent volatility. Buying this name and waiting out the market at a 6% yield might be boring, but will prove to be rewarding in our opinion.

Read the full article here