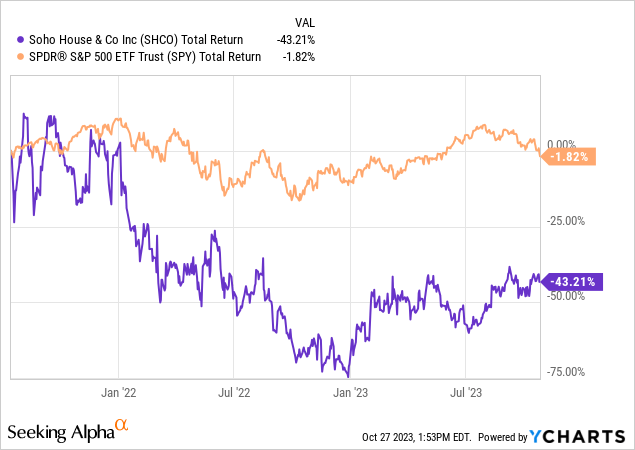

Since coming public in 2021, shares of Soho House & Co (NYSE:SHCO) have not proved a good investment. Since inception, SHCO has delivered a total return of -43.2% compared to a -1.8% total return posted by the S&P 500.

SHCO has built a business around an innovative membership based concept. The company has delivered strong growth but remains unprofitable. SHCO carries a significant amount of debt on its balance sheet and thus remains a high risk investment.

[object HTMLElement]

Company Overview

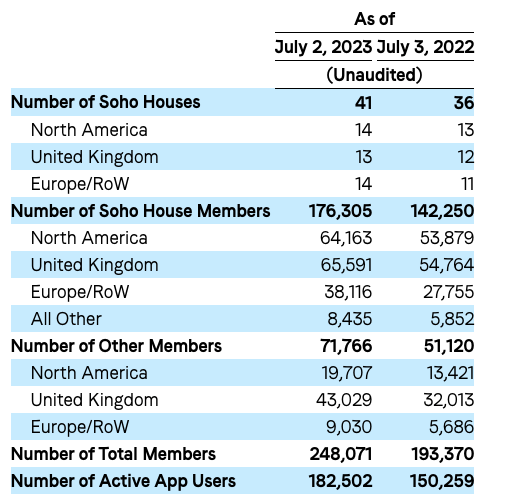

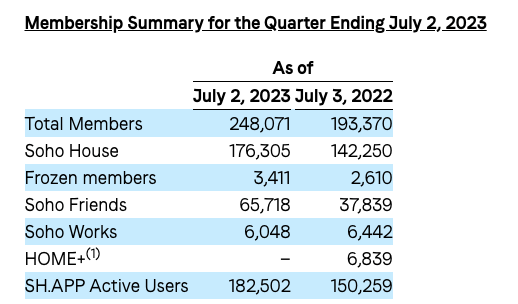

SHCO is a hospitality companies operating a leading private membership platform which includes hotels, clubs, and working spaces. As of Q3 2023, the company had 248,071 total members. Additionally there are currently 95,000 people on the waiting list, a number which represents an all-time high.

~30% of revenue comes from membership dues while 43% comes from in-house revenues (primarily food and beverages) and the remaining 27% comes from other sources including Soho Works and stand-along restaurants.

SHCO operates 41 Soho Houses across the globe including 14 locations in the North America and 13 locations in the United Kingdom. The remaining 14 locations are across Europe and the rest of the world.

The price of a Soho House membership with access to all houses is ~$5,000 per year but prices vary based on the primary location. The company’s cheapest membership option is a Soho Friends membership which costs $130 per year and includes special rates on bedrooms and full access to Soho Houses when staying.

SHCO Q3 Earnings Release SHCO Investor Presentation SHCO Investor Presentation

High Growth Story

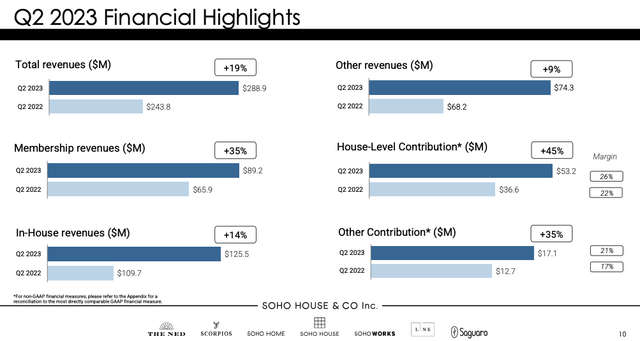

SHCO is a high growth story. For Q2 2023, SHCO reported total membership growth of 28.3% on a year-over-year basis. Total revenues increased 18.5% on a year-over-year basis while Adj. EBITDA more than doubled year-over-year as margins improved.

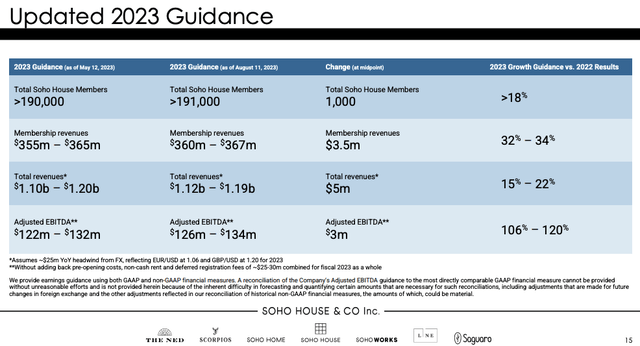

Consensus analyst estimates currently call for the SHCO to grow 2024 revenue by 16.6% and 2025 revenue by 10.3%.

Given the very high waiting list of 95,000 members, I believe SHCO will be able to exceed those revenue growth estimates (assuming we avoid a recession.)

Additionally, given the SHCO only operates 41 Soho House locations currently means there is significant growth opportunity in terms of new locations.

SHCO Investor Presentation SHCO Investor Presentation Seeking Alpha

Lack of Profitability

Despite significant revenue growth over the past few years, SHCO has yet to turn a profit on an annual basis. However, results have been improving and SHCO reported a loss of just $2.6 million or $0.01 per share during Q2 2023 compared to a net loss of $81.9 million or $0.41 per share during the same period a year ago.

Consensus analyst estimates currently call for the company to report a loss of $0.10 per share in 2024.

Seeking Alpha

High Leverage

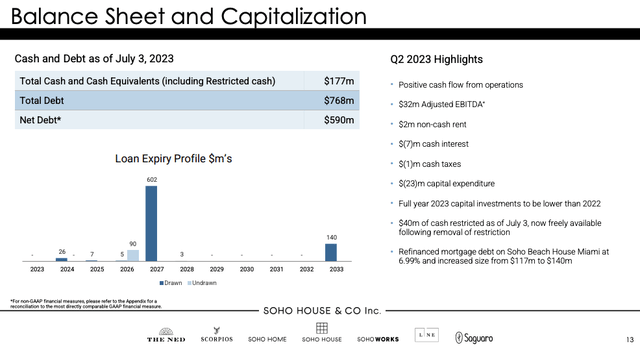

SHCO has total debt of $768 million and net debt of $590 million. Using the midpoint of FY 2023 Adj. EBITDA guidance of $130 million implies a net leverage ratio of 4.5x.

4.5x leverage represents a relatively high amount of leverage for any company. While I do believe the company will be able to grow into this leverage and de-lever overtime via EBITDA growth, the high level of leverage creates substantial risk in the event of a recession.

Generally speaking the hospitality industry is highly cyclical as it tends to be a highly discretionary spending choice for most customers. Moreover, SHCO requires customers to pay a high annual fee which may become more of a challenge for consumers in the event of an economic downturn.

SHCO Investor Presentation

Relative Valuation Analysis

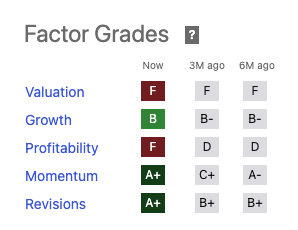

SHCO receives a Seeking Alpha quant valuation score of F. I believe that SHCO is more reasonable valued than this score indicates.

While SHCO is not attractive based on earnings multiples, there are some measures by which SHCO appears more reasonably valued vs its peers.

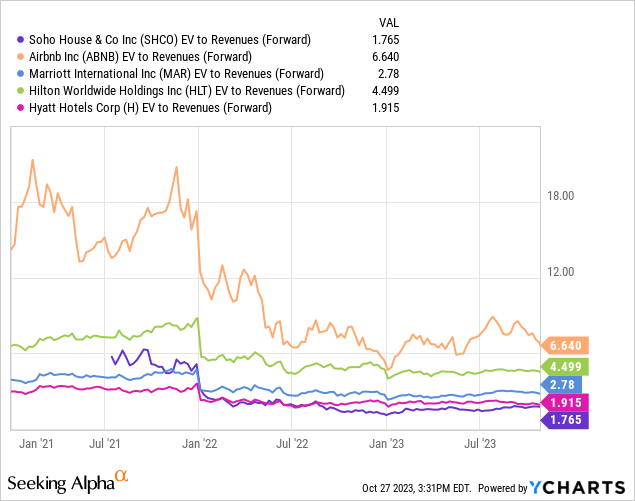

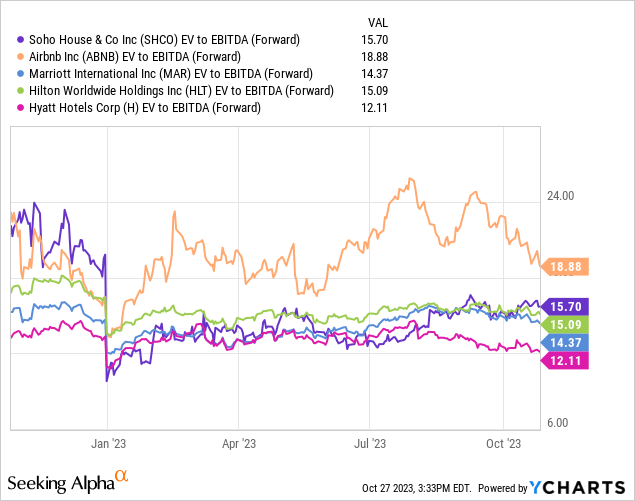

Based on EV to sales, SHCO trades at 1.7x compared to 6.6x for AirBnb (ABNB) which I think represents a highly relevant comp given the high growth potential. However, on a forward EV/ EBITDA basis SHCO is valued at ~15.7x compared to 19x for ABNB and mid-teens multiples for slower growth hotel chains such as Marriott (MAR), Hilton (HLT), and Hyatt (H).

That said, I believe SHCO is still in the early stages of a massive growth opportunity given the company operates just 41 Soho House locations currently and has a waiting list that represents 38% of its current total member count. Comparably, even ABNB is a much more mature company so thus deserves to trade at a lower valuation.

Seeking Alpha

[object HTMLElement]

[object HTMLElement]

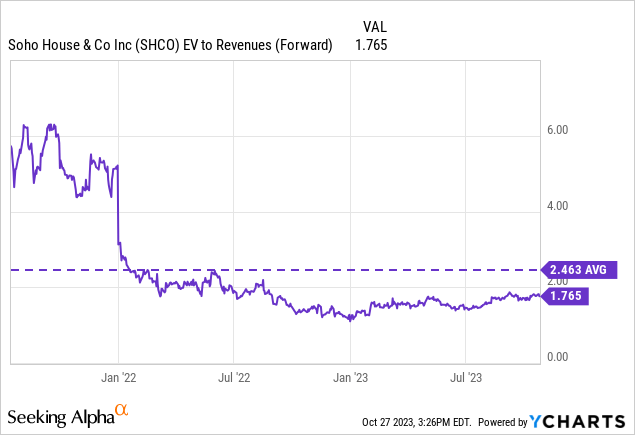

Historical Valuation Analysis

Given the fact that SHCO has not been profitable and generated negative EBITDA for a significant part of its history, I believe EV / Revenue represents the most reasonable historical valuation to consider.

As shown by the chart below, SHCO is trading significantly below its historical forward EV/Revenue multiple.

[object HTMLElement]

Conclusion

SHCO has an attractive business model with a significant part of revenue coming from membership dues. The company has experienced very rapid membership and revenue growth but has yet to fully turn the profitability corner.

I believe SHCO will continue to experience strong growth in the coming quarters and years as the company has a lot of room to expand given its relatively small size and unmatched global network of clubs.

My biggest concern with SHCO as a potential investment is the significant debt load. I view the 4.5x net leverage ratio to be very high for a company that operates in a highly cyclical industry. Moreover, SHCO is still in the process of becoming profitable. That said, if the company is able to deliver strong revenue growth in future I believe it can grow into its current debt load.

Based on metrics such as EV / Revenue and EV / forward EBITDA, I believe SHCO is attractive relative to more mature slower growing peers.

Due to my concerns around leverage, I am initiating SHCO with a hold rating.

I would consider upgrading SHCO if the company is able to grow into its current debt load through EBITDA and earnings growth. Additionally, I would like to see SHCO turn the corner and become profitable on a consistent basis.

Read the full article here