Life Time Group Holdings (NYSE:LTH) shares fell nearly 20% last week and have now declined 37% since my February article, so I’ve decided to revisit the name. What is particularly interesting here is that while the stock chart is ugly, the 2023 full year EBITDA guidance Life Time provided last week is up 21% from the guidance which was in place in February. With the stock having plummeted but guidance being significantly higher, there has been substantial multiple compression, setting up a potentially interesting opportunity for investors.

Current Results

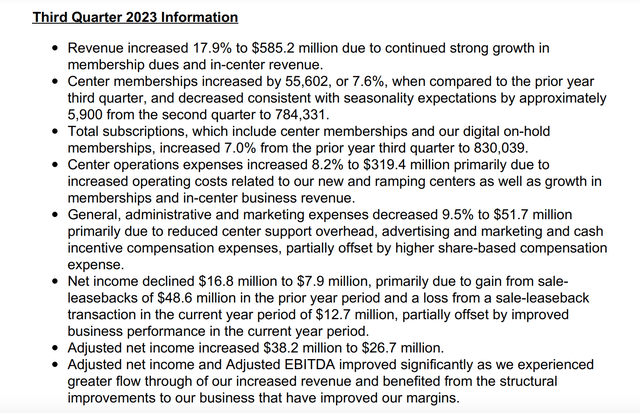

3Q23 Results (3Q23 Earnings Release)

As you can see, revenue performance was strong year-over-year on the back of both membership and pricing increases. The robust top-line performance coupled with a largely fixed cost structure lead EBITDA to increase just over 100% year-over-year.

However, as you saw from last week’s nearly 20% share price decline, there are items which are concerning to investors including:

- Quarterly decline in memberships. While management attributes this to normal seasonality, this is difficult for investors to verify because the company has only been public since October 2021. In 2021-22, membership was increasing sequentially on the back of the pandemic rebound, whereby members who had cancelled were returning to the gym.

- Life Time has historically relied on net lease real estate companies to provide capital for expansion via sale-leaseback transactions. The significant rise in interest rates has made the terms of sale-leaseback transactions much less attractive than in 2019-2022 as cap rates have increased, leading to reduced proceeds/higher rent expense per club. Further, many net lease companies have increased the annual escalators on leases 40-75 basis points over the past ~18 months, which shows up as higher expense growth. For its part, management notes that the company will be patient in executing sale-leaseback transactions and that growth can be self funded. Of course there is a tradeoff here as keeping new locations on the balance sheet relies on debt financing which has also become more expensive.

- Similar to the first bullet, the market is somewhat concerned that the dramatic price hikes (20+%) over the past year or two will ultimately prove unsustainable and that a tougher economy could lead to increased member churn. While price hikes and membership growth have had an outsized impact on EBITDA on the way up, the same would be true if revenue were to decline (fixed costs) which could lead to a more pronounced decline in EBITDA.

Merits of an Investment in Life Time

Here are what I see as the key positive attributes of an investment in Life Time:

- As discussed in my February article, Life Time is a beneficiary of a large number of gym closures as a result of the pandemic (which led to the permanent closure of 20-25% of gyms in the US).

- While the pandemic has faded and there have been some new gym openings as activity has normalized, gyms are a capital intensive business. A high-end gym requires a multi-million dollar capital outlay. As we’ve seen with Life Time, rising interest rates have increased the cost of capital, which will likely slow the pace of gym openings. Further, the vast majority of the industry is small local operators with limited access to capital.

- With just ~170 locations, there is a significant growth opportunity ahead for Life Time, which seeks to add 10+ locations per year for the next several years.

- While the stock was expensively priced earlier this year, the valuation has become much more reasonable (discussed in the next section) given the share price decline despite improved results.

Valuation

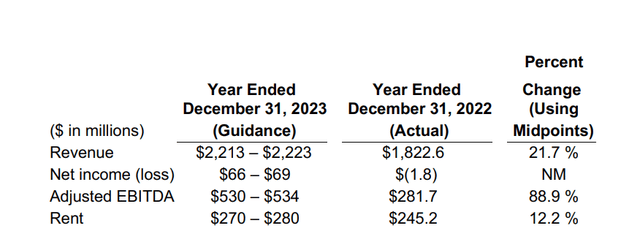

Below I show management’s current full year guidance, which was disclosed last week in the 3Q23 earnings release.

Current 2023 FY Guidance (3Q23 Earnings Release)

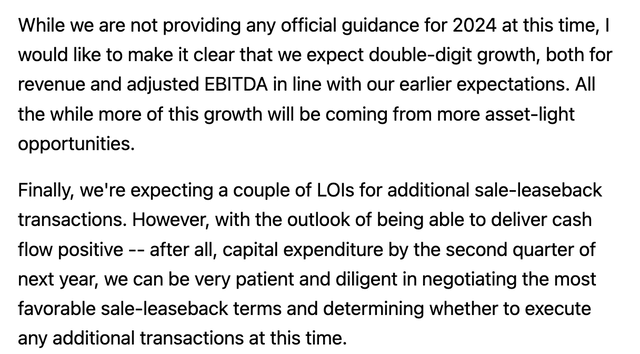

In addition, management provided the following commentary regarding the outlook for 2024:

2024 Expectations Commentary (3Q23 Conference Call Transcript from Seeking Alpha)

I think the company will hit some headwinds related to consumer spending (curtailing ability to increase price and likely slowing membership growth) over the next year, so I don’t give any credit for growth in 2024. Instead, in my analysis below, I simply use the low end of 2023 expected results as the basis for my valuation.

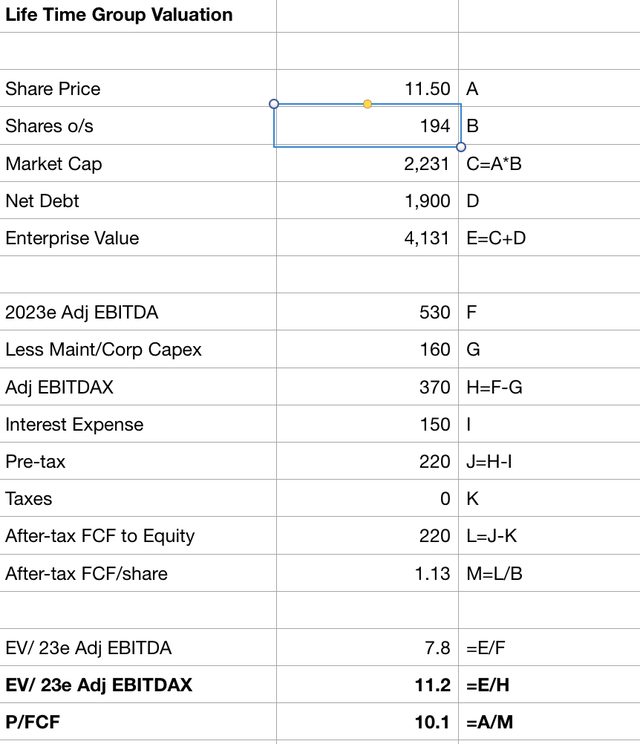

Life Time Valuation (Company Filings; Author Estimates)

As we sit today, Life Time trades at ~10x free cash flow to equity on a maintenance capex basis (i.e. not including the capital expenditures associated with new gym openings). While the price hikes of the past couple years are not sustainable, over the medium term, I think the business should be able to price in-line with inflation with an additional boost from adding net new members per club. All-in 3-5% growth in same store free cash flow per club seems a reasonable expectation. I consider 10x free cash flow to be a fairly attractive price for this level of expected same store growth.

In addition, purchasers of shares will benefit from having management invest the free cash flow generated by the business into opening new gyms, which I expect to create additional value for shareholders in the medium term.

With an improved market position following competitor closures and significant growth potential, I think 15-18x FCF (on a maintenance capex basis) is a reasonable fair value for Life Time shares (the company has traded between 12-24x FCF since coming public). This suggests a fair value of $17-20 per share, implying 47-74% upside potential.

Risks

- Operating leverage – as I mentioned in the article, while revenue growth drives an outsized impact to EBITDA on the way up, the same would be true on the way down. Should economic weakness cause members to churn and/or force the company to discount pricing, this could cause a significant decline in EBITDA.

- Financial leverage – as we sit today, Life Times has net debt-to-EBITDA of 3.6x. Taking into account the company’s lease obligations, the company has fixed charge coverage of ~2.0x. While this is manageable, should the company experience negative operating leverage and/or rising interest rates, things could get a bit tight.

Conclusion

Considering both the positives and the risks, I’ve taken a small position in Life Time shares. Should we see continued positive operating momentum (without a corresponding increase in share price), I may increase my position.

Read the full article here