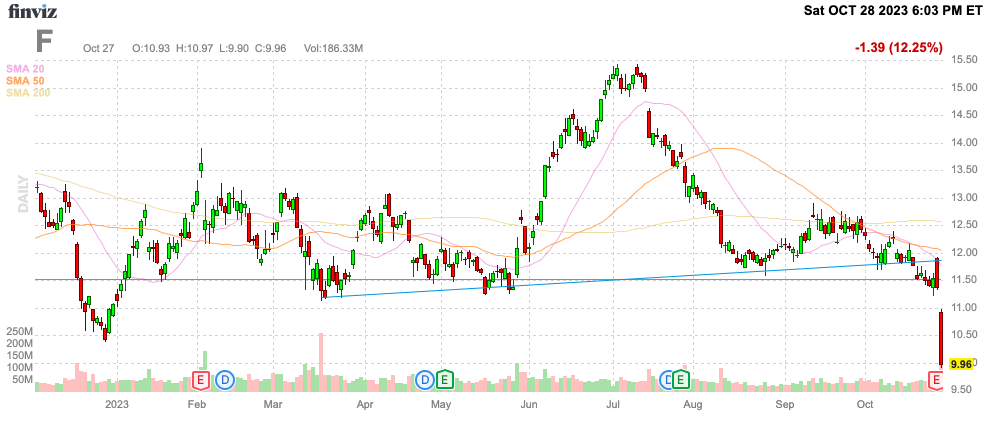

Ironically, Ford (NYSE:F) survived the UAW strike just fine, but the stock collapsed after weak Q3’23 results and the removal of guidance for 2023. The move is odd considering the market already knew the auto manufacturer faced a dicey period with production limited and a tentative union deal not ratified yet. My investment thesis is far more Bullish now with the stock dipping below $10 after reaching nearly $15 during the Summer and the company appearing to avoid the path to ruin.

Source: Finviz

UAW Impact

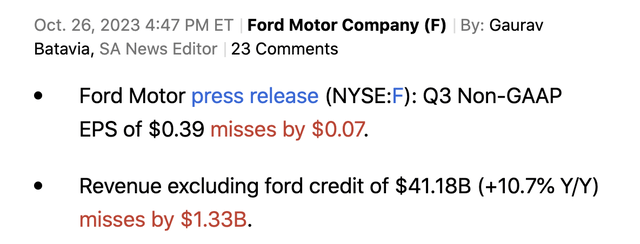

Ford reported Q3’23 results that missed analyst targets on the top and bottom line as follows:

Source: Seeking Alpha

The auto maker missed revenue targets by $1.3 billion. Per the company, the strike cost Ford $100 million in EBIT during the quarter and trimmed 80,000 units from production.

Ford is now forecasting a $1.3 billion EBIT impact for the year. The company previously forecast hitting the goal of $11 to $12 billion in adjusted EBIT for the year, but the strike hit will limit Q4 profits.

The stock collapsed on Friday due to Ford withdrawing full-year guidance. On the Q3’23 earnings call, CFO John Lawler highlighted a plethora of short-term issues caused by the strike making Q4 results difficult to predict:

With that said, the UAW strike created significant uncertainty regarding our full-year results, and even though we have reached a tentative agreement and our employees are starting to return to work, we have withdrawn our guidance for the year. This is in part because of the continued disruption in the industry with the ongoing strikes, the follow-on impact to our shared supply base, the ramp up of production in our plants and at our supplier partners, as well as other ancillary effects.

In essence, the market shouldn’t be surprised that Ford isn’t sure on the updated guidance. Not to mention, the UAW deal isn’t even ratified yet and management is wisely focusing on lost profits from the stock without pointing out the ongoing strong profit potential.

The UAW and Ford apparently reached a tentative deal calling for 25% wage hikes over a 4-year period plus a cost-of-living adjustment. The amount is far below the 40% requested by the UAW, but the devil will definitely be in the details of the wage and benefits hikes, including a much higher rate of up to 68% for new employees.

The strike has lasted about 6 weeks so far since the initial start on September 15 with multiple assembly plants for Ford shutdown from making Super Duties, Explorers, and Broncos. Analysts have apparently forecast ~$4 billion in additional employee costs for all 3 U.S. auto manufacturers from the potential UAW deals amounting to somewhere less than $1.5 billion for Ford.

The company was already expected to absorb higher costs on an annual basis due to normal wage pressure. The deal appears to avoid some of the excessive cost fears, though Ford already has higher costs than EV only competitors like Tesla (TSLA).

Slowing EV Focus

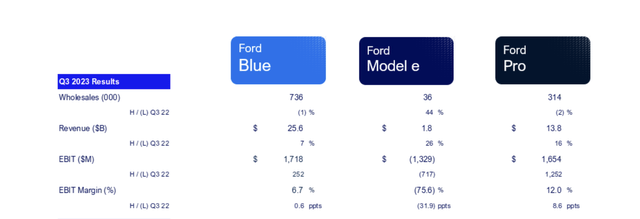

Ford lost $1.3 billion during the quarter on the EV business. The company is slowing capacity expansion due to the lower EV growth.

Source: Ford Q3’23 presentation

The company only sold 36,000 EV units during Q3 for $1.8 billion in sales. Ford lost ~$36K in adjusted EBIT per each EV unit sold.

The auto manufacturer has both reduced production plans for the Mustang Mach-E and delayed the second BlueOval SK JV battery plant in Kentucky. The company is evaluating plans for the BlueOval Battery Park Michigan plant and claims to have pushed out $12 billion in EV spending.

Ford claims customers are increasingly uninterested in paying premiums for EVs when viable gas and hybrid vehicle options exist. The company can dramatically boost profits by slowing EV spending while focusing design on building Gen 2 and Gen 3 EVs with cost optimization for better economics.

Besides, the company states F-150 hybrids are in more demand where the company can sell the truck at premium prices due to the fuel savings and back up battery functionality for job sites. Though, the market doesn’t necessarily want to hear Ford slow down the transition to EVs, investors should want Ford to make these moves where beneficial, especially considering the company now has the technology and knowledge to become fully EV focused when the market is ready.

At $10, the stock only has a market cap of $40 billion for a company with $11+ billion in EBIT potential before the UAW strike impact. In addition, Ford is facing $4+ billion in EBIT losses from the struggling EV business providing a substantial earnings boost from removing those losses from the business.

The stock only trades at 3.5x EBIT targets, excluding the UAW impact. In addition, the slowdown in EV spending should quickly cut those losses in 2024 pushing the EBIT even higher.

Ford would actually generate $15+ billion in EBIT without these initial EV losses. The company didn’t provide any updated EV EBIT profit targets, but Ford likely pulls the profitable target day forward by pushing out $12 billion in costs.

Takeaway

The key investor takeaway is that Ford is just far too cheap here. The auto manufacturer avoiding some of the dire outcomes of the UAW strike is a huge positive, yet the stock has fallen to recent lows due to fears surrounding the short-term impacts to the business.

Investors should use the stock weakness to own Ford, though everyone needs to keep an eye on the actual details of the ratified UAW contract.

Read the full article here