Perion Network (NASDAQ:PERI) has had a rough go of it lately with shares down about 30% in the last six weeks, from ~$35 to $25. There are risks associated with an investment in Perion, but they are far outweighed by other factors, and the company is now extremely undervalued.

Business Model

Buyers And Sellers – One, Multi-Channel Platform

Perion is a “global, multi-channel advertising technology company that delivers synergistic solutions across all major channels of digital advertising – including search, social media, display, video and connected TV (CTV). These channels converge at Perion’s intelligent HUB (iHUB), which connects the Company’s demand and supply assets[.]” (Source: Company’s September 6-K, p.2)

Perion serves both buyers and sellers of digital advertising on one unified platform. The company views its “agility” in following advertisers’ budgets between different channels as a competitive advantage.

SORT

SORT showcases Perion’s ability to develop innovative technology. It stands for “Smart Optimization of Relevant Traits.” SORT is an AI-based ad targeting solution that delivers better click-throughs than cookies while respecting a user’s privacy. It does not collect or store any user data.

SORT’s superior performance on click-throughs “has been validated through real-time comparison tests completed by Neutronian, a respected third-party research firm.” (Source: September 6-K, p.2) In August, SORT won a prestigious award from Digiday for Best Cookieless Identification Technology for an ad campaign Perion did for Mercedes-Benz.

Growth and Cash Generation

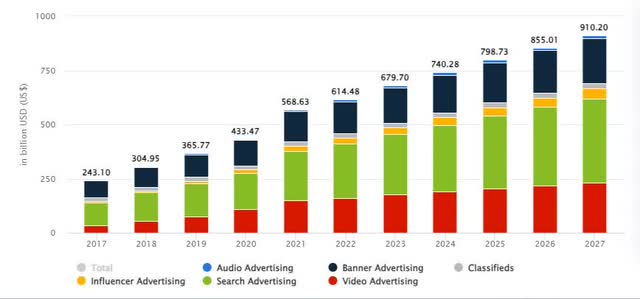

Digital Advertising Market

Perion operates in the digital advertising market. Per Statista, this market will grow from $679B in 2023 to $910B in 2027 across multiple channels, which is about 8% annually.

Digital Advertising – Worldwide (Statista)

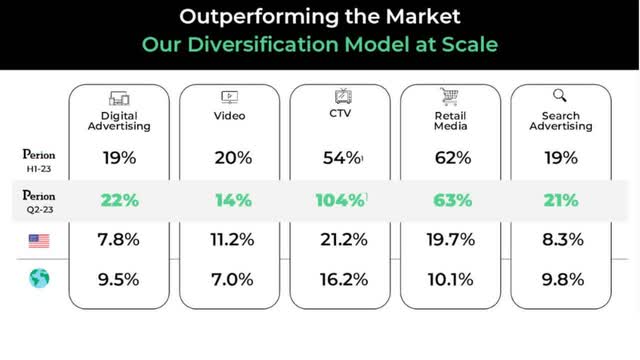

Market Share

Perion is growing faster than the digital advertising market, which means they are taking share.

Growth Vs. Digital Ad Market (Company’s Q2 Investor Presentation)

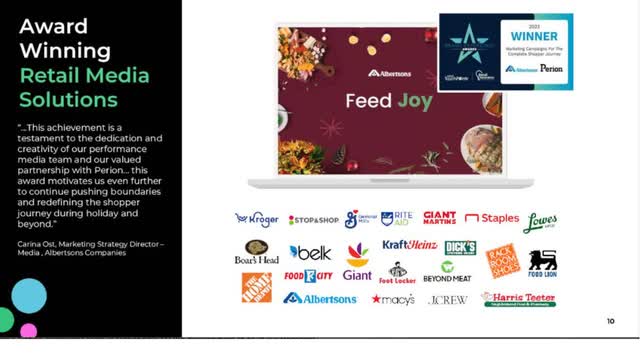

In the fast-growing retail media segment, Perion has partnered with an impressive list of blue-chip logos.

Perion Retail Media Customers (Company’s Q2 Investor Presentation)

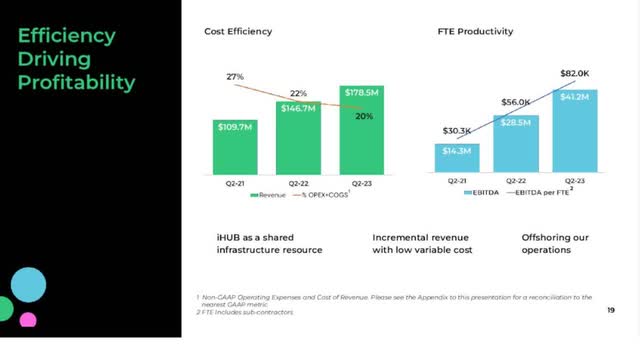

Keeping Costs Down

Perion has been scaling its business rapidly, but it has also been keeping costs in line, demonstrating leverage in its model.

Perion Cost Control (Company’s Q2 Investor Presentation)

In the last two years, Perion has reduced OPEX + COGS as a percent of revenue by 7%. Companies will often measure margin improvements in basis points, i.e., 1/100 of a percent. Using basis points as the yardstick, Perion has improved this metric by 700 points in just two years.

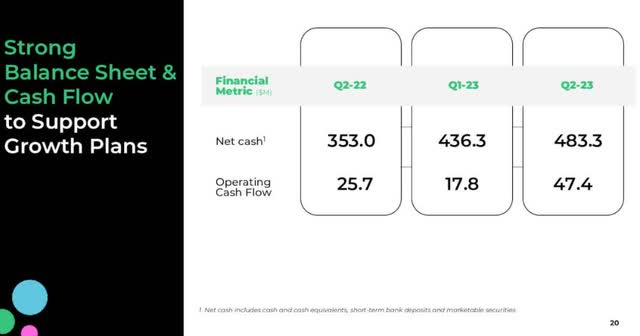

Cash Generation

This growth and efficiency has turned Perion into a cash-generating machine. The following slide is one of the most powerful I’ve seen in a company presentation.

Perion’s Cash (Company’s Q2 Investor Presentation)

In the last 12 months, the company ($1.2 billion market cap) has added $130M to its immense cash pile, which now stands at $483 million. (Note: Q1 is typically a slow quarter, and it was also impacted by an $8 million collection pushed from Q1 to Q2, otherwise the operating cash flow would have been smoother.)

This is net cash, as Perion has no long-term debt. With ~49 million diluted shares outstanding, $483 million is almost $10/share of net cash against a recent share price of $25, giving Perion a miniscule EV/OCF of ~6x.

The Risks

So why would a company that is (1) growing rapidly, (2) taking share in a high-growth market, and (3) generating gobs of cash be valued by the market at such a low multiple? There are two major risks, and a handful of smaller ones, that could explain why the market is penalizing Perion.

Two Big Risks

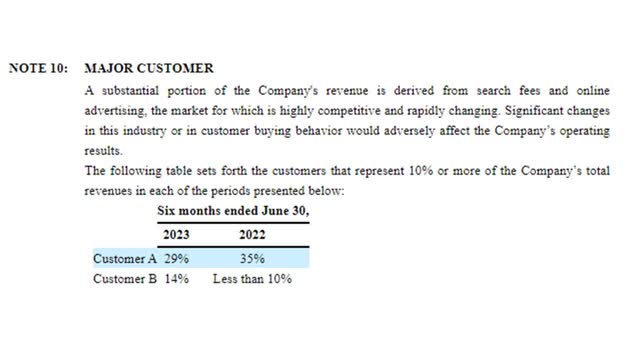

Customer Concentration

Microsoft is Perion’s biggest customer.

Perion Customer Concentration (September 6-K, p.F-19)

Perion’s contract with Microsoft for Bing runs through 2024. There is always the risk that Microsoft could end the partnership, but there are many factors which suggest this is not likely.

- The two companies have worked together since 2010

- The previous renewal in 2017 was for 3 years, while the 2020 renewal was extended to 4 years

- Microsoft’s Advertising division named Perion’s Search subsidiary, CodeFuel, its 2021 Supply Partner of the Year

- Perion’s current CEO, Tal Jacobson, was the head of CodeFuel from 2018 through 2023, and he was a key player in building the relationship with Microsoft

- Perion added 159 new Search Advertising publishers in Q2 (up 28% YOY)

- Perion’s search revenue was up 22% YOY in Q2, compared to 10% for Microsoft recently, so Perion is outpacing the rest of Microsoft search

Although anything could happen at renewal time, a customer does not typically end a long-standing relationship with a supplier unless they are dissatisfied. The most likely result of the renewal discussions in 2024 is that the relationship is extended again.

If Microsoft is happy with Perion’s performance, the 2024 renewal could actually be an opportunity for Perion, rather than a risk. The companies could broaden their relationship, or agree to compensation terms that are more favorable to Perion (which currently takes an estimated 75%-85% of the Bing search advertising revenue it brings in).

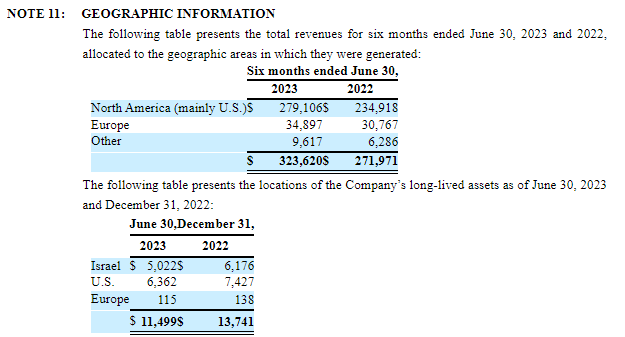

Israel-Hamas War

This article will not address the politics around the Israel-Hamas War. From an investment standpoint, the war could impact Perion as the company is based in Israel.

Perion Geographic Risk (September 6-K, p.F-19)

97% of Perion’s business is in North America and Europe. The “Other” category from the table above is not broken out by country, but it does put a ceiling on Perion’s business in Israel at 3%.

The bigger issue potentially is the location of employees and long-lived assets. Will the conflict impact the ability of Perion to conduct business? Unfortunately, the company has not provided a statement as to business continuity as other companies with substantial Israel operations have done.

This risk is difficult to quantify, but since Perion is not an industrial company with a plant and other fixed assets, it seems likely that the “long-lived assets” are also reasonably portable, and the business can continue with minimal interruption regardless of how the war unfolds.

Other Risks

CEO Turnover

The previous CEO, Doron Gerstel, had a very successful 6-year tenure from 2017 to 2023, and he’ll be a tough act to follow. Tal Jacobson has only been in the role since August, and he did not have CEO experience at a public company prior to joining Perion.

On the positive side, Jacobson was the General Manager at CodeFuel from 2018 to 2023, and he played a key role in building the Microsoft relationship. The Board must have had a good view of his body of work over five years, and they chose not to pass him over for an external candidate, or one with more experience. Also, Gerstel is still on the Board and can provide guidance to Jacobson as he learns the role.

Equity Raise Hangover/Acquisition Risk

Perion raised $180 million from selling equity at $21.50/share in December of 2021. Company followers believe this was done to fund a potential acquisition that did not pan out. An equity raise at $21.50 makes it a challenge to buyback shares now even though the company is (1) extremely undervalued and (2) they have plenty of cash to do a buyback. “Sell low, buy back higher two years later” is not going to win management any capital allocation awards.

With all of this cash lying around, there is a risk of an ill-advised acquisition. Most acquisitions destroy shareholder value, and Perion’s cash pile is so big that a smaller, tuck-in acquisition wouldn’t “move the needle.” The cash pile may be easier to explain right now with higher short-term interest rates. The company earned $7.1 million interest on that cash in Q2. But if interest rates drop, and the cash is earning next to nothing, the pressure to do something with it could be hard to resist.

Slowing Growth/Recession

Perion guided for “only” 16% revenue growth in 2023. While this would be a great number for most companies, Perion investors may be concerned because it has been growing faster recently (28% CAGR Q2 ’21-23).

Perion has a history of conservative guidance, and they seem to “beat and raise” nearly every quarter. The year is off to a good start with 19% revenue growth YOY for Q1-Q2 combined. If growth does turn out to be 16% this year, that would still be a solid result, especially with a 6x EV/OCF multiple.

If there is a recession, an advertising company may not seem like a good place for capital. A recession would impact Perion, but digital channels will likely fare better than traditional media. Also, recent data shows that digital ad spend is still holding strong, with more growth forecast in 2024, and major ad buyers like LVMH, Kellogg’s and Nestle saying they plan to ramp up campaigns in support of their brands.

The Bottom Line

Is it possible that one of these risks could hit the company, or multiple risks at the same time? It’s possible, but the risk-reward sets up favorably here.

As a quick check, let’s look at a highly unfavorable scenario. Assume that Microsoft ends the search deal in 2024, and that Perion has zero growth in operating cash flow for the remaining 5+ quarters of the deal (a conservative assumption in light of historic growth trends). At that point, the company could be sitting on close to $15/share of net cash. And even if operating cash flow drop 25% post-Microsoft, we would still be looking at a ~5x EV/OCF multiple at $25/share.

And what would investors be getting for this rock-bottom valuation? A company with an efficient, one-stop digital advertising platform, a blue-chip customer base, and a track record of growth and innovation.

And if the worst doesn’t happen? What if Perion continues to grow at 15-20%, with leverage in the model generating cash at an even higher rate? And what if the market gives the company at 10x multiple? It doesn’t take aggressive assumptions to see the share price doubling in 2-3 years.

The bottom line is that Perion is oversold. The market has overreacted to a number of perceived threats and created a great opportunity for investors here at 6x EV/OCF.

Read the full article here