AAON: Investment Thesis

Share price action –

Back on Dec. 22, 2021,with the AAON, Inc. (NASDAQ:NASDAQ:AAON) split adjusted share price at $52.00, I published the article, “AAON: ‘Mr. Market’ Is Showing Irrational Exuberance”, and gave the stock a Strong Sell rating. From then until my subsequent article on June 29, 2022, the share price dropped by over 30% to $34.94, compared to a fall of ~16% in the S&P 500 over the same period, justifying my Strong Sell rating. That next article, “AAON: Looking Back, Looking Forward – Still Too Dear“, maintained a Strong Sell rating but with a very different outcome. The stock subsequently traded as low as $34.70 through October 2022, but with emergence of strong EPS growth, far above analysts’ estimates, the share price then grew progressively to a high of $71.39 by August 2023. That $71.39 obviously was driven by a degree of exuberance, as the share price has subsequently declined to the present $53.74 — only 3.35% above the $52.00 level from the time of my December 2021 article.

About AAON Management –

On May 7, 2020 AAON announced:

“…Norman H. Asbjornson, Chief Executive Officer and Founder of AAON, Inc., will transition to the role of Executive Chairman, effective May 12, 2020 […] Gary D. Fields, President, will assume the role of Chief Executive Officer (in addition to his current position of President)…”

I never had any doubt from earnings calls Mr Fields could “talk the talk”, particularly around marketing, but he has also shown he can “walk the walk” in all areas of management. The company has had a huge spurt in growth over the last 12 to 24 months, and this growth appears to have been managed well, with construction of additional production facilities, increased production to meet growing sales, retention and addition of skilled personnel, and product development, all necessary for delivering strong sales growth based on both price premiums as well as additional units sold.

Excerpted from AAON’s Q2-2023 earnings call transcript from SA Premium –

– Organic volume was up 16%, and on a two-year stack, it was up 27.6%. We’ve made great strides at increasing our production capacity to allow for this growth. Capital headcount was up 26.1% from a year ago, and up 18.2% from the end of 2022.

– Our operations team is doing a great job managing the robust demand by increasing production capacity quickly. In fact, production finally began to outpace bookings this quarter, allowing our backlog and lead times to fall, which we were happy to see… reflects the investments we have made in production capacity, including workforce, equipment and warehousing…

About AAON’s competitive advantages –

Comments by Mr Fields excerpted from AAON’s Q2-2023 earnings call transcript linked above.

– … believe the price premium of our equipment relative to the competition is in the high single digits, down from 15% to 20%… making the value proposition of our equipment even more compelling, helping drive further share gains. At the same time, we were able to expand profit margins.

– later this year, we will be rolling out a new branding of our highest performing package solutions ever. The industry’s most versatile line of commercial, fully electric, air source heat pumps. We will call it the ALPHA Class…Operating down to zero degrees Fahrenheit, there is no other commercial air source heat pump like it on the market, and the ALPHA Class retains the superior quality of manufacturing that the AAON brand exemplifies. This new equipment will revolutionize the industry, paving the way for a cleaner environment while maintaining the comfort of AAON’s premium performance.

– In the second quarter, we held the grand opening of our new marketing building, also known as the Exploration Center. Our products are best in class in our industry, providing premium performance at the most attractive value proposition. This new building, located at our headquarters in Tulsa, displays market alternatives side by side with our products, showcasing the superiority of our equipment. This is an extremely valuable tool for our sales channel partners… the next thing that’s been compelling a lot of people to come in is the ALPHA Class unit … we’re actually in production on those units and have been for a bit. And so that story is beginning to resonate with people. We had a client in a couple of weeks ago, a very, very major client that’s got to replace the thousands upon thousands of units…their board has tasked them with becoming zero emissions, not net zero, but zero emissions… an electrified heating method is required to make that happen. And when you look at a wide swath of North America, our ALPHA Class units satisfy that need and we’re the only ones currently that do that.

– (question from Conference participant) …the pending regulations from the DOE on lowering, global warming potential refrigerants, that’s 2025, …how that’s going to impact you guys or you out in front as normally you are on these things and how significant is that to the industry? (Gary Fields)… we’re very far ahead of the curve on that. … we’re very close to having from two tons all the way to 240 tons completed with the new refrigerant. Very close.

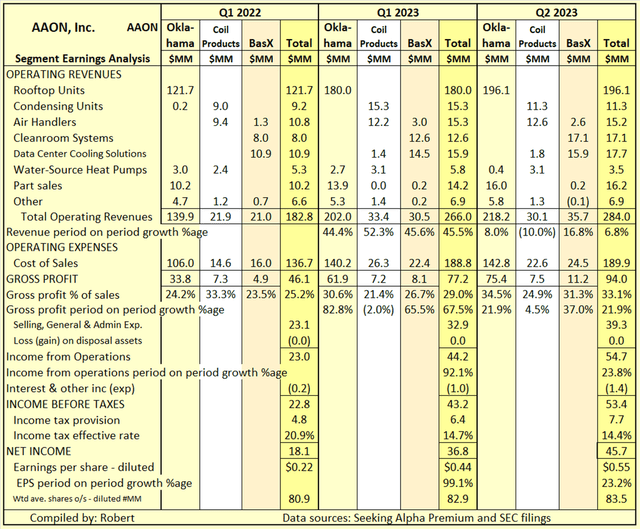

Table 1 below illustrates how AAON has grown EPS through a mix of revenue growth, gross profit margin growth, and economies of scale.

Table 1

Seeking Alpha Premium and SEC filings

Comments on contents of Table 1 –

- Twelve months Q1-2022 to Q1-2023 – Revenue for Oklahoma segment grew by 44.4%, but gross profit grew by 82.8% due to gross profit margin increasing from 24.2% to 30.6% Similarly for total segments, revenue grew by 45.5%, but gross profit margin increased by 67.5%, due to margin improvement. Despite a significant increase in SG&A expense, operating income growth of 92.1% exceeded gross profit growth of 67.5% due to economies of scale.

- Three months Q1-2023 to Q2-2023 – Revenue continued to grow strongly, except for Coil Products segment. Total gross profit grew by 21.9% for the quarter compared to total revenue growth of 6.8%, due to gross profit margins continuing to increase. Notably, Coil Products segment achieved 4.5% gross profit growth despite a decline of 10.0% in revenue for the quarter. Again, despite significant increase in SG&A in absolute terms, operating income grew at a faster rate than gross profit growth due SG&A as a percentage of revenue decreasing due to economies of scale.

Summary and conclusions:

My Strong Sell recommendations in previous articles related to my concern AAON share price was above fundamental value due to an excessively high multiple, not justifiable by future EPS growth based on SA Premium analysts’ consensus EPS estimates at that time. That concern was overturned by AAON’s strong EPS performance, far exceeding even analysts high EPS estimates. At the time of my Jun. 2022 article, analysts’ EPS estimates for 2023 ranged from a low of $1.37 to a high of $1.67, with consensus $1.52. Current analysts’ EPS estimates for 2023 per SA Premium range from $1.95 to $2.09, with consensus $2.04. I still have concerns the forward multiple of 26.66 based on current share price and analysts’ consensus EPS estimate for 2023, is overly high. At the same time, I am impressed by the ability shown by management to grow both the top and bottom lines over the last 12 to 24 months in particular. The positioning of the company to provide potential zero emissions solutions for customisers needing and wanting to achieve lower emissions, ahead of competitors, encourages me to believe the company might well continue to exceed analysts’ EPs estimates. Seeking Alpha Premium shows AAON Q3 earnings release due out post-market on Nov. 6 with consensus EPS estimate of $0.55 for the quarter (same as EPS of $0.55 for Q2). I would not be at all surprised to see a further beat, which could well provide a boost to the share price, which has declined by ~25% since that high of $71.39 on Aug. 2, 2023. Based on my expectation of continuing EPS growth, supported by a premium product addressing customer’s decarbonization issues, I believe AAON deserves at least a Hold rating. Based on the competence being shown by Management in operating the business, and results achieved to date, in the short term, at least, I rate the stock a Buy.

Read the full article here