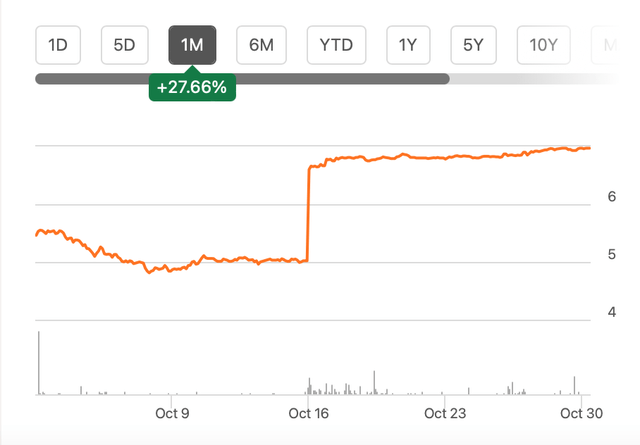

ADRs of the Colombian grocer Almacenes Éxito (NYSE:EXTO), more commonly called Grupo Éxito, have seen an interesting price trend since they started trading on US exchanges in late August. While the price was largely on a downward trajectory until earlier this month, it suddenly spiked mid-month. As a result, it’s now up by 26% since the opening price.

This is a good starting point. Here I take a closer look at the company to assess why its price rose so much and whether it matches the fundamentals for the company.

The company

But first, a look at the company. Grupo Éxito has a long history as a retailer, going back to 1905. It now has a 28% market share in its home market of Colombia. It also has a significant presence in Uruguay, with a 42% market share and a smaller 7% share in Argentina.

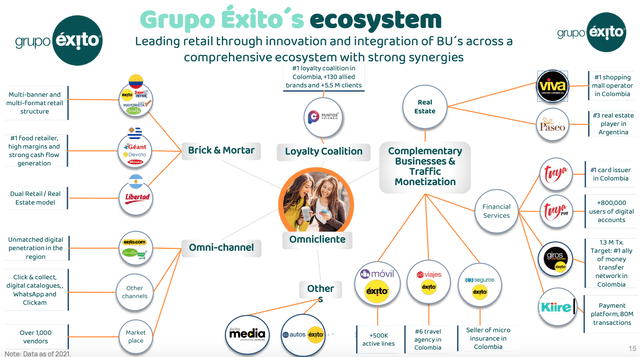

While grocery retailing is the dominant business for Grupo Éxito, it works through a fairly big ecosystem. Just within the grocery segment, it covers a range of brands, with its namesake brand Éxito being the leader in the home market. Under the Carulla brand, it provides premium products and SurtiMax is its fair-price retail arm. It also owns shopping malls, and issues credit cards as well as complementary services like travel and insurance (see chart below).

Source: Grupo Exito

Why has the price jumped?

The company’s financials aren’t entirely on point, however, as is discussed in the next section. But clearly, it is valued well, a fact that was revealed with the recent stake sale by the French supermarket Casino to El Salvador’s Group Calleja, which owns the grocery chain Supermercados Super Selectos, as Casino streamlines its debt-ridden business.

The sale happened at a valuation of USD 0.90 per share, which amounts to USD 7.20 per ADR. The actual price could be lower, depending on dividend payouts and asset transfers by EXTO. At the time the news was released, the price per ADR was USD 5.04, after which it showed a sharp uptick.

Even now, though, the price has risen to USD 6.99, which is less than the valuation at which the stake was sold. It’s close enough to the valuation indicated by the share sale, but it does imply a small upside. This is only part of the story though. Let’s now look at the financials to assess whether its price can rise further.

Price Chart (Source: Seeking Alpha)

The financials

Over the past decade, its revenues have grown at a compounded annual growth rate [CAGR] of 8.2%, though its net income has declined by 31.1% in USD terms.

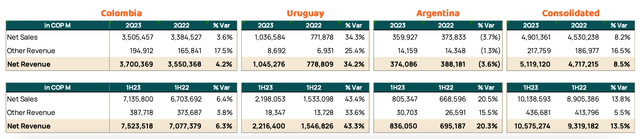

Even in Colombian Pesos, however, the same trend is visible for the first half of 2023 (H1 2023). EXTO’s revenues in its home currency are up by 13.5% year-on-year (YoY), significantly bolstered by growth in both Uruguay and Argentina, even as sales in its biggest market Colombia grew at a slower rate (see table below), as the economy slows down with high inflation plaguing it.

Revenue by Geography (Source: Grupo Exito)

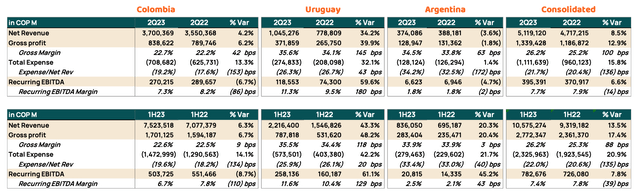

Despite the economic woes in Colombia, though, the company has been able to sustain its gross margins in the market, and overall, the margin actually improved in H1 2023 to 26.2% compared to 25.3% for the full year 2022. The recurring EBITDA margin, however, softened to 7.4% (H1 2022: 7.8%) on lower margins from the Colombian operations and higher taxes.

Profits by Geography (Source: Grupo Exito)

The net margin based on the group’s share in the result, also shrank 0.4% in H1 2023 from 1.4% in H1 2022. Net profits also declined in absolute terms by 69% YoY. This was partly because of one-time listing expenses but also a doubling in interest expenses, at a time of high inflation and rising interest rates. That said, while its interest coverage ratio has fallen from the healthy 4.9x in the second quarter of last year (Q2 2022), it is still alright at 2.2x even as of Q2 2023.

The outlook

The company’s earnings could also improve going forward, though. To assess where they might be, I assumed that revenues would grow at the same rate of 13.5% as seen in H1 2023. The net margin is assumed to be at 0.76%. This is higher than the margin of 0.4% for H1 2023, with the additional 0.36 percentage points obtained by adding back the one-time expense associated with the public listing of EXTO in the US. This results in a 37.7% YoY increase in net profit in Colombian Pesos, and an absolute value of USD 33.3 million.

This more than reverses the trend of the sharp fall in net income seen in H1 2023. But then it’s also an optimistic forecast considering that the Colombian economy is slowing down. Forecasters like Fitch Solutions have reduced the economy’s growth rate to 1.3% for 2023 from the earlier 2%. For context, the average growth rate of the economy has been 3.5% over the past five years.

While consumer staples is a resilient sector, which can hold its own in a softening economy, it is still likely to be somewhat impacted. There’s a very particular reason why I’ve made the more optimistic estimate, though. And that is to determine its market multiples, which I will talk about next.

The market multiples

EXTO’s TTM P/E is exceptionally high at 418.5x. But if the forward P/E looks more reasonable, there can still be a case to buy it. My estimates yield a forward P/E of 34.8x. This is of course a far more palatable number. But it’s still significantly higher than the median forward P/E of 17.6x for the consumer staples sector.

At the same time, the company’s TTM and forward P/S are low at 0.2x compared to 1.05x for the sector. This indicates a significant increase in the share price is possible.

What next?

Essentially, the market multiples don’t give a clear indication of where the stock can head next. While the P/S points towards a rise, the P/E shows a potential decline. In this case, I believe that the best signal is indeed the valuation indicated by Casino’s selling price to Calleja. And that price indicates that the stock is almost fairly valued right now.

The company does have a whole lot of potential going by its expansive operations. Its sales growth is good too. The stumbling block has been its minuscule earnings as a proportion of revenues. But as the Colombian economy in particular picks up again and inflation subsides further, I reckon there’s potential for an uptick in earnings here. That remains to be seen, though. For now, I’m going with a Hold on EXTO.

Read the full article here