This year, I have been fortunate enough to find some really interesting prospects in the banking industry. While some of the companies have been prospects that I would not touch with a 10-foot pole, others have warranted really optimistic assessments. One of those that deserve to be near the top of the list in terms of the opportunity that it offers is Premier Financial Corp. (NASDAQ:PFC). With a market capitalization of only $609 million as of writing, Premier Financial is a pretty small bank. Its overall financial track record has been a bit mixed in recent years. However, throughout 2023, management has succeeded in continuing the growth of the deposits at the institution. Shares are cheap relative to earnings and book value. And uninsured deposit exposure, on an adjusted basis, is quite low. Add all of these factors together, and we have a very solid ‘buy’ candidate at this time.

A bank that’s close to home

Located in Youngstown, Ohio, Premier Financial is quite close to home for me. It’s less than an hour from where I live and where I have lived for the better part of over 20 years. Unfortunately, like every city within Ohio with the exception of Columbus, Youngstown has seen far better days. The refusal of the region to adapt to the economy of tomorrow and its insistence on clinging to the past has done it far more harm than good. But Premier Financial does seem to be evidence that even some of the most challenged parts of the country can have something of an attractive value in them.

Although Premier Financial’s bank, Premier Bank, is based out of Youngstown, the firm actually has a sizable number of offices in its network. It has 74 full-service banking center offices, 12 loan offices, and two wealth offices split between Ohio, Michigan, Indiana, Pennsylvania, and West Virginia. As you might expect, the institution focuses primarily on community banking activities. In short, it accepts deposits from the general public and then allocates those deposits toward other parties in the form of loans. Examples of the loans that it gives include those dedicated to the purchase or repair of real estate, the purchase of homes, home improvement, the purchase or financing of businesses, and more. The bank also invests some of its funds not only in US Treasuries, but also in other securities such as residential collateralized mortgage obligations, corporate bonds, and more.

The enterprise does have other operations as well. For instance, it has its own wholly-owned insurance subsidiary that provides property and casualty insurance, life insurance, and group health insurance. It has a risk management firm indicated to insure the institution. On top of this, it has a subsidiary called PFC Capital that offers mezzanine funding for customers.

Author – SEC EDGAR Data

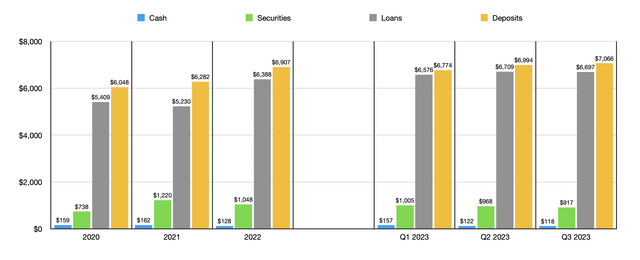

Over the years, management has done a pretty good job of growing the institution. The value of deposits, for instance, has grown from $6.05 billion in 2020 to $6.91 billion in 2022. Despite all of the chaos in the banking sector earlier this year and high-interest rates that have made it challenging for institutions to keep deposits on their books, Premier Financial has only seen the value of deposits continue to expand. At the end of the first quarter of this year, they totaled $6.77 billion. By the third quarter, they totaled $7.07 billion. Unfortunately, a rather sizable amount of these deposits, 32.8% in all, are classified as uninsured. This is slightly higher than the 30% threshold I prefer to see. But if we adjust for certain things such as collateralized amounts, exposure does drop considerably to 17.7%.

The growth in deposits has allowed the bank to increase the value of loans it gives out as well. These grew from $5.41 billion in 2020 to $6.39 billion in 2022. Loans peaked at $6.71 billion in the second quarter of the year before dipping slightly to just under that figure at $6.70 billion. I do understand that one area that investors are worried about is the office space. High vacancy rates have created concerns about the ability of office assets to cover the loans that are on them. The good news is that only about 5% of the loan portfolio owned by Premier Financial falls under this category.

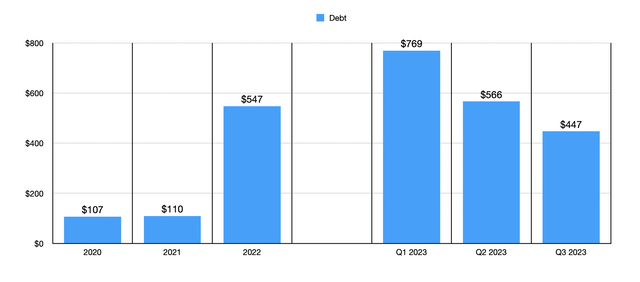

There are some other assets that we should pay attention to. For instance, we have the value of securities that the company invests in. These have bounced around in recent years between a low point of $737.7 million and a high point of $1.22 billion. As of the end of the most recent quarter, they totaled $917 million. The value of cash has remained quite low at the bank in recent years. At the high point, it stood at $161.6 million. And at the low point, it was the $117.5 million that the company ended the third quarter of this year at. And lastly, there is also debt. After seeing debt balloon from $109.7 million in 2021 to $547.3 million in 2022, it continued to climb until hitting $769.4 million in the first quarter of this year. Fortunately, the number has been on the decline since then. And by the end of the most recent quarter, debt totaled a more modest but still historically elevated $447 million.

Author – SEC EDGAR Data

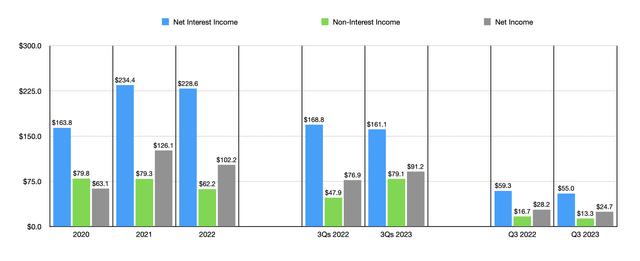

You would think that the general uptrend in deposits and loans would allow the institution to consistently grow. But there have been some hiccups along the way. As you can see in the chart below, net interest income dipped slightly from 2021 to 2022. And in the first nine months of this year, the amount dropped from $168.8 million to $161.1 million. Even though asset values are higher, a rise in overall debt has caused interest expense to grow, as have higher interest rates. But you also have net interest margin considerations caused by a tight interest rate environment. Non-interest income has also been quite volatile, though results for the first nine months of this year have been encouraging with the metric climbing from $47.9 million to $79.1 million. Net income, meanwhile, has followed a very similar path here. We do see some volatility from year to year. But the important thing is that we don’t experience any significant deterioration in the company’s earnings potential.

Author – SEC EDGAR Data

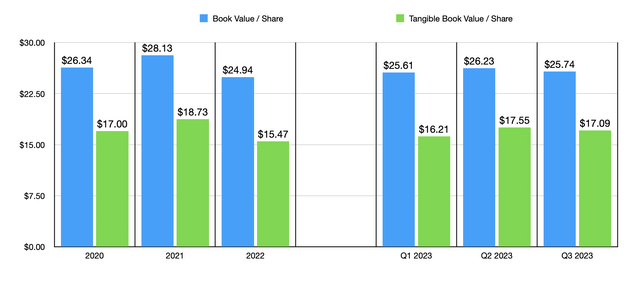

If we use the financial results covering the 2022 fiscal year, shares of Premier Financial look very cheap. The company is trading at a price-to-earnings multiple of 6, which is near the low end of what I have seen so far this year. Some companies are even lower than this, but many are higher. Shares are not just cheap relative to earnings. They are also cheap on a price-to-book basis. At present, the company is trading at a discount to its book value of 32.5%. And it’s trading at a premium to tangible book value of only 1.6%. Again, not the cheapest I’ve seen. But it is up there.

Author – SEC EDGAR Data

Takeaway

From all that I can see, I must say that I am quite impressed with Premier Financial. The institution has a good track record of growing its balance sheet. Income statement data has been less bullish. But it’s certainly not bad. The stock is cheap relative to both earnings and book value, and debt has dropped back to more realistic levels. Uninsured deposit exposure is a bit higher than I would like and I don’t like the volatility that I have seen in earnings. But these things are not enough to keep me from rating the company a very solid ‘buy’.

Read the full article here