YETI (NYSE:YETI) looks poised to benefit from some new distribution and new product introductions next year, going up against a bit easier comps with 20223 being impacted by product recalls.

Company Profile

YETI is an outdoor brand that sells products in three categories: Coolers & Equipment, Drinkware, and Other. Drinkware is largest category and was 59% of sales last year, while Coolers & Equipment represent about 38% of sales while Other was just 2%.

Its Coolers & Equipment line consists of both hard and soft coolers, as well as cargo, bags and outdoor living products. Its Drinkware products come in different form factors, but are generally make of 18/8 stainless-steel and are meant to keep beverages either hot or cold. The Other category includes a variety of apparel and different gear.

YETI sells its products in the wholesale channel through several large retailers throughout the U.S., Canada, Australia, New Zealand, Europe, and Japan. It also sells its products through the DTC channel through its own website and Amazon Marketplace. The company also operates 17 retail locations.

Opportunities & Risks

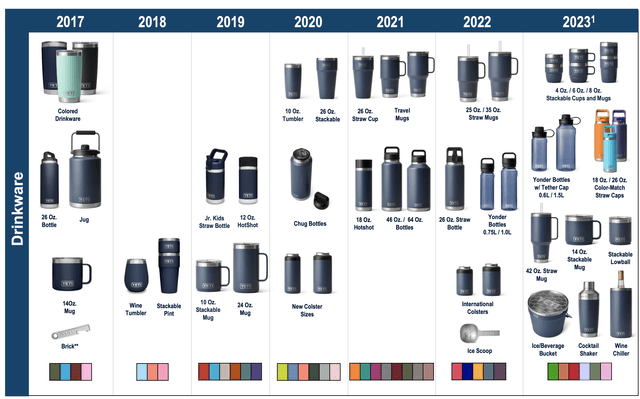

Product innovation and the introduction of new products is one the biggest opportunities for YETI. The company has a history of introducing new form factors for its popular drinkware, as well as introducing new types of coolers. This year, the company introduced a large variety of new drinkware options, including stackable cups and mugs, a 42 ounce straw mug, color-matched straw caps, a wine chiller, and cocktail shakers, among other introductions. On the cooler side, it introduced a soft cooler backpack and a new cargo offerings.

YETI New Product Introductions (Company Presentation)

The company has also been looking to drive sales through customization and adding new colors. It has also been selling limited edition items to drive interest in the brand.

Increasing DTC is another nice opportunity for the company. Yeti has been able to grow its DTC mix from only 8% in 2015 to 59% last quarter. It’s done a nice job of growing online sales, both through its own website as well as embracing Amazon Marketplace, which it started selling through in late 2016. Amazon Marketplace has been a great way for the company to expand its reach and capture a different audience. It also participated in its first Prime Day earlier this year, where it was able to sell some end-of -life and products with older colors.

Meanwhile, with only 17 retail locations, the company has room to add more physical stores. It opened three new stores in Q3. It’s also notable that between FY15-FY21, the company did cut back on its U.S. dealers by -60% to help protect the brand after it expanded too quickly in the wholesale channel. However, a new distribution deal with Tractor Supply (TSCO) looks like a great fit for the brand and should help grow its wholesale business, as well.

International expansion is another opportunity for YETI. International sales were only 16% of its total in Q3, which is low compared to many consumer brands. However, international revenue grew 20%, while domestic sales fell -3%. The company is only in a few select international markets and will look to expand within those markets before moving into new markets. On the international front, it opened up new distribution centers in the Netherlands in Q2 and in Australia in Q3. It also started offering e-commerce customization in its first international market with Australia earlier this year.

When it comes to risks, competition is a big one. Drinkware has been a popular category the last several years, but that has drawn in more players. There also seems to be a shift in the popularity of brands every few years. A few years ago, Hydro Flask was the “it” brand in the drinkware category, while more recently Stanley Cups have become very popular. Yeti may have a different core user demographic than these brands, but this does impact getting additional consumers.

Earlier this year, the company also ran into issues where it had to recall its new soft coolers and gear cases over magnet issues. It also recalled some travel mugs back in 2020. Recalls can hurt its results, as well as in some cases hurt its reputation as well. While I don’t think this is big issue going forward, it is something to watch. In bound freight costs was another issues that

The macro environment also remains a potential headwind. YETI’s products are not cheap, and is certainly an area where consumers can pull back on during periods of economic uncertainty. The company also sells into the wholesale channel, so retailers being cautious stocking inventory is a risk, is as overordering leading to eventual de-stocking issues, something many consumer product brands had to deal with somewhat recently.

Q3 Results

For its most recent quarter, YETI reported flat sales of $433.6 million, which was pretty much in line with analyst estimates. Adjusted EPS of 60 cents, topped the consensus by 5 cents.

Drinkware sale rose 6% to $253.3, while Cooler & Equipment sales fell -8% to $171.5 million. DTC revenue climbed 14% to $259.5, while wholesale revenue dropped -16% to $174.1 million.

On its earnings call, the company highlighted the success of its new drinkware option, with CFO Mike McMullen saying:

“We continue to see our innovation in Drinkware resonate with consumers and put us in a position to capitalize on trends in the market. For instance, we expanded our Yonder product lines with new sizes and lid offerings and launched new color match lids in our Rambler stainless bottle line. In addition, we had incredibly successful fall color launches in Camp Green, Cosmic Lilac, and Power Pink. We also remain encouraged by some of the initial success we are seeing as we look to move beyond individual use drinking vessels into more group sharing and entertaining options. As Matt outlined earlier, we think we can further capitalize on these trends in Q4 with our extensive lineup of new innovation. This includes an expanded range of products designed for coffee occasions with three smaller size cups and mug, a great new hydration solution with the Rambler 42-ounce Straw Mug and the introductions of new entertaining options with the YETI Cocktail Shaker and Wine Cellar.” Gross margin climbed 670 basis points to 58.0%, helped by lower in-bound freight costs and lower product costs.

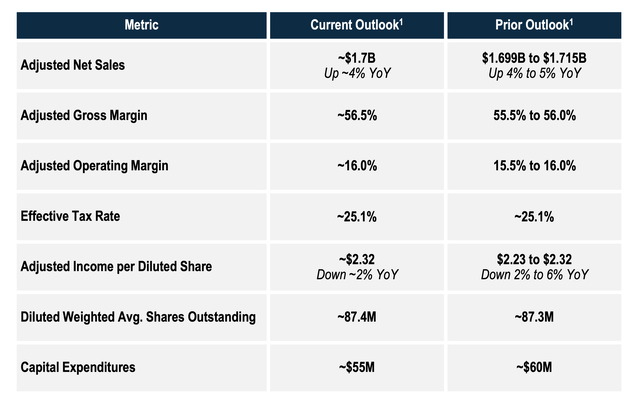

Looking ahead, the company projected full-year adjusted EPS of about $2.32, at the high-end of its previous guidance of $2.23-2.32. It is looking for sales growth of around 4% to $1.7 billion. For Q4, it is looking for 10% growth, helped by a new distribution deal with TSCO.

Company Presentation

Overall, the third quarter was mixed for YETI. Sales were flat, but it DTC sales rose and the company to call out good sell-through in the wholesale channel. Meanwhile, gross margins improved nicely, helped by lower freight costs.

The guidance for Q4 looks solid, as the company is set to benefit from its new TSCO distribution channel. It seems like the store should be a good fit for the outdoor brand.

Valuation

YETI stock currently trades around 10.7x the 2023 consensus EBITDA of $315.4 million and 9.2x the 2024 consensus of $368.3 million.

It trades at a forward PE of 17.3x the 2023 consensus of $2.29 and 14.5x the 2024 consensus of $2.73.

It’s projected to grow revenue by 7% this year and 10.3% next year.

While it doesn’t have a great similar peer, it generally trades towards the high end of more non-apparel consumer discretionary stocks. However, given its superior growth, this seems justified. I think a 12.5x multiple of 2024 EBITDA looks like a fair target given its double digit projected revenue growth, which would equate to a $55 stock price.

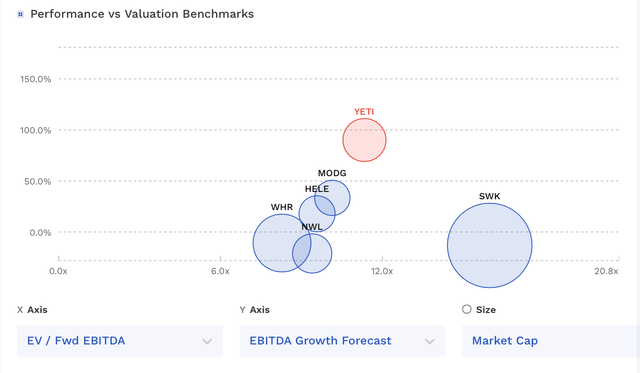

YETI Valuation Vs Peers (FinBox)

Conclusion

If the consumer holds up, TSCO should be in pretty good shape for 2024. It will lap the recalls that impacted 2023, as well as have a full year of all the new products offerings that came out this year. It also will have a full year of new TSCO distribution, as well as some more of its own retail stores, as well as a full year of some of its international initiatives.

Its valuation of near 9x 2024 EBITDA also isn’t that challenging given its projected return to 10% growth. That said, the overall state of the consumer remains a risk. Taken all together, I’m going to rate YETI a “Buy,” but I would be mindful of the macroenvironment.

Read the full article here