Editor’s note: Seeking Alpha is proud to welcome Brave Investor as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis In A Nutshell

Currently, Orlen (OTC:PSKOF) trades at a substantial discount to its book value, standing at 0.45x, and has notably low multiples, with an EV/EBITDA ratio of 1.3x and a P/E ratio of 2.1x. with respect to 2022 results. Using an estimate of 2023 results, EV/EBITDA would be around 1.5x and 2x and P/E around 3.5x.

In other words, it has a current market value of 17 billion euros and is generating around 5-7 billion in profit.

This valuation certainly takes into account various factors, including potential fluctuations in oil price/cycle (anticipating price decreases), uncertainties about capital allocation (particularly towards renewable investments), the company’s shareholding structure, with 49% state ownership, and the vulnerability of the Polish currency, the zloty.

However, Orlen’s unique strengths, including its complete vertical integration, diversified portfolio, and strong cash position, position it exceptionally well to navigate the energy transition while delivering significant value to its shareholders. Given the sustained demand for oil until alternative fuels like hydrogen become more prevalent, Orlen would have great earnings potential, especially given the limited investment in new oil wells and refining facilities during this transitional period.

Orlen’s Business

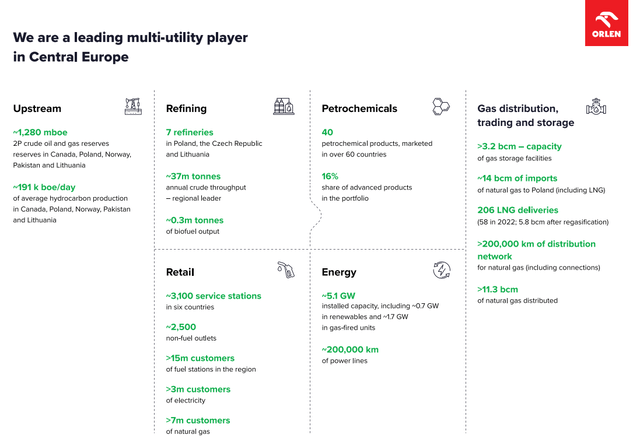

Orlen SA is a Polish oil company founded in 1999 through the merger of Centrala Produktów Naftowych (‘CPN’) and Petrochemia Płock. The company is the largest company in Poland and one of the leading oil and gas companies in Central and Eastern Europe, with a market capitalization of around 15 billion dollars. After the merger, Orlen became an energy conglomerate. Please see the link to their corporate strategy presentation for more detailed information (page 14).

Orlen’s financial information

It engages in oil and gas exploration and production, refining, petrochemicals, fuel marketing, and power generation. It is a vertically integrated company with a relevant cyclical component, as the main activity (around 50% of the business) is the refining segment. The company operates in over 20 countries worldwide.

Poland’s Economy

Orlen is highly significant to the Polish economy. The company is a major contributor to the state’s finances (49% state ownership).

Poland is one of the fastest-growing economies in Europe, surpassing even South Korea in GDP growth since 1980. This puts Poland ahead of the United Kingdom by 2030, with a per capita GDP higher than that of the UK. Average growth of 2% is expected for the next three years. A country with such economic growth will require more energy. A clear beneficiary of this trend, expected to continue for decades, should be ORLEN, especially through a combination of traditional and renewable energies.

From an investing point of view, something relevant it’s that Poland has its own currency, the zloty. Orlen is listed on the Warsaw Stock Exchange (WSE:PKN), although an investment in EUR is also possible (PKY1:FRA). Investing in Orlen from a USD point of view means that every investor is exposed to the exchange rate risk. This means that if the PLN or the EUR depreciates against the USD, your investment in Orlen will be worth less in USD terms. The higher the US interest rates, the lower the Polish economic growth or the lower risk appetite for Poland could mean a depreciation of the zloty, which may affect your investment. To mitigate this, hedges are one clear option (buying PLN forward contracts or USD put options) Nevertheless, I am confident about the Polish economy as it is expected to grow faster than the US economy. This means that the PLN is likely to appreciate against the USD over time. In any case, currency risk is definitely something to consider when investing in Orlen.

Lotos And PGNiG Mergers

In 2020, 27% of the company was owned by the Polish state. However, the shareholding structure changed recently as a result of two major mergers with the LOTOS and PGNiG groups. LOTOS was Orlen’s largest competitor.

PGNiG was the country’s largest gas wholesaler and retailer, with around 90% of gas sales to end consumers in Poland. The Polish state’s stake in ORLEN increased after the mergers. In other words, shareholders of the acquired companies received Orlen shares as compensation, with the State compensated with a substantial amount as the main shareholder of the companies (for example, around 70% of the PGNiG group was state-owned), leading to an increase in its relative ownership. Therefore, the current shareholding has increased to 49.9%, which is not a random number. This acquisition was allowed by the European Commission, as long as it did not exceed 50% control, which has been the case.

Before these mergers, in 2020, Orlen had already acquired Energa, a relevant player focused on renewable energy generation.

The newly formed company resulting from all these mergers is led by Daniel Obajtek, who has been the CEO of Orlen since 2018. Obajtek is a Polish politician who served as a member of the Sejm, the lower house of the Polish Parliament, from 2007 to 2015. These mergers solidify Orlen’s position and represent a significant step in the consolidation of the Polish energy sector. Poland’s politics are complicated, with a recent election that will probably result in a change of government. Management may potentially change, but I personally see Orlen in a strong position for the future.

Transition To Renewable Energies And Dividend Policy

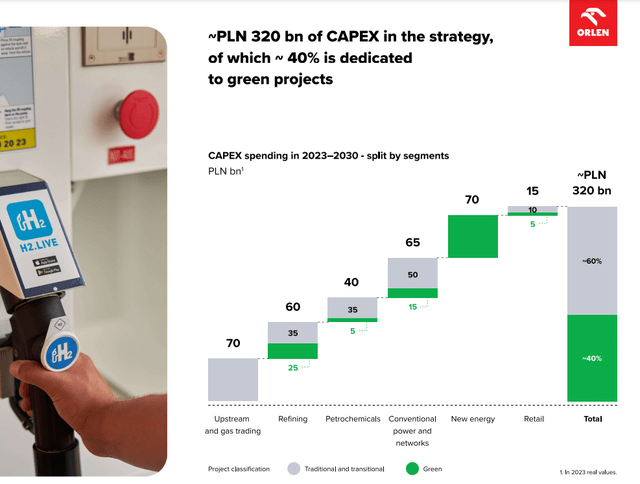

Knowing where a company is heading is a crucial aspect of any valuation or thesis, particularly when it comes to capital allocation during the transition to green energy. Orlen has shared its plan for 2030, which is publicly available on its website.

Based on their 2030 Strategy presentation, Orlen’s plan focuses on three key pillars: decarbonization, sustainable growth, and integrity and responsibility. To achieve these goals, Orlen will invest a total of 320 billion zlotys (65 billion euros) over the next seven years. These investments will focus on the following projects:

- Renewable Energies: Orlen will build new solar and wind power plants, as well as biofuel facilities.

- Energy Efficiency: Orlen will improve the efficiency of its operations in all business segments.

- Carbon Capture and Storage: Orlen will develop technologies to capture and store the carbon dioxide produced by its operations.

- Electric Mobility: Orlen will build a network of electric vehicle charging stations and develop new products and services for the electric mobility market.

The division is shown in the image below. Please see the link to their corporate presentation for more detailed information (page 8).

Orlen’s strategy documents

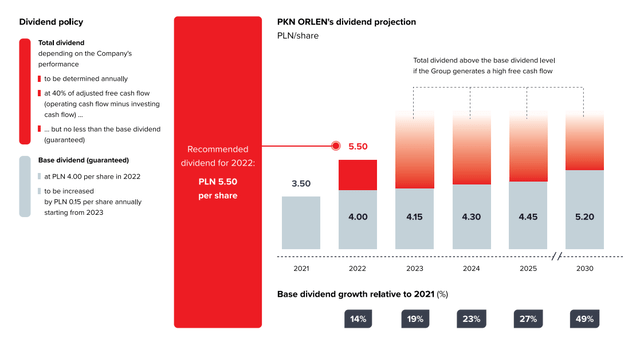

To finance these investments, Orlen will use a significant portion of its current earnings and debt capacity, reducing the available cash for buybacks and dividends. However, this strategy is aimed at generating more long-term earnings. This implies that the cash available for dividend payments will be limited.

However, I maintain an optimistic view on this matter, given the importance of ORLEN’s dividends for Poland as a nation. Additionally, Orlen has recently provided clarity on its dividend policy, indicating that approximately 40% of free cash flow will be allocated to dividend payments.

Orlen’s strategy documents

Even in a scenario of oil price reductions, Orlen is committed to maintaining a base dividend, unless substantial unforeseen challenges occur. Currently, this base dividend amounts to 4.00 zlotys per share, equivalent to approximately one billion euros annually, and is expected to increase incrementally by 0.15 zlotys each year until 2030.

Given the current share price, this translates to a minimum dividend yield ranging from approximately 7% to 10%, depending on the company’s commitment to at least deliver the “base dividend”. In this context, Orlen takes on the character of an investment with pure yield, particularly if it encounters obstacles to improve its financial performance. However, it is essential to highlight the company’s ambitious strategic initiatives, which could substantially shape its trajectory in the coming years.

The new investments are expected to generate an accumulated EBITDA of over 400 billion zlotys by 2030 (see page 45 of the link, approximately 85 billion euros), implying a total annual EBITDA of around 15 billion for the year 2030. Therefore, the company is currently valued at approximately 15 billion euros in the stock market, and its plan is to achieve an annual EBITDA of 15 billion euros by 2030. This means that if they manage to follow their plan, Orlen would trade at an implied EV/EBITDA ratio of 1x in 2030.

Valuation

In this case, I perform a multiples-based valuation, with historical data serving as a benchmark. A discounted dividend model could be valid, although a discounted cash flow model is understood to lose much sense when almost everything will go to CAPEX.

Forward Valuation

We cannot use 2022 results as a good proxy due to the fact that PGNIG and Lotos were not integrated and that 2022 was a very good year for refining. This means that 2022 results are quite extraordinary, and we need to use most recent information.

As discussed below, I have gathered information from H1 2023 results and the 2021 results (considering the PGNiG and Lotos groups plus Orlen’s figures), which offer a more representative benchmark, reflecting a return to more typical oil prices (around $60-80 per barrel).

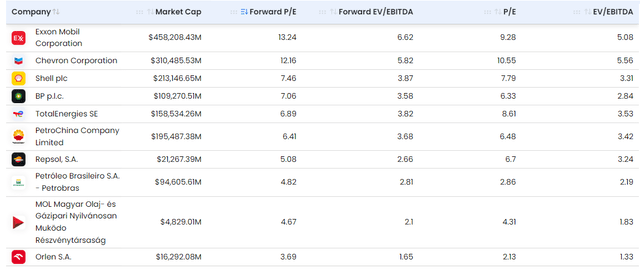

Both on a forward and trailing valuation basis, comparable companies of similar size, such as Shell, BP, and Exxon, usually have EV/EBITDA multiples ranging from 3 to 7x. This underscores the fact that we defend in the thesis, a significant margin of safety even if Orlen’s earnings experience a decline. Please below Stratosphere data on comparables.

You can introduce the names of the companies you want to compare.

Stratosphere

As it is explained below, assuming a forward conservative EV/EBITDA ratio of 3x, the potential upside compared to the current stock price could be approximately 40%.

I believe that 2023 YTD results are representative of a good year, and we expect EBITDA and net profits to be lower in future years.

YTD 2023 EBITDA amounts to 35 billion zlotys (around 7.5 billion euros).

Using this as a proxy for 2023, I estimate an EBITDA of close to 9.5-10 billion euros. I assume an exchange ratio of 1 Zloty = 0.22€ based on current rates.

Even so, this is based on high crack spread margins and oil prices in 2023. For 2024 and 2025, based on a decrease in both margins, I estimate EBITDAs of at least 9 billion and 8 billion euros respectively.

Using the 2.5x multiple and this EBITDA estimation I have prepared the following cases, which explain why Orlen’s valuation spells opportunity:

• Base Case:

- Using 2023 result estimation as a proxy with a 3x multiple. Normalized earnings in 2023 ≈ 45 billion zlotys. 3x ≈ 135 billion zlotys representing a ≈ 80% potential revaluation compared to the current value.

- For 2024: estimated earnings for 2024 ≈ 41 billion zlotys. 3x ≈ 123 billion zlotys representing a ≈ 64% potential revaluation compared to the current value.

- For 2025: estimated earnings for 2025 ≈ 36 billion zlotys. 3x ≈ 108 billion zlotys representing a ≈ 44% potential revaluation compared to the current value.

Now I will assume the same (already depressed) multiples in a stress case, where EBITDA is 36 billion zlotys. Using a 2x multiple, which is a ridiculously low level, we would arrive at 72 billion zlotys, which represents a ≈ 5% downside. From my point of view, this scenario is extremely conservative, as these ratio levels are more related to a high-earnings scenario rather than a low-earnings one.

All of these results don’t consider dividends, expected to amount to up to 10% per year. This is another reason why Orlen’s valuation spells opportunity – even if there is no capital appreciation, there is a reasonable amount of dividends expected, as per the policy explained above.

In the long term, if the plans of achieving 60 billion zlotys in EBITDA by 2030 materialize, at current (depressed) multiples, we could see a 150% potential revaluation over 7 years, in addition to dividends (around 7 to 10% for a compounded annual growth rate of 21%, or historically 28% compounded annual growth).

In any case, it’s crucial to recognize that Orlen intends to allocate a significant portion of its EBITDA (and free cash flow) to capital expenditures. This aligns with current market expectations, which are influenced by relatively high estimates of the weighted average cost of capital (WACC), estimated at around 14%.

Consequently, cash flows beyond the fourth or fifth year are almost negligible, and Orlen’s current investment and dividend policies heavily impact market prices.

Risks

It must be said that the valuation is highly dependent on the cycle and other factors.

Main Orlen business is refining (around 50% of current revenues) Refining is a cyclical activity, which tends to overheat with gasoline demand and suffer when there are recessions. If the economic cycle takes a downturn, the valuation would be affected if current multiples are maintained.

Currency as well as political risk and projected results are also significant factors to consider. The Polish State has a relevant percentage of shares (almost 50% as discussed above) On one hand, recent elections have created relevant uncertainty on what are going to be the plans for Orlen. On the other hand, the local currency, the zloty, has experienced some degree of volatility, which is not beneficial to Orlen. Its evolution will depend on a series of factors that the company doesn’t control. From an investing point of view, hedging is a clear option, but I remain confident in Polish economic growth and the appreciation of the zloty.

In particular, capital allocation is a significant topic, as renewable investments are not expected to have high returns. It is clear that the way Orlen will invest its own profits in renewables is key for a successful business case, what I personally believe that it is very well positioned to be the key utility player in East Europe.

Conclusion

Orlen presents a compelling opportunity for investors seeking a blend of stability, potential for substantial gains, and a dependable dividend stream. The company’s current valuation is notably attractive, offering a reasonable safety margin.

However, it’s imperative to acknowledge the inherent risks associated with the economic cycle, especially in light of potential fluctuations in oil prices. Despite these challenges, Orlen stands out as a prominent global player in the sector, solidifying its competitive advantage and fortifying its moat.

While the expansion into renewable energy does introduce certain risks, such as increased competition, Orlen’s robust positioning and strategic initiatives equip it to thrive in this evolving landscape.

In essence, Orlen not only offers the potential for capital appreciation but also ensures a reliable dividend stream for the foreseeable decade. This dual benefit, coupled with the company’s competitive edge, underscores the compelling investment proposition it presents to astute investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here