Last time I wrote about Blackstone Mortgage Trust, Inc. (NYSE:BXMT) it was in April this year, right before the release of the Q1 2023 report, and the trust was coming from a roughly 44% drop in a matter of a year. As of today, BXMT is doing much better and trading at $21.35 – roughly 20% growth since the $17.85 of my last article. This capital appreciation plus the dividends paid in both June and September make it a quite profitable investment up to now. But has BXMT reached its peak or is it still a good time to enter? As for my last analysis, I still believe that the main interest one should have in a stock like BXMT is the dividend, as it still sits at an attractive 11.62% yield.

Business Model and Key Financial Data

I won’t dig too much into the business model in this second article, but with about $22.1 billion in loan portfolio and a weighted-average origination LTV of 64%, BXMT functions as a lender in the commercial real estate market. The firm specializes in offering first mortgage loans to proprietors and managers of real estate, primarily concentrating on senior loans backed by properties that generate income. These loans are generally short-term, ranging from 3 to 5 years, and are entirely floating-rate, which safeguards them against fluctuations in market interest rates.

The first change I noted when comparing the Q4 2022 (basis for my last article) results and the most recent Q3 2023 results is that the loan portfolio size has decreased by about $4 billion, from $26.8 billion to the current $22.1 billion; not surprisingly also the book value per share decreased from $26.26 to $25.90. Furthermore, the performing portfolio percentage decreased from 99% to 95%, which although a very low change should be monitored in case of further declines. On the other hand, the weighted-average risk rating has remained almost stable going from 2.8 to 2.9. Finally, the CECL reserve, which is the allowance for current expected credit losses, has increased from $343 million to $477 million. Possibly to compensate for these slightly declining metrics, the liquidity has increased to a record $1.8 billion, bringing the leverage down by 0.2x compared to Q4 2022, which is definitively positive given the increasingly uncertain economic outlook.

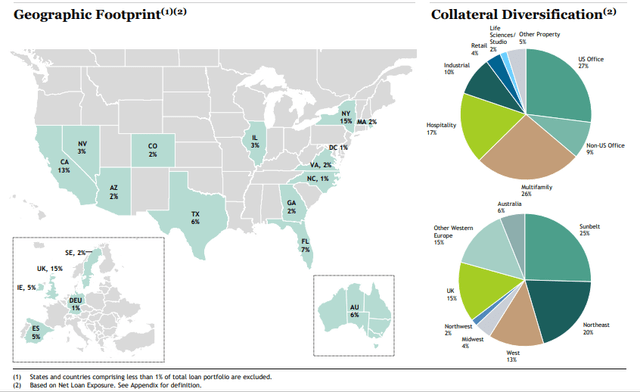

Compared to seven months ago when I wrote my first analysis, the main difference I see in the allocation is the shift from a fully US office space exposure to an inclusion of non-US offices in the portfolio. In fact, US Office has decreased from 40% to 27%, however, there is also the addition of 6% non-US Office, which brings the total to 36%. Some people might find this a still too high exposure to office space, given the still current “work-from-home revolution”, but to me the hybrid model is here to stay and office spaces are still going to be valuable in the coming years.

Geographical and Collateral Diversification (Blackstone Mortgage Trust, Inc. – Third Quarter 2023 Results)

Financial Performance

From the graph below one might be pessimistic about the performance of BXMT, however, it has grown about 20% since April, showing a definitively positive trend for the last period. Compared to the performance of the sector we can see that it’s not too different.

BXMT Share Price YTD (Seeking Alpha)

As I mentioned in my last article, BXMT has a long-standing track record of strong financial performance. In Q3 2023, the dividend coverage was still at a relatively healthy 126%, confirming that BXMT is still sustainable. Regarding the overall economic situation, I don’t see many structural changes since the last article I wrote so I won’t go to deep into details. What was important for me in this update analysis was to see that the US economy (BXMT’s main exposure region), is still resilient and strong, which makes me somewhat optimistic towards the resilience of this REIT’s borrowers.

Valuation

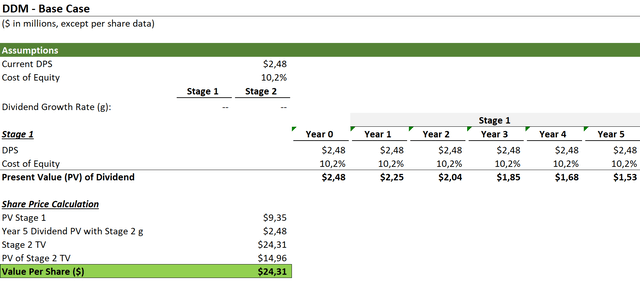

Last time I valued this company I used a two-stage dividend discount model given the uncertainty of the short-to-medium term economic environment. Using three different sets of assumptions, I weighted the valuation between pessimistic, base, and optimistic scenario – with a resulting valuation of $24.

Given the changes I’ve mentioned above, I don’t see the need of changing the assumptions, as the changes have not been dramatic in neither the company or the economy affecting the firm. I will therefore copy below my previous valuations and reasoning.

The first model below is the base case, in which dividend stays constant. I believe this is a quite realistic scenario as BXMT might want to avoid not paying dividends but also not increase before the economy stabilizes. With these assumptions BXMT is quite undervalued.

DDM – Base Scenario (Personal Calculations)

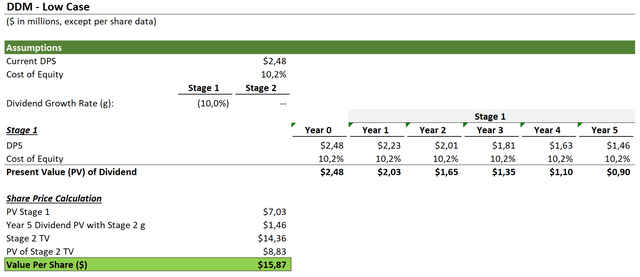

In the more pessimistic case I opted for a negative growth of -10% dividend growth every year for the next 5 years, for then to settle at a 0% growth.

DDM – Pessimistic Scenario (Personal Calculations)

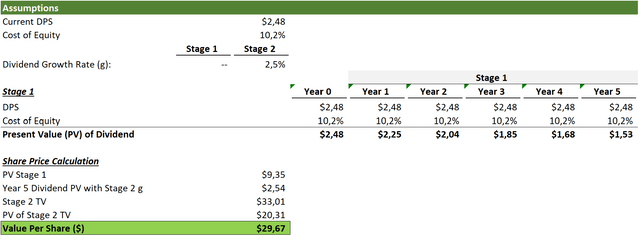

Finally, for the more optimistic scenario I still opted for a 0% dividend growth for the first 5 years, but a 2.5% growth after that.

DDM – Optimistic Scenario (Personal Calculations)

Finally, assigning a 50% weight to the base case and 25% each for the pessimistic and optimistic, we still get a share price of roughly $24 – 40% higher than current prices.

Risks

BXMT defends itself from rising interest rates with the 100% floating rate portfolio, however, the operators it lends to might default on the loans. This risk is becoming a bit more real, albeit marginally, with the percentage of loans performing decreasing from 99% to 95% and the weighted-average risk rating going from 2.8 to 2.9. However, I see the US economy being resilient for the time being, and with BXMT’s biggest debtors being office operators, multifamily, hospitality, and industrials I think their portfolio is good from a diversification point-of-view.

In my last article, I touched on a pretty important point that a lot of readers also picked up on in the comments – the way office space valuations could really shake things up for BXMT’s portfolio. But, looking at it from another angle, I actually think there’s a silver lining with them cutting down on office spaces in the U.S. and expanding more internationally. The big worry everyone’s talking about is how the work-from-home trend might make office spaces less valuable. By spreading out across different countries, BXMT is playing it smart because each country has its own take on remote work. This kind of move could really help balance things out for their portfolio, especially with how the workplace is changing these days.

Conclusion

While last time the company was significantly undervalued, with a potential for 40% appreciation, today BXMT appears to be much closer to its fair valuation, with a potential appreciation of about 12%. Given the particularly risky nature of mortgage REITs, which is offset by attractive dividend yields, this potential upside seems too small to justify an investment.

Current investors, like myself, have several reasons to hold onto the stock and continue enjoying the robust dividends, depending on their entry price and other factors. However, if I were considering an investment today, I would prefer to wait on the sidelines for a decrease in price or some other significant opportunity to arise.

Read the full article here